Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

Aussie jumps to six-month highs

The Australian dollar closed at the highest level since November overnight after a weaker US manufacturing reading hit the US dollar.

The key ISM manufacturing report came in at 48.5 – below the 49.3 expected – in another sign of a slowdown in US manufacturing activity. Other US manufacturing numbers also missed forecasts while the “prices paid” component was also lower.

The USD tumbled on the news with the US dollar index down 0.7% as it fell to the lowest level since 22 April.

The Aussie and kiwi led the charge higher. The AUD/USD gained 1.0% while NZD/USD gained 1.2%.

The USD/CNH gained 0.1% while USD/SGD fell 0.5%.

Greenback also pressured with Waller open to cuts

Growing expectations that the US Federal Reserve might be willing to cut interest rates also weighed on the USD.

In line with the negative risks to employment and economic activity brought on by trade policy, Fed Governor Christopher Waller stated that he still sees a route to rate cuts later this year.

He recommends seeing through a brief increase in price growth, even though tariffs should exacerbate inflation in the “coming months.”

At a Bank of Korea conference in Seoul, Waller stated, “I would be supporting ‘good news’ rate cuts later this year, provided that the labor market stays strong, that underlying inflation keeps moving toward our 2% target, and that the effective tariff rate settles close to my lower tariff scenario,” according to Bloomberg.

The “smaller-tariff” scenario assumed a 10% average tariff and that higher nation and sector-specific charges would be negotiated lower over time, while his “large-tariff” scenario envisaged an average trade-weighted tariff on goods of 25% that persisted for “some time.”

Euro gains as EU looks to strike back

According to Reuters, the European Commission stated on Saturday that the EU is ready to strike back against US President Trump’s increase in steel and aluminum tariffs.

“Consultations on additional countermeasures are presently being finalized by the European Commission.

According to a spokeswoman, “existing and additional EU measures will automatically take effect on July 14 — or earlier, if circumstances require — if no mutually acceptable solution is reached.”

EUR/SGD might be poised for correction given ECB is expected to cut 25bp this week with dovish commentary.

Next key support lies on 21-day EMA of 1.1297 and 50-day EMA of 1.1179, where EUR buyers may look to take advantage.

On the other hand, the AUD/EUR was higher on Monday as it extended gains from one-month lows, thanks mainly to the AUD’s recent outperformance.

Aussie ends at highest level since November 2024

Table: seven-day rolling currency trends and trading ranges

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Canada’s economy grew at an annualized rate of 2.2% in Q1 2025, closely mirroring the revised 2.1% expansion in the previous quarter (down from an initial 2.6%). While this suggests stability on the surface, the underlying factors paint a more nuanced picture. Much of the growth was driven by businesses stockpiling inventories ahead of anticipated tariffs and a sharp uptick in machinery investment, both of which are unlikely to be sustained in the months ahead.

Trade activity also showed signs of softening. Export growth remained positive but was largely fueled by companies front-loading purchases of machinery and autos in preparation for potential disruptions. This means that inventory accumulation and trade, rather than broader economic momentum, were the key drivers of growth.

Meanwhile, household spending weakened noticeably, particularly in services, a stark departure from the robust gains of the past four quarters. Residential investment also took a sharp downturn, reversing much of the late-2024 rebound. Uncertainty around trade policy and broader economic conditions continues to weigh on housing activity.

Non-residential investment remained positive, though growth slowed compared to the previous quarter. A surge in machinery and equipment investment helped offset declines in structural investment, but the sustainability of this trend remains in question.

Looking ahead, while Canada’s economy continues to expand, much of the recent strength has been tied to temporary factors. The downward revision of Q4 2024 growth from 2.6% to 2.1% reinforces a sense of caution. Preliminary data from April suggests the expansion is continuing (+0.1% m/m), but the risk of near-zero growth in the second quarter remains significant.

Can the CAD go 5 in a row?

Kevin Ford – FX & Macro Strategist

The CAD just wrapped up its strongest four-month streak since 2021, closing Friday at 1.373. Will it extend to five months? The last time it posted five consecutive months of gains against the USD was back in April 2020, a similar price pattern that saw it surge to 1.467 before pulling back to 1.30.

What stands between the CAD and next key support at 1.35? The loonie’s 2-year average aligns closely with key support at 1.37, reinforcing its technical significance. Short-term price action continues to be dictated by movements in the US dollar, where persistent bearish positioning remains overstretched. A contrarian view would suggest that the overstretched positioning against the USD is poised for a pause at least, potentially putting a floor on the CAD.

However, as June kicks off, the USD/CAD has hit a fresh 2025 low at 1.3675, testing the 1.37 support level. A decisive daily close below this mark could signal additional weakness in the US dollar.

Meanwhile, President Trump’s recent decision to raise steel and aluminum tariffs injects fresh uncertainty into Canada’s economic outlook. As a leading exporter of both metals to the U.S., Canada could see mounting pressure, potentially dampening broader market sentiment. However, the CAD has largely shrugged off these sector-specific levies, showing little reaction to their immediate impact.

High bar for sustained dollar weakness

George Vessey – Lead FX & Macro Strategist

The initial boost to the US dollar from the Federal Trade Court’s ruling against Trump’s tariffs quickly faded as a federal appeals court granted a stay on the ruling until 9 June, keeping tariffs in place for now. Moreover, markets shifted focus to Section 899 of the “One Big, Beautiful Bill” as US policy uncertainty remains a key overhang.

Adding to renewed trade tensions with China, this could be another growing challenge for the US dollar. Section 899, if passed through the Senate, would allow the US to tax companies and investors from countries deemed to have “unfair foreign taxes”, such as digital services taxes or rules on under-taxed profits. This could effectively act as a capital account tax, at a time when investor confidence in US assets is already shaky. A policy that reduces foreign investors’ returns on US holdings would likely dampen capital inflows, further driving away foreign investors from US assets, including the dollar, already weakened by Trump’s unpredictable trade moves and worsening fiscal conditions.

However, there are still uncertainties around the bill’s final form. It has yet to clear the Senate, and key details remain unresolved. First, it’s unclear if income from US Treasuries will be exempt. Second, S899 would primarily target countries like the EU, UK, Australia, and Canada, while Middle Eastern and Asian nations, home to large global reserves, are seemingly excluded.

