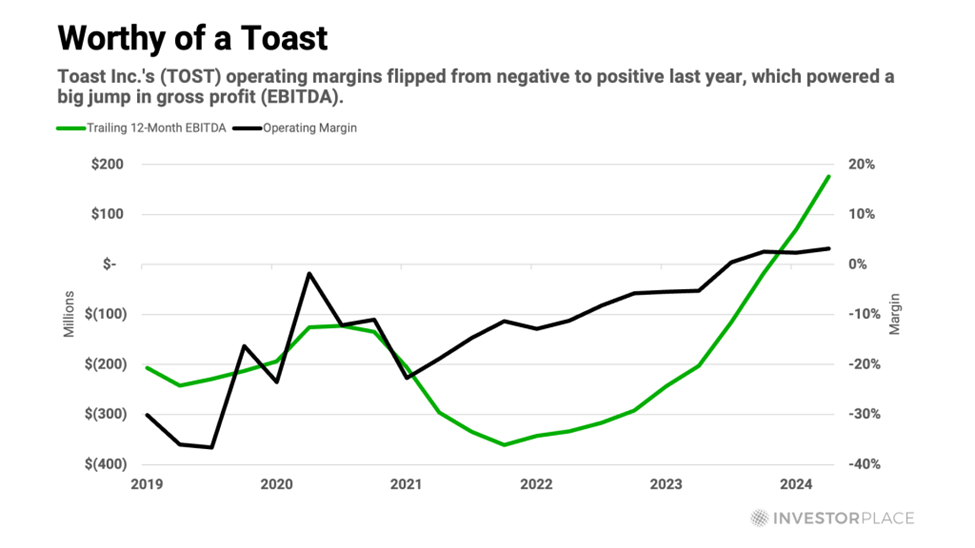

Wall Street Has Mispriced This Risk

Walmart should “eat” tariffs … can the average U.S. consumer absorb them? … earnings estimates don’t support stock prices … Jeff Clark says lower prices are coming … but looking farther out, AGI stocks are where we want to be

We’re anticipating a barrage of new trade deals, as well as a lower tariff on China.

But until that happens – and potentially even after that happens if the blanket 10% tariff remains – retail prices and consumer spending are on a collision course.

Will it be a fender bender or complete totaling?

Last week, we reported on Walmart’s CFO John David Rainey’s statement that the 30% tariff on China is “still too high.” He suggested price increases are on the way:

We’re wired for everyday low prices, but the magnitude of these [tariff] increases is more than any retailer can absorb. It’s more than any supplier can absorb.

And so, I’m concerned that the consumer is going to start seeing higher prices. You’ll begin to see that, likely towards the tail end of this month, and then certainly much more in June.

President Trump took offense over the weekend. He took to social media, writing:

Walmart should STOP trying to blame Tariffs as the reason for raising prices throughout the chain.

Between Walmart and China they should, as is said, ‘EAT THE TARIFFS,’ and not charge valued customers ANYTHING. I’ll be watching, and so will your customers!!!

It appears Walmart will eat the tariffs, at least, to some degree.

Speaking on NBC’s “Meet the Press” Sunday, Treasury Secretary Bessent said Walmart will:

Eat some of the tariffs, just as they did in ’18, ’19 and ’20.

As an investor in Walmart, I don’t like being told to bear the financial burden of someone else’s decision. If Walmart executives (and high-profile investors) eventually share my sentiment, resulting in higher prices, is the average U.S. consumer equipped to handle it?

Yesterday, we looked at the financial health of lower-income Americans

Let’s pick back up with that as we answer the question.

Here’s Jack Kleinhenz, chief economist of the National Retail Federation:

Consumers are still spending despite widespread pessimism fueled by rising tariffs.

While tariffs may have weighed on spending decisions, growth is coming at a moderate pace and consumer spending remains steady, reflecting a resilient economy.

This is good news, and echoes the phenomenon of the “surprisingly resilient” U.S. consumer that’s helped our economy elude a recession for years now.

However, Kleinhenz went on to say that the U.S. economy is “at a pivot point.” So, the more appropriate analysis isn’t “what’s happened so far?” it’s “what’s going to happen?”

But even that question misses the mark. The best question is “what do consumers believe is going to happen, which will influence their spending decisions?”

Back to Kleinhenz:

People are on an economic cusp, and when people worry about their jobs, their anxiety often triggers a slowdown in consumer spending.

Last Friday’s University of Michigan consumer sentiment survey revealed how inflation expectations are running higher than those seen in 2022, back when we had soaring inflation. In early May, one-year inflation expectations jumped to 7.3% – the highest level since 1981.

If you’ve listened to Fed Chair Powell speak, he frequently reports that “long-term inflation expectations remain well-anchored.”

The risk is that these well-anchored expectations are slipping.

Now, what might soothe wary consumers, re-anchoring their expectations, are lower interest rates from the Fed and commentary from Fed presidents that higher prices from tariffs aren’t a major concern.

Neither of these is happening.

The Fed isn’t as dovish as many had hoped

One of the foundations of the bull argument is that we’re on the cusp of a handful of Fed rate cuts. They will lead to a decline in treasury yields that will trigger a daisy chain of fortuitous financial repercussions (think lower mortgage rates and lower borrowing costs at the bank).

