Broadcom is expected to report fiscal first-quarter results after the market closes Thursday.

Analysts are widely bullish on the chipmaker’s stock despite recent losses.

Broadcom shares have lost about one-quarter of their value since hitting an all-time high in December.

Broadcom (AVGO) is set to report fiscal first-quarter results after the market closes Thursday, with analysts widely bullish on the chipmaker’s stock despite recent losses.

All but one of the 13 analysts covering the stock tracked by Visible Alpha have issued a “buy” or equivalent rating, with one “hold” rating. Their consensus price target of $259 would suggest about 30% upside from Friday’s closing price at $199.45.

Broadcom is expected to report revenue of $14.61 billion, up 22% year-over-year, and adjusted net income of $7.39 billion, up from $5.25 billion a year earlier.

Or so you might believe based on the sentiment indicators.

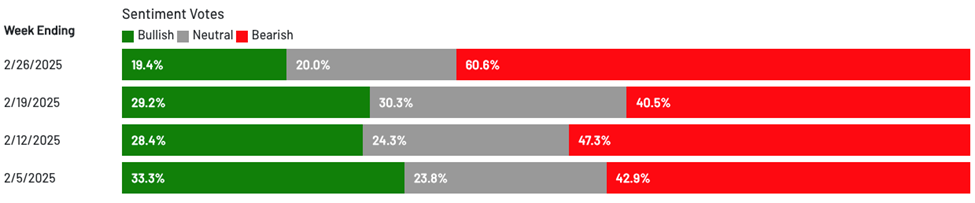

The latest AAII Sentiment Survey showed only 19.4% of respondents are bullish. This was the sixth time in eight weeks the reading came in below the historical average of 37.5%.

Here are the results from the last four weeks:

Meanwhile, the Conference Board Consumer Confidence Index showed a rise in consumer pessimism. The Expectations Index (based on consumers’ short-term outlook for income, business, and labor market conditions) dropped 9.3 points to 72.9. From their press release:

For the first time since June 2024, the Expectations Index was below the threshold of 80 that usually signals a recession ahead.

The survey also showed that 27% of consumers expect business conditions to worsen over the next six to 12 months, the highest since June 2022.

Looking at this data could spook any investor, leading to a classic investing mistake.

However, investors who can keep their heads can profit no matter what the crowd is doing, and I’m going to share an opportunity today.

Profiting by Separating Feelings from Data

Last week I wrote about the Iron Law of the Stock Market: If a company massively grows its sales and earnings, its stock price will grow, too.

Today, investor sentiment is low, but the earnings data tells a different story.

According to FactSet:

77% of S&P 500 companies exceeded earnings per share (EPS) estimates – equal to the five-year average of 77%.

The S&P 500 reported growth in earnings of 17.8% – the highest growth since Q4 of 2021.

No wonder the market hit an all-time high just a week ago.

And amid all the concern about inflation reigniting, yesterday, we learned the Personal Consumer Expenditures Index is 2.5%, down from 2.6% in December.

Regardless of the numbers, herd mentality takes over when sentiment turns negative, causing investors to react without thinking.

Here is what legendary investor Louis Navellier, editor of Growth Investor, has written about this classic investing mistake.

A lot of you are probably fans of momentum investing. The truth is, I am, too. You always want to capitalize on a trend, and trends are made up of people.

But while following the crowd CAN result in great momentum plays… you don’t want to do so blindly.

The crowd-seeking I’m talking about – follow the herd, think later – is responsible for a lot of failed investments. It means you won’t pick up on a shift in the trend. Thus, you’ll get your timing all wrong. You’ll often end up buying near the highs and selling near the lows.

Taking our natural biases out of the equation is at the heart of Louis’ quantitative stock picking system.

A Quality Stock on Sale

When market fear is high, savvy investors start to look for superior stocks that are on sale. That doesn’t necessarily mean cheap stocks. It means great companies selling at reasonable prices, resulting in good value.

Warren Buffett once encapsulated this idea in his usual folksy way, saying:

It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

In Louis’ system, that means stocks growing sales, operating margins, and especially earnings. When a stock like that experiences a sell-off… then that’s a great opportunity.

This week, one of Louis’ Growth Investor stocks, Vistra Corp. (VST), reported outstanding earnings…and still took a hit from the market.

Here is Louis’ summary of its earnings report.

Vistra Corp. (VST) noted that 2024 was not only a “record year but a transformational one” for the company. Full-year earnings soared 88.5% year-over-year to $2.81 billion, compared to $1.5 billion in fiscal year 2023. Revenue rose 16.5% year-over-year to $17.22 billion, topping estimates for $17.15 billion.

For the fourth quarter, Vistra reported earnings of $490.0 million, up from a loss of $184.0 million in the same quarter a year ago.

Below is a screenshot of how the stock rates in Louis’ system. Despite outstanding earnings, the stock took a hit at the end of the week.

But you can also see that the stock is still an “A” in Louis’ Stock Grader system.

As I write Friday morning, Vistra is up more than 140% since Louis recommended exactly one year ago.

And it’s still below his “buy below” price, and that means Louis believes there is a lot more room left for growth!

Keith Kaplan, the CEO of our corporate partner TradeSmith also is a big fan of using data to invest wisely.