Market positioning already reflects broad scepticism toward the dollar, but the scale of additional bearish shifts may be constrained. Traders remain focused on tariff developments, fiscal policy, and global trade negotiations, but much of the negative USD sentiment may be priced in. The dollar’s direction this week will continue to be driven by developments with the court ruling on tariffs, but a slew of economic data will also be key. The May jobs report on Friday will be closely watched, especially for signs of Liberation Day’s impact on hiring and whether DOGE spending cuts are starting to weigh on federal employment.

Euro’s path hinges on ECB and market momentum

George Vessey – Lead FX & Macro Strategist

The European Central Bank’s (ECB) upcoming meeting on Thursday is drawing attention, as recent developments in trade and tariffs have slightly increased the possibility of a pause. However, a downward revision to inflation forecasts and the earlier-than-expected drop in headline inflation to below 2% suggest that the balance is tilting toward a 25 basis-point rate cut. Inflation risks continue to weigh on the outlook, reinforcing expectations for monetary easing.

Eurozone inflation data due on Tuesday is expected to show a decline to 2.0% in the headline print for May. This drop is largely due to falling energy prices and a reversal of last month’s core inflation spike, which had been inflated by Easter-related holiday and leisure costs. With core inflation likely returning to 2.5%, policymakers may see further justification for easing. A rate cut could exert downward pressure on the euro, though much depends on how aggressively markets price in future ECB policy moves.

A dovish ECB, combined with cooling trade tensions and legal battles, could drive EUR/USD lower in the near term. However, the pair has reclaimed its 21-day moving average, which is starting to slope upward, suggesting positive momentum may be rebuilding for the euro. The options market and positioning trends indicate that traders are still favouring euro strength, though short-term volatility remains a risk.

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

The initial boost to the US dollar from the Federal Trade Court’s ruling against Trump’s tariffs quickly faded as a federal appeals court granted a stay on the ruling until 9 June, keeping tariffs in place for now. Moreover, markets shifted focus to Section 899 of the “One Big, Beautiful Bill” as US policy uncertainty remains a key overhang.

Adding to renewed trade tensions with China, this could be another growing challenge for the US dollar. Section 899, if passed through the Senate, would allow the US to tax companies and investors from countries deemed to have “unfair foreign taxes”, such as digital services taxes or rules on under-taxed profits. This could effectively act as a capital account tax, at a time when investor confidence in US assets is already shaky. A policy that reduces foreign investors’ returns on US holdings would likely dampen capital inflows, further driving away foreign investors from US assets, including the dollar, already weakened by Trump’s unpredictable trade moves and worsening fiscal conditions.

However, there are still uncertainties around the bill’s final form. It has yet to clear the Senate, and key details remain unresolved. First, it’s unclear if income from US Treasuries will be exempt. Second, S899 would primarily target countries like the EU, UK, Australia, and Canada, while Middle Eastern and Asian nations, home to large global reserves, are seemingly excluded.

Market positioning already reflects broad scepticism toward the dollar, but the scale of additional bearish shifts may be constrained. Traders remain focused on tariff developments, fiscal policy, and global trade negotiations, but much of the negative USD sentiment may be priced in. The dollar’s direction this week will continue to be driven by developments with the court ruling on tariffs, but a slew of economic data will also be key. The May jobs report on Friday will be closely watched, especially for signs of Liberation Day’s impact on hiring and whether DOGE spending cuts are starting to weigh on federal employment.

Euro’s path hinges on ECB and market momentum

George Vessey – Lead FX & Macro Strategist

The European Central Bank’s (ECB) upcoming meeting on Thursday is drawing attention, as recent developments in trade and tariffs have slightly increased the possibility of a pause. However, a downward revision to inflation forecasts and the earlier-than-expected drop in headline inflation to below 2% suggest that the balance is tilting toward a 25 basis-point rate cut. Inflation risks continue to weigh on the outlook, reinforcing expectations for monetary easing.

Eurozone inflation data due on Tuesday is expected to show a decline to 2.0% in the headline print for May. This drop is largely due to falling energy prices and a reversal of last month’s core inflation spike, which had been inflated by Easter-related holiday and leisure costs. With core inflation likely returning to 2.5%, policymakers may see further justification for easing. A rate cut could exert downward pressure on the euro, though much depends on how aggressively markets price in future ECB policy moves.

A dovish ECB, combined with cooling trade tensions and legal battles, could drive EUR/USD lower in the near term. However, the pair has reclaimed its 21-day moving average, which is starting to slope upward, suggesting positive momentum may be rebuilding for the euro. The options market and positioning trends indicate that traders are still favouring euro strength, though short-term volatility remains a risk.

Pound’s rally faces key tests

George Vessey – Lead FX & Macro Strategist

Sterling edged lower to $1.35, retreating from its three-year high of $1.3593 on May 26, as investors reassessed growth prospects and trade dynamics. In tandem, GBP/EUR pulled back from near €1.20, with traders shifting toward the euro amid global trade tensions and rising FX volatility.

Recent soft US economic data, including a Q1 contraction and higher jobless claims, has strengthened expectations for two Fed rate cuts by early 2026, creating a potentially supportive backdrop for GBP/USD. However, lingering global uncertainty and UK-specific factors remain key for near-term direction. The BoE’s cautious approach reflects resilient UK data, with strong April retail sales, improved consumer confidence in May, and sticky inflation.

Markets are pricing 54bp of BoE cuts over 12 months, compared to 60bp from the ECB, leaving a policy gap of around 200bp in the UK’s favor. The recent stabilization in risk sentiment has pushed GBP/EUR toward levels consistent with rate differentials and VIX, though modest further upside remains possible.

For GBP/USD, staying above its 21-day and long-term moving averages suggests the uptrend remains intact. With four consecutive monthly gains, further upside could materialize—especially if investors continue reducing dollar exposure amid US policy uncertainty. A move toward $1.40 in H2 2025 remains on the radar, contingent on macro drivers aligning.

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

Asia FX mostly lower on US-China worries

The Australian dollar and most regional FX markets were weaker on Friday after US President Donald Trump said China has “totally violated” last month’s tariff-pause agreement.

Posting on Truth Social, Trump’s commentary sparked fears of another round of escalation in US-China trade negotiations. A follow-up statement from the Trump administration said the talks were now “a bit stalled”.

That said, the reaction in FX markets was mostly moderate.

The AUD/USD was down 0.2% while NZD/USD fell less than 0.1%.

The USD/SGD gained 0.3% while USD/CNH gained 0.2%.