Additionally, lower rates will be a tailwind for stock market valuations while also making bond yields look less attractive to investors, further strengthening the case for stocks.

But rates haven’t fallen this year – despite Wall Street’s expectations.

For example, one month ago, traders put 52.1% odds on at least four quarter-point cuts by December.

As I write, that probability has dropped to 6.9%. And if Atlanta Fed President Raphael Bostic has his way, the Fed will cut just once in 2025.

Here’s CNBC:

Atlanta Fed President Raphael Bostic told CNBC on Monday that he currently prefers only one rate cut this year as the central bank tries to balance potential upward pressures on inflation with worries of a recession.

The Federal Reserve released projections in March that pointed toward two quarter-point rate reductions in 2025.

However, Bostic said Monday that the tariffs have been larger than the central bank expected at the start of the year.

Can the average U.S. consumer handle just one cut this year?

It might not be comfortable, but most likely, yes – even if they say otherwise.

Let’s remember that soft data like the consumer sentiment survey doesn’t always translate into reduced consumer purchases.

Powell made this point in his post-FOMC press conference earlier this month:

I think going back a number of years the link between sentiment data and consumer spending has been weak.

So, I’m not suggesting that we’re headed for a deep recession.

But the risk for you and me isn’t so much that the average consumer falls off a cliff, it’s that the stock market has incorrectly priced earnings based on how much the average consumer will actually spend in a tariff environment.

Today, the S&P 500 is barely 3% below its all-time high. For all practical purposes, we’re at the all-time high.

And yet, there’s now a blanket 10% tariff on most of the U.S.’s trading partners, and a 30% tariff on China.

Is that logical?

Bulls may respond, “Yes. The market is looking forward, pricing in the removal of these tariffs.”

Someone forgot to tell Commerce Secretary Howard Lutnick.

About two weeks ago, he said:

We will not go below 10 percent. That is just not a place we’re going to go.

Permanent 10% tariffs and pre-Liberation Day earnings growth rates are incompatible. And yet stocks are basically back to pre-Liberation Day levels.

JPMorgan’s CEO Jamie Dimon sees the disconnect. Here’s CNBC from yesterday:

JPMorgan Chase CEO Jamie Dimon…believes the risks of higher inflation and even stagflation aren’t properly represented by stock market values, which have staged a comeback from lows in April…

In six months, [earnings] projections will fall to 0% earnings growth after starting the year at around 12%, Dimon said. If that were to happen, stocks prices will likely fall.

I hope Dimon is wrong. But let’s at least recognize the risk.

“Recognizing the risk” is why master trader Jeff Clark recently bet against stocks

Last week, we told his readers “It’s time to bet on another decline phase.”

First, if you’re new to the Digest, Jeff is a technical trading expert. He uses a suite of indicators and charting techniques to profitably trade the markets regardless of direction – up, down, or sideways.

Big picture, Jeff believes we’re in a bear market that won’t bottom until later this fall around 4,125. That’s 30% lower than where it trades as I write Tuesday approaching lunch.

Here’s Jeff’s latest thinking from this morning:

The S&P 500 managed to recover all of yesterday morning’s losses, and close up a few points on the day. Much of that action, I suspect, was bears and reluctant bulls throwing in the towel and just buying anything in order to participate in the rally.

Meanwhile, all of the technical warning signs remain.

So, as I’ve argued for the past several sessions – if not the past few weeks – there is a pullback coming. I can’t say definitively when. Though, I suspect it’ll happen soon…

Technical conditions are stretched. Fundamental valuations are stretched. And, the risk in the market right here is far greater than the potential reward.

Troubling as that might sound, even in a bear market, Jeff writes that there’s plenty to look forward to – massive rallies (within a broader decline) that we can trade for fast, double-digit profits, followed by a “generational buying opportunity” at the ultimate bottom.

We’ll continue bringing you more of Jeff’s analysis, but to join him for all his daily updates, click here to learn about joining him.

Even if you’re bearish, don’t overlook the wildly bullish longer-term outlook for leading AI stocks

Even if lower prices are in our short- and medium- term outlooks, higher stock prices for leading AI stocks seem all but certain the farther out we look. After all, we certainly won’t have less AI profits five years from now – likely, dramatically greater profits, with related stock prices to show for it.

Over the last few days, we’ve highlighted Eric Fry’s research on AI – specifically, the “Road to AGI.”

AGI refers to “Artificial General Intelligence,” which is the watershed moment when an AI system can match or exceed the cognitive ability of the smartest human across any task. The arrival of AGI is hurtling toward us, and it’s drawing a sharp dividing line in the investment world. Eric says there are two camps: “the AI appliers and the AI victims.”

We’re running long today, so I’ll bring you more of Eric’s research in tomorrow’s Digest. But Eric’s latest AGI research video is available to you right here.

Eric dives into his AGI blueprint, including details on critical stocks to avoid or sell immediately before they collapse under the weight of AI advancements.

We’ll keep you updated on all these stories here in the Digest.

Have a good evening,

Jeff Remsburg