Friday’s action brings to a close a momentous month in financial markets although FX markets were more muted.

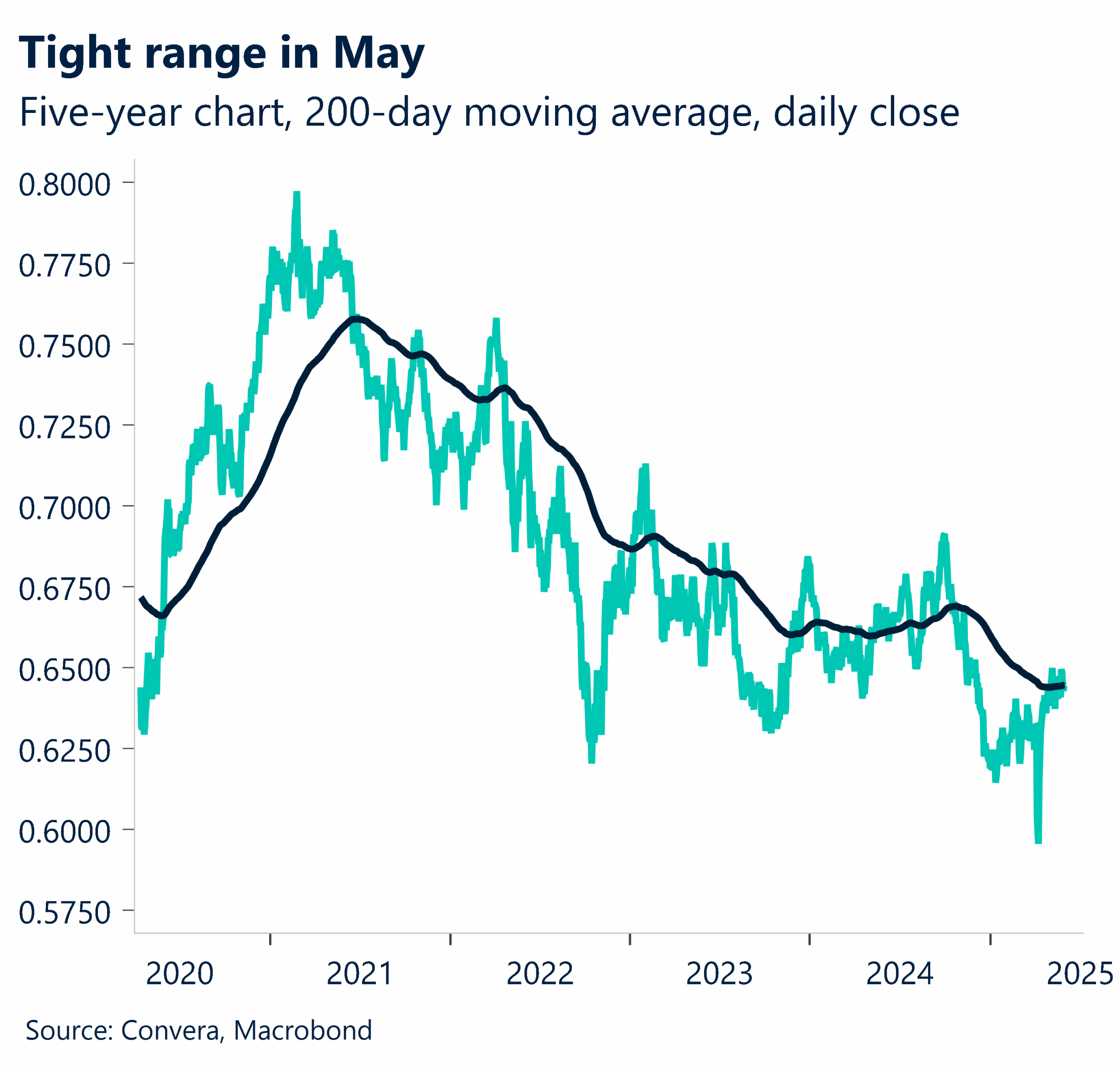

The Aussie’s 2.8% trading range in May was the tightest trading range since June 2024.

Trump’s team develops a backup plan to apply tariffs

According to the Wall Street Journal, which cited unnamed sources, the US administration is contemplating a temporary attempt to impose tariffs under a never-before-used provision of the Trade Act of 1974 that includes language permitting tariffs of up to 15% for 150 days in order to address trade imbalances with other nations.

Then, under a separate section of the same bill, President Donald Trump would have more time to create customized tariffs for each of his main trading partners.

Although the second step necessitates a protracted notification and discussion procedure, administration officials believe it is more legally sound than the tariff policy that was declared unlawful this week.

Trump’s initial tariffs on China were one of the numerous instances in which the alternate provision was employed.

Looking forward, we’d be prepared for more FX volatility in the coming months.

For USD/SGD, the next key resistance lies with 21-day EMA of 1.2953, and 50-day EMA of 1.3082 next.

A week focused on growth and inflation metrics

The upcoming week features a relatively heavy economic calendar, with inflation and growth metrics taking centre stage. Highlights include Eurozone preliminary CPI data on Tuesday night, Australia’s Q1 GDP on Wednesday morning, and Canadian and US labor market data on Friday.

These events will provide critical insights into economic conditions and central bank policy direction.

Eurozone inflation data will dominate the early part of the week, with preliminary May CPI figures released on Tuesday night. These will help shape market expectations for the ECB’s policy decision on Thursday night. Inflation trends globally remain a key concern for policymakers and markets alike.

Midweek, all eyes will turn to Australia’s Q1 GDP figures, along with Germany’s factory orders and Eurozone growth metrics. These releases will give a clearer picture of the global growth trajectory. Thursday brings Australia’s trade balance data, while US Nonfarm Payrolls and Canada’s labor market report on Friday are expected to cap off the week.

The Bank of Canada rate decision on Wednesday will be a highlight for monetary policy watchers. Similarly, the ECB’s rate decision on Thursday will attract attention.

USD mostly higher in Asia

Table: seven-day rolling currency trends and trading ranges

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Tariffs off. A new twist in the global trade war story saw most of President Trump’s tariffs deemed illegal by a US trade court, ordering levies to be stopped within 10 days. This would reduce the effective US tariff rate to below 6% from a high of almost 27% last month.

Dollar up. The initial reaction was USD strength, whilst equities extended higher with the S&P500 up 1.6% this week primed for a more than 5% monthly advance.

Tariffs on. Less than 24 hours after, the White House appealed, and a federal appeals court temporarily paused the trade court’s ruling, which means that tariffs will stay in place – for now.

Dollar down. The dollar came under renewed selling pressure, suggesting traders were eager to align with the broader trend of de-dollarization. Investors had better buckle up for a turbulent summer.

Japan’s quick fix. In other news, Japan’s ministry of finance survey hints at reduced issuance, complicating global rate dynamics. Bond markets from Japan to the UK and US reacted positively, pushing prices up and yields down.

Yields relief. That paused the weeks-long bond selloff forced by investors demanding bigger yields as they braced for increased inflation and government spending caused by US Trump’s trade and tax policies.

Mixed macro. US consumer sentiment saw sharpest rise in four years but remains historically weak. Continuing jobless claims hit highest since 2021, and GDP in Q1 confirmed at -0.2%.

Global Macro Tariff twists and turns

More flip-flopping. Markets were caught off guard by President Trump’s latest tariff threats targeting Europe and Apple. However, past Sunday, President Trump agreed to push the deadline to July 9 following a phone call with European Commission President Ursula von der Leyen.

Tariffs are challenged. On Thursday, the US Court of International Trade ruled President Trump’s tariffs illegal, affecting fentanyl and immigration-related tariffs (10%–30%) on imports from China, Canada, and Mexico, as well as global trade surplus tariffs (10%+), with reciprocal tariffs suspended until 9 July. The ruling does not impact steel, aluminum (25%), auto, or auto parts tariffs. The administration has appealed, with the case likely headed to the Supreme Court to determine the legality of IEEPA-based tariffs.

Tariffs remain (for now). A federal appeals court granted a bid from the White House to temporarily suspend the lower court’s order though. The next hearing is on 5 June.

Japan bond market in focus. A recent survey by Japan’s Ministry of Finance suggests a potential reduction in bond issuance, introducing new complexities to market dynamics. Meanwhile, the Bank of Japan’s move toward policy normalization, ending yield curve control and possibly raising rates, poses risks to U.S. yields, as demand for new issuance can’t be given. Although global rates have declined through the week, under this evolving landscape, long-term yields are likely to stay elevated.

Mixed macro data. Consumer sentiment improved for the first time since November, with May’s Conference Board confidence index posting its sharpest rise in four years, though still at the lower end of the recent range. Meanwhile, US continuing jobless claims hit their highest level since 2021, pending home sales fell short of expectations, and Q1 2025 GDP contracted by -0.2%, slightly less than previously reported.

Week ahead Tariff drama could overshadow macro data

Focus on inflation and growth. The upcoming week features a relatively heavy economic calendar, with inflation and growth metrics taking centre stage. Key releases include Eurozone preliminary CPI data on Tuesday, Australia’s Q1 GDP on Wednesday morning, and Canadian and US labour market data on Friday. These events will provide critical insights into economic conditions and central bank policy direction.

Inflation in focus.Inflation data from the Eurozone will set the tone for the week. Preliminary May CPI releases are scheduled for Tuesday evening, and these figures will inform expectations for the European Central Bank’s (ECB) policy decisions later in the week. Markets will also monitor inflation-related data from the US and other regions for further clues on global price pressures.

Growth indicators from major economies.Growth remains a key theme, with GDP data from Australia (Q1) dominating the midweek schedule. Factory orders and industrial production figures from Germany will further shape the growth narrative, while US factory orders and durable goods data will offer insights into business activity. Canada and the US cap the week with labour market updates, including US Nonfarm Payrolls on Friday.

Central bank decisions. The Bank of Canada rate decision on Wednesday will be a highlight for monetary policy watchers. Similarly, the ECB’s rate decision on Thursday will attract attention with a 25-basis point cut baked into market pricing.

Tariff drama. For now, the appeals court decision allow Trump’s tariffs to be used while the case is litigated. The next hearing is on 5 June, whilst the Trump administration has been ordered to respond again by June 9. The matter is widely expected to end up at the Supreme Court. Broad uncertainty remains elevated, keeping investors on edge.

FX Views G10 strength on USD slide

USDDollar comes down from haven. The US dollar has seen a decline in its traditional safe-haven appeal, moving inversely to yields and the VIX. This suggests that despite current market volatility, the DXY is not being sought as a refuge, and higher yields are insufficient to attract investors, leading to capital outflows from US assets. Federal Reserve officials Kashkari and Williams reinforced the Fed’s “wait and see” stance this week, and the FOMC minutes echoed this sentiment, indicating that rate cuts are unlikely until there is greater clarity on tariffs and their impact on inflation. US durable goods orders fell by 6.3% in April, and the disappointing GDP release (-0.2% QoQ) confirmed the prevailing downbeat sentiment. Compounding this, the US Court of International Trade ruled late Wednesday that President Trump’s tariffs are illegal. While this ruling could provide some support for the dollar, the timing—coinciding with weak economic data—exacerbated market concerns, sending the DXY below 99.5. Looking ahead, the implications of this ruling remain uncertain. Earlier in the week, positive trade headlines had buoyed sentiment, raising hopes for policy improvements. The ruling could serve as a catalyst for more market-friendly policies, supporting the dollar, or conversely, prompt President Trump to shift focus toward imposing more aggressive tariffs on unaffected sectors.

EUR Euro momentum falters. Despite being the second most liquid alternative to the U.S. dollar, the euro has lost some traction this month, with EUR/USD slipping 0.1%, hovering around the $1.14 handle. Optimism surrounding the euro remains intact, particularly after ECB President Christine Lagarde’s “global euro moment” remarks, which have reinforced a euro-positive sentiment. However, soft German retail sales for April, disappointing PMI figures, and a weaker-than-expected CPI print from France highlight a lack of robust domestic macroeconomic support for the euro. The ECB maintains its dovish stance, with a rate cut expected on June 5, emphasizing growth over inflation. The key question now is whether deflationary risks will prove transitory or become more persistent, affecting future policy rate decisions. For now, markets are pricing in a 58bp rate cut from the ECB compared to 50bp from the Fed for the year, reinforcing the view that rate differentials alone should push EUR/USD lower while favoring the USD. Any further removal of risk premiums from the dollar—following eased trade tensions and recent legal battles—could see EUR/USD trading a leg lower in the near term.

GBP Homegrown momentum. Sterling’s 7.6% gain against the dollar this year may largely reflect broad USD weakness, but its lower beta to the DXY sets it apart from many G10 peers, making it less reactive to dollar declines. Beyond dollar dynamics, GBP sentiment has notably improved too though, driven by UK trade agreements, strong domestic economic data, and the BoE’s relatively hawkish stance. These factors reinforce sterling’s idiosyncratic strength, making its rally more than just a dollar story. Although GBP/USD has fallen from $1.36 towards $1.34 this week due to renewed dollar demand, the pair remains above its 21-day moving average and other long-term moving averages in a sign that the uptrend is still intact for now. Indeed, zooming out on a monthly chart, we note the currency pair is primed to clock its fourth monthly rise in a row having last month closed comfortably above its 100-month moving average for the fourth time in about ten years. This chart looks bullish, with upside potential of $1.40 a possibility later this year, particular if investors resume offloading dollar-denominated assets amidst ongoing US policy angst. Meanwhile, GBP/EUR, is trading 1.5% higher month-to-date and might be poised to test the €1.20 handle soon thanks largely to widening rate differentials and the UK’s better trade position with the US.

CHF Defiant but SNB on the brink. Despite the tariff ruling and equity market rally, EUR/CHF remains below 0.94, reflecting growing distrust in US Treasuries and concerns over the Swiss National Bank’s policy constraints. That said, USD/CHF has rallied over 1% over the past week after rebound off the 0.82 support. Looking ahead, the SNB faces a tough decision ahead of its June 19 meeting, with markets split between a 25bp or 50bp rate cut. While the central bank is reluctant to return to negative rates, it may have little choice given economic pressures. Additionally, investors expect the SNB to be more constrained in FX intervention, aligning with Washington’s directives. The key question remains whether the SNB can be dovish enough to ease EUR/CHF downside risks, especially if the ECB proceeds with two more rate cuts.

CNYManufacturing focus dominates new policy framework. China’s government is developing a comprehensive five-year plan targeting high-end technology manufacturing, particularly chip-making equipment production. The strategy aims to maintain manufacturing’s GDP share over the medium term, reflecting Beijing’s continued emphasis on industrial capacity expansion. The manufacturing-centric approach suggests policymakers prioritize export competitiveness over domestic demand rebalancing, potentially supporting yuan stability through trade surplus maintenance. USD/CNH remains below key psychological handle of 7.2000. The next key resistance levels for the pair will be 21-day EMA of 7.2109, 50-day EMA of 7.2385 and 200-day EMA of 7.2455. We do expect range-bound price action for this pair. It is still circa 3% from its all-time highs of 7.4290. Market participants will closely watch upcoming Chinese manufacturing PMI, non-manufacturing PMI, Caixin manufacturing PMI, and Caixin Services PMI for economic momentum insights.

JPY Bond market tensions drive range-bound trading. Japan’s Ministry of Finance is considering adjustments to its bond issuance composition, potentially reducing super-long debt offerings amid record-high yields and declining institutional demand. Life insurers, traditionally major buyers, have reduced appetite for ultra-long duration bonds. The MoF will likely decide by mid-to-late June, having surveyed market participants about appropriate issuance volumes. USD/JPY has failed to break the psychological level of 145, after having touch recent highs of 146.28. USD/JPY has established a new trading range following recent volatility. The technical setup suggests consolidation below the 149.11 200-day moving average, while maintaining support above the crucial 140 level. Next key resistance barriers for the pair include 21-day EMA of 144.45 and 50-day EMA of 145.53. Market participants will focus on upcoming capital spending data, household spending figures, and au Jibun Bank Services PMI for economic activity confirmation.

CADBounce from 2-year average. The USD/CAD has retreated about 6.6% from its 2025 high of 1.479, though it remains up approximately 4% year-to-date. Over the past month, the pair has been largely driven by persistent dollar weakness, further supported by investor relief following developments on tariffs and the U.S. tax bill. These factors prompted a shift away from the greenback, leading the USD/CAD to hit 1.368—its lowest level in eight months—before rebounding above 1.38 as fiscal concerns eased. Despite weakening domestic fundamentals and lingering global uncertainty, USD/CAD has stabilized after bouncing off its two-year average, finding key support at 1.37. This level coincides with a year-long trendline dating back to June 2021, reinforcing medium-term uptrend support. The recent recovery to 1.38 was influenced by oversold conditions, U.S.-Canada bond yield differentials, and renewed dollar strength. From a technical standpoint, the Loonie remains unable to close below its 100-week simple moving average (SMA) at 1.375, reinforcing its current range-bound trading pattern. If USD/CAD holds above 1.381, it could signal the end of its three-month decline. Additionally, the 60-day SMA is approaching a crossover below the 200-day SMA, setting up a key resistance zone near 1.40.

AUD Inflation progress stalls near critical technical junction. Australia’s headline CPI in April printed 2.4% y/y, higher than estimates of 2.3% but still tracking below the RBA’s inflation target midpoint of 2.5%. Trimmed mean CPI was 2.8%, up from 2.7% in March, suggesting underlying price pressures remain elevated. Several CPI lead indicators have recently rebounded, with business surveyed selling prices and the inflation gauge both rising back above 3% y/y, indicating potential stickiness in the disinflation process. AUD/USD has already gained circa 8%+ since rebounding from April 9 lows of 0.5915. AUD/USD continues to hover at its strong 21-day EMA as key support. A decisive break below 50-day EMA of 0.6385 would likely trigger an impulsive move lower, potentially targeting the next support confluence of 0.6200. A decisive break above key psychological resistance of 0.6500 will augur well for the pair. Market participants will monitor upcoming current account data, RBA meeting minutes, GDP figures, and trade balance for further policy guidance.

MXN Peso rally stalls. Banco de Mexico (Banxico) released this week its quarterly economic forecast, painting a cautious picture with clear downside risks to growth. GDP projections for 2025 took a sharp hit, falling well below market expectations. Governor Victoria Rodríguez Ceja announced that Mexico’s GDP is now expected to grow only 0.1% in 2025, down from a previous estimate of 0.6%. The 2026 outlook was also revised downward, from 1.8% to 0.9%, with Banxico citing a combination of internal economic weakness and global challenges, particularly shifts in U.S. trade policy, as key factors adding uncertainty to Mexico’s external demand. The Mexican peso reacted negatively to Banxico’s dovish tone. After three consecutive weeks of gains, momentum has lost steam and the USD/MXN has found support just above its 60-week SMA at 19.2, rebounding from weekly and 2025 lows at 19.18, though still below its five-year average of 19.5. A push to retest 2025 lows will require fresh momentum and weaker dollar. Banxico’s reluctance to signal a more aggressive easing cycle has kept market expectations anchored around a terminal rate near 6.5%, leaving carry-erosion concerns unchanged. In the near term, with the dollar strengthening across the board, the peso’s range is likely to hover between 19.2 and 19.4. The Mexican peso has staged a solid comeback, appreciating 9% from its yearly high of 21.2. After a rough 2024, where it tumbled nearly 20% from its low of 16.2, the currency has rebounded, posting a year-to-date gain of approximately 7% against the U.S. dollar.

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Another whirlwind week in US trade policy. Markets were caught off guard by President Trump’s latest tariff threats aimed at Europe and Apple, but by Sunday, he agreed to push the deadline to July 9 after speaking with European Commission President Ursula von der Leyen. Then, the US Court of International Trade ruled his tariffs illegal—impacting fentanyl, immigration-related tariffs (10%–30%) on imports from China, Canada, and Mexico, as well as global trade surplus tariffs (10%+). Hours later, a federal appeals court hit pause on that ruling, likely sending the case to the Supreme Court to determine the legality of IEEPA-based tariffs.

This renewed uncertainty sent the dollar lower, compounded by weaker-than-expected US economic data. Pending home sales missed expectations, and continuing jobless claims hit their highest level since 2021, suggesting it’s taking longer for people to find jobs.

The dollar initially spiked in Asian trading after the trade court’s ruling but lost momentum during the American session, slipping against all G10 peers, most notably the euro and Nordic currencies.

While this might be just the beginning of yet another chapter in the US trade policy, the turbulence is further chipping away at confidence in the broader US economic outlook. Positioning remains bearish on the dollar over the next three months, as reflected in 3-month risk reversals.

Sideways momentum holds strong

Kevin Ford – FX & Macro Strategist

The USD/CAD has retreated about 6.6% from its 2025 high of 1.479, though it remains up approximately 4% year-to-date. Over the past month, the pair has been largely driven by persistent dollar weakness, further supported by investor relief following developments on tariffs and the U.S. tax bill. These factors prompted a shift away from the greenback, leading the USD/CAD to hit 1.368, its lowest level in eight months, before rebounding above 1.38 as fiscal concerns eased.

On the domestic macro front, markets are keeping an eye on Canada’s first-quarter GDP figures, set to be released today. The economy is expected to have grown 1.6% year-over-year in the first quarter. Meanwhile, traders remain unsure whether the Bank of Canada will go for another rate cut next week, with current odds sitting at 25%, based on Overnight Index Swaps.

Despite weakening domestic fundamentals and lingering global uncertainty, USD/CAD has stabilized after bouncing off its two-year average, finding key support at 1.37. This level coincides with a year-long trendline dating back to June 2021, reinforcing medium-term uptrend support.

The recent recovery to 1.38 was influenced by oversold conditions, U.S.-Canada bond yield differentials, and momentary dollar strength. From a technical standpoint, the Loonie remains unable to close below its 100-week simple moving average (SMA) at 1.375, reinforcing its current range-bound trading pattern. If USD/CAD holds above 1.381, it could signal the end of its three-month decline. Additionally, the 60-day SMA is approaching a crossover below the 200-day SMA, setting up a key resistance zone near 1.40.

Euro’s upside momentum wanes

Antonio Ruggiero – FX & Macro Strategist

The euro rally has lost some momentum, with EUR/USD down 0.1% month-to-date, and hedge funds trimming their top-side exposure – effectively scaling back the most aggressive bullish bets on the pair. Despite this pullback, ongoing uncertainties in Washington continue to favor the euro, the latest being a federal appeals court’s temporary stay on a ruling regarding Trump’s global tariffs, adding another layer of complexity to the trade dispute. Further boosting the euro, Thursday’s disappointing US jobless claims and GDP figures helped the currency close yesterday’s session higher.

Despite legal turbulence, trade negotiations remain active behind the scenes. The US administration has accelerated discussions with the EU, with Brussels proposing a “zero-for-zero” tariff arrangement on industrial goods, including automobiles. The EU is also open to increasing imports of US products such as soybeans, liquefied natural gas, and defense equipment. Meanwhile, Trump is pushing for revisions to non-tariff barriers, including food safety regulations and digital services taxes, which his administration considers obstacles to fair trade. While the exact contours of a deal remain unclear, both sides appear eager to make progress.

The impact of a potential agreement on EUR/USD price action remains uncertain. On one hand, reduced trade barriers and increased demand for European goods could support the euro. On the other, a reassessment of US growth prospects and decreased uncertainty could remove additional risk premium from the dollar, forcing the euro to realign with its rate differentials—potentially weighing on the currency.

Sterling’s winning streak faces summer test

George Vessey – Lead FX & Macro Strategist

Sterling is on track for its fourth monthly rise on the trot versus the US dollar, its longest monthly winning streak in over two years with a cumulative gain of over 10%. Historically, GBP/USD has suffered a down month following such an aggressive move higher. But we note that June exhibits no meaningful seasonality trend and with dollar demand tepid amidst ongoing uncertainty regarding the US trade story and fiscal policy stability – the pound could extend higher into the summer.

Our upside scenario of $1.40 before year-end assumes the “sell America” trade continues, supported not just by the erosion of confidence in US policy making but also by deteriorating US economic data. Moreover, such an uplift would require a resilient UK economy and more hawkish signals from the Bank of England, hence inflation data will be crucial. In the very near term though, month-end flows could create some temporary selling pressure for sterling, given its strong month-to-date performance across both an aggregate and cross-border basis.

When it comes to GBP/EUR, although the pair has pulled back by about a cent from this week’s highs following the increase in FX volatility in the wake of renewed tariff uncertainty, the pair is likely to snap a 2-month losing streak which at one point saw the pair drop to an 18-month low near €1.14. Now the pound is perched closer to “fair value” versus the euro as indicated by UK-German rate differentials and it also sits around 2% higher than its 5-year average.

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quothave a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

From renewed trade tensions to bond market jitters, investors continue to navigate a volatile mix of geopolitical uncertainty and macroeconomic shifts. The United States remains central to this fragile sentiment, with unpredictable policy developments rattling markets and challenging expectations around currency movements.

Is your business prepared to weather this ongoing storm? Download our Global FX Outlook for June to uncover the key forces shaping currency markets, with a focus on rising fiscal concerns, evolving trade dynamics, and a market increasingly uncertain about the value of the US dollar.

US dollar momentum undermined by policy turbulence

The US dollar staged a brief comeback in April, recovering nearly 4% from a three-year low. A temporary reduction in US-China tariffs revived risk appetite and saw a rebound in global equities, but the optimism was short-lived. President Trump’s surprise threat of a 50% tariff on EU imports, later delayed to July, reignited fears of a trade war.

Meanwhile concerns around bond markets are growing. Moody’s downgrade of the US credit rating and mounting concerns about America’s fiscal outlook have pushed long-term treasury yields higher. This typically leads to a stronger currency, however US yields and the USD have decoupled over the past two months, offering further evidence of fading confidence in US assets.

Diverging fortunes: EUR, GBP, and AUD

The euro continues to move in tandem with US sentiment. Following a correction from three-year highs, EUR/USD climbed back above $1:13. Sterling, however, stood out from its G10 peers to hit its highest level against the dollar since 2022. The pound’s strength is underpinned by resilient UK economic data, improved trade relations, and the Bank of England’s hawkish stance.

The Australian dollar remains in a narrow trading range, cushioned by robust trade conditions and a stable Chinese yuan. Despite a dovish Reserve Bank of Australia, the AUD/USD is finding support between 0.63 and 0.65.

Key market themes

Tariffs a silver lining for the USA?

The US collected $48.1 billion in tariff revenues by late May; a 67% increase compared to last year. While this surge might look promising, it pales in comparison to the $2.4 trillion collected via federal income taxes in 2024. Tariffs may provide short-term revenue relief but are unlikely to comfortably offset the lost tax revenue. A clearer picture of the policy’s impact will take shape in the coming months.

Surging bond yields unwelcome

Bond markets appear to be in retreat globally, not just in the US. Yields on Japan’s 40-year bonds and the UK’s 30-year bonds are near multi-decade highs. The sharp rise in long-term yields is typically a sign of optimism but is now more reflective of fiscal concerns which are driving the dollar’s depreciation.

Resilience or data distortions?

Surprisingly positive economic data across most major economies (excluding Canada and Japan) has dampened recession fears. However, this data is likely distorted by a run of tariff front-loading boosting short-term activity and painting a misleading picture of economic strength.

Fiscal on the forefront

The global trade war remains a key theme to watch, with the renewed standoff between the US and EU emphasizing that tariff threats and delays can quickly re-emerge and ignite volatility.

Another significant theme in this month’s report is fiscal policy and US debt dynamics. The US deficit stood at 6% of GDP in 2024, but projections suggest it could approach 9% by 2035. A proposed tax cut bill was met with scepticism, and combined with Moody’s downgrade and rising borrowing costs, the outlook is increasingly challenging.

This fiscal pressure is contributing to a broader structural shift. As the world diversifies away from dollar-denominated assets, the inverse relationship between US yields and the dollar becomes more pronounced. Higher yields are no longer translating into dollar strength and are instead highlighting that investors are reluctant to bet on US creditworthiness.

Watch a recap of the Global FX Outlook for June

Watch our Market Insights team give an overview of our Global FX Outlook for June, including the growing dislocation between traditional market drivers and current investor behavior.

Fiscal concerns, erratic policymaking, and trade tensions are reconfiguring expectations across currencies, bond markets and global trade flows. For companies managing cross-border payments and volatile currency markets, agility and insight have never been more critical. Now is the time to rethink assumptions and prepare your business to navigate this rapidly changing environment.

Download our Global FX outlook for June and leverage deep analysis, currency forecasts, and insights that can help you manage international trade with confidence.

Want more insights on the topics shaping the future of cross-border payments? Tune in to Converge, with new episodes every Wednesday.

Markets were caught off guard by President Trump’s latest tariff threats aimed at Europe and Apple, but by Sunday, he agreed to push the deadline to July 9 after speaking with European Commission President Ursula von der Leyen. Then, the US Court of International Trade ruled his tariffs illegal—impacting fentanyl, immigration-related tariffs (10%–30%) on imports from China, Canada, and Mexico, as well as global trade surplus tariffs (10%+). Hours later, a federal appeals court hit pause on that ruling, likely sending the case to the Supreme Court to determine the legality of IEEPA-based tariffs.

This renewed uncertainty sent the dollar lower, compounded by weaker-than-expected US economic data. Pending home sales missed expectations, and continuing jobless claims hit their highest level since 2021, suggesting it’s taking longer for people to find jobs.

The dollar initially spiked in Asian trading after the trade court’s ruling but lost momentum during the American session, slipping against all G10 peers, most notably the euro and Nordic currencies.

While this might be just the beginning of yet another chapter in the US trade policy, the turbulence is further chipping away at confidence in the broader US economic outlook. Positioning remains bearish on the dollar over the next three months, as reflected in 3-month risk reversals.

Euro’s upside momentum wanes

Antonio Ruggiero – FX & Macro Strategist

The euro rally has lost some momentum, with EUR/USD down 0.1% month-to-date, and hedge funds trimming their top-side exposure – effectively scaling back the most aggressive bullish bets on the pair. Despite this pullback, ongoing uncertainties in Washington continue to favor the euro, the latest being a federal appeals court’s temporary stay on a ruling regarding Trump’s global tariffs, adding another layer of complexity to the trade dispute. Further boosting the euro, Thursday’s disappointing US jobless claims and GDP figures helped the currency close yesterday’s session higher.

Despite legal turbulence, trade negotiations remain active behind the scenes. The US administration has accelerated discussions with the EU, with Brussels proposing a “zero-for-zero” tariff arrangement on industrial goods, including automobiles. The EU is also open to increasing imports of US products such as soybeans, liquefied natural gas, and defense equipment. Meanwhile, Trump is pushing for revisions to non-tariff barriers, including food safety regulations and digital services taxes, which his administration considers obstacles to fair trade. While the exact contours of a deal remain unclear, both sides appear eager to make progress.

The impact of a potential agreement on EUR/USD price action remains uncertain. On one hand, reduced trade barriers and increased demand for European goods could support the euro. On the other, a reassessment of US growth prospects and decreased uncertainty could remove additional risk premium from the dollar, forcing the euro to realign with its rate differentials—potentially weighing on the currency.

Sterling’s winning streak faces summer test

George Vessey – Lead FX & Macro Strategist

Sterling is on track for its fourth monthly rise on the trot versus the US dollar, its longest monthly winning streak in over two years with a cumulative gain of over 10%. Historically, GBP/USD has suffered a down month following such an aggressive move higher. But we note that June exhibits no meaningful seasonality trend and with dollar demand tepid amidst ongoing uncertainty regarding the US trade story and fiscal policy stability – the pound could extend higher into the summer.

Our upside scenario of $1.40 before year-end assumes the “sell America” trade continues, supported not just by the erosion of confidence in US policy making but also by deteriorating US economic data. Moreover, such an uplift would require a resilient UK economy and more hawkish signals from the Bank of England, hence inflation data will be crucial. In the very near term though, month-end flows could create some temporary selling pressure for sterling, given its strong month-to-date performance across both an aggregate and cross-border basis.

When it comes to GBP/EUR, although the pair has pulled back by about a cent from this week’s highs following the increase in FX volatility in the wake of renewed tariff uncertainty, the pair is likely to snap a 2-month losing streak which at one point saw the pair drop to an 18-month low near €1.14. Now the pound is perched closer to “fair value” versus the euro as indicated by UK-German rate differentials and it also sits around 2% higher than its 5-year average.

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

Tariff reprieve gives markets temporary relief

The greenback weakened as the US appeals court temporarily suspended Trump tariff blockade, though headline risk remains elevated heading into the weekend.

The USD index fell 0.5% to 99.30 as markets faded overnight gains following concerning US jobless claims data and downward Q1 GDP revisions.

The Japanese yen gained ground with USD/JPY sliding from 145.00 to 144.21 close.

In Europe, EUR/USD jumped to 1.1350 after weak US data, topping out near 1.1385 before settling at 1.1370 by close.

In Asia, SGD gains 0.18% while CNH was flat overnight.

Powell tells Trump policy path depends on data, outlook

The Fed said Chairman Powell and President Trump met at the White House on Thursday.

They discussed growth, employment and inflation with Powell stressing the Fed’s path depends on the data and outlook.

Powell said the Fed would set its path solely on objective, non-political analysis.

From technical lens for risk-sensitive currencies like AUD/USD, it is still hovering on 21-day EMA as key support.

Next key strong psychological handle to break will be the 0.6500 handle.

Trump and Japanese Prime Minister Ishiba speak

According to Japanese Prime Minister Ishiba, he held a 25-minute conversation with US President Trump. He claimed that they discussed economics, security, and diplomacy.

He said that before the G7 summit, he had offered to travel to the US.

Overall, he claimed that their desire to produce a win-win solution had not changed.

Looking at USD/JPY, it failed to break 21-day EMA resistance of 144.44, with 50-day EMA of 145.52 resistance barrier to break next.

Antipodeans strengthen on dollar weakness

Table: seven-day rolling currency trends and trading ranges

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Nicola Goose kickstarts her day like most people based in the UK – with a good, old-fashioned cup of tea. “Nothing beats it!” she says, settling into a day’s work as a Product Marketing Specialist.

Nicola joined Convera’s Bids team six years ago, working on requests for tenders and other proposals in support of the company’s new business efforts. It was a role that instilled Nicola with a deep understanding of Convera’s core business and the market landscape. When an opportunity arose to challenge herself by joining a new team, Nicola jumped at the chance.

“The Bids team recently became part of the wider Brand & Growth organization here at Convera, which gave me a deeper insight into other functions within the business. I realized that my skills as a bids professional could also be applied to other areas, which was exciting,” said Nicola.

“An opportunity came up on the Product Marketing team supporting a new segment, and I decided to apply. The idea of being able to flex my creative muscles developing strategies for approaching this new segment was really appealing, and now here I am on a new team!”

Communicating across borders

The global nature of the Product Marketing role was another appealing factor for Nicola, who thrives on building relationships with colleagues around the world while also working cross functionally.

“The nature of this role means that my days can vary greatly,” Nicola elaborated. “After my first cup of tea for the day, I might find myself on calls with people on the other side of the world discussing the competitive landscape in their region. Other days I’ve got my head down developing email marketing campaigns or reviewing website content.”

When asked what skill serves her best as a product marketing specialist, Nicola says that being able to communicate clearly with teams cross-functionally is essential.

“Stakeholder management plays a large role in what I do, and working cross-functionally means there are often lots of contrasting opinions in one room. Clear communication is an important part of being able to navigate these conversations, keep them on track, and come away with actionable tasks that keep programs running smoothly.”

“I also think it’s important not to be afraid to ask for support – I may not be new to the business, but I am new to the function. There are a lot of things I still need to learn, and my skills will only grow if I show curiosity and ask questions.”

Tackling websites and marathons

When it comes to new skills, Nicola is challenging herself every day working on a range of projects. From competitive analysis of new strategic markets, to developing frameworks to help go-to-market teams retain and grow revenue, Nicola takes on every task with aplomb.

“Right now, I’m entrenched in a cross-functional project that involves defining messaging and content for our website refresh. This has been an exciting challenge for me because it’s so different to the projects I worked on in my previous role. And yet, I still find I’m drawing on those skills to help achieve these new objectives.”

Outside of work, Nicola tackles life with the same gusto she brings to the office. “I love to stay busy,” she says. “Fitness is important to me, and I also enjoy trying new foods, so I do a lot of running. I recently trained for a half marathon which is something I’m proud to have tackled and achieved.”

“I’m a mum with a toddler who keeps me on my toes, and I’m planning a wedding, so life is busy. I also love being creative, pushing my limits and discovering what I am capable of. I was a competitive all-star cheerleader for 10 years, which is something that might surprise people!”

The future is bright at Convera

When asked what she values most about working at Convera, Nicola talks about the people and the excitement of what’s on the horizon.

“The people are what truly makes Convera. The environment is so supportive, people really want the best for you. We’re all working towards a common goal, reshaping this organization for the future. Everyone has put in a lot of hard work, and now we’re seeing the outcome of that which is super inspiring.”

“If I had to sum up my experience at Convera, I’d say that my role is always exciting, challenging in a good way, and definitely rewarding.” Are you interested in shaping the future of commercial payments at Convera? Visit our careers page to find a role near you.

Want more insights on the topics shaping the future of cross-border payments? Tune in toConverge, with new episodes every Wednesday.