His own experience of allowing emotions to drive his investment decisions led him to develop computer systems that can pinpoint the right time to buy and sell any stock, and a set of indicators that can tell him when the market is headed for a rally or a plunge.

Despite widespread investor pessimism, Keith’s data suggests it could be a great time to grab stocks poised for profits. Here he is describing what he sees.

They say you should never try to catch a falling knife.

That’s certainly true… if you’re doing it without a plan.

But if you do it with the right stocks, buying into a downtrend and banking on a reversal can be quite lucrative.

A couple months back, we got the idea of designing a system that’s like catching a falling knife with Kevlar gloves on… where we minimize the risk and trade only the rarest setups with a strong track record of working.

We tested tons of different variables, and eventually we found one combination that produces a rare but quite reliable trading signal.

Keith and his team designed a system that helps investors take advantage of rare but reliable setups with a strong track record of success.

Here is one example from Keith’s back-testing.

One of the cleanest examples I’ve found – a case from 2022, in Caesars Entertainment (CZR).

The signal triggered at $32.36 on Sept. 30… and would’ve led to a 35.5% gain if you’d sold it 21 trading days later (on Oct. 31) for $43.73:

To be clear, there are losers too. No system is 100%.

But in Keith’s study, only one-fifth of the signals lost money, which makes for pretty good odds.

Our data shows that we’re in a rare kind of market that we previously only saw in 1996… and then 70 years earlier, in 1926.

If your market history is sharp, you know those were the early stages of massive investment manias that went far further and lasted much longer than anyone expected.

Both were powered by technological breakthroughs… financial institutions lowering the barrier for smaller investors to participate… and a consumer credit revolution that spurred the economy higher.

These are all things we’re seeing the beginnings of today. And what we’ve found is that these specific conditions signal the start of a “mega melt-up.”

Keith prepared a free demo where he shows how to find 10 “melt-up stocks” for the historic market conditions TradeSmith is picking up now.

We all work hard for the money we invest, so it’s difficult to watch the market plunge. But staying with the data and not acting emotionally is going to lead to greater profits over time.

California’s recent traumatic spate of wildfires has spotlighted the often clunky process of traditional commercial insurance.

Typically, businesses are required to document their losses, file a claim, and wait months or even years for reimbursement. Insurance companies must meticulously assess damages, verify that a claim was not excluded from the policy, and determine how much to pay. Midsize companies and multifamily property owners can go bankrupt waiting for reimbursement.

Some businesses are choosing another option that promises to get them help faster: parametric policies. Allied Market Research forecasts that the global parametric insurance market, which totaled $18 billion in 2023, will grow to more than $34 billion by 2033.

Parametric insurance has been around for years, covering catastrophes like tropical cyclones, other weather-related events, and earthquakes. These policies’ main advantage is a faster payout, since the insurer agrees to pay a predefined sum when a specific peril reaches a predefined magnitude. Payment is triggered by parameters that can be measured quickly, such as rainfall, hurricane category, or wind speed.

The insurer knows how much the insurance subscriber will pay, and the subscriber understands the amount of coverage it will get. Both are aware of the conditions necessary to green-light the payment.

Parametric policies are expensive: A $1 million wildfire insurance policy could require $50,000 in annual premium payments. But the increased frequency of natural disasters is emphasizing the need for faster procedures. Ten years ago, wildfires were considered secondary perils and not regarded as existential threats. The 2016 Fort McMurray fire in Alberta, Canada, changed that attitude within the insurance industry: The fire caused $3 billion in losses, which at that time was considered enormous.

Since then, wildfire costs in the US have multiplied, totaling $67 billion in insured losses in 2024, not counting the 2025 fires, according to reinsurer Munich Re.

Target is scheduled to post its fourth-quarter earnings report on Tuesday, with analysts seeing substantial upside for the retailer’s stock.

Sales and profit for Target are expected by analysts to decline from the same time a year ago, while comparable store sales are projected to rise.

Analysts have said lately that they expect Target will be conservative in its 2025 forecasts, and they are looking for updates on executive succession planning.

Target (TGT) is set to report fourth-quarter earnings on Tuesday morning, with analysts seeing substantial upside for the retailer’s stock.

Analysts’ ratings are split nearly evenly, with five “buy” and six “hold” ratings among the brokers who currently follow Target and are tracked by Visible Alpha. Their average price target of just under $145 suggests about 18% upside to Friday’s close and would put the stock back at late-January levels.

The retailer is expected to report revenue of $30.77 billion for the quarter and adjusted earnings per share of $2.26, down 3.6% and 24%, respectively, from the same time a year ago. At the same time, analysts expect comparable store sales to rise 1.39% year-over-year, a consensus figure that Morgan Stanley analysts noted this week has risen since Target lifted its comparable sales projection in January.

Analysts Expect Conservative 2025 Outlook, Question CEO Succession

Analysts from JPMorgan, Oppenheimer, and Morgan Stanley all said in recent notes that they expect Target will likely follow some of its retail rivals like Walmart (WMT) and Home Depot (HD) and remain conservative in their first-quarter and 2025 projections.

Despite a potential conservative 2025 forecast—and concerns over the impact of tariffs and inflation on discretionary spending—Oppenheimer analysts said they “continue to believe shares have bottomed” and said they would “take advantage of any volatility” after the report. They noted that Target shares have fallen after two of the past four earnings reports, with double-digit swings after four of the last five.

JPMorgan and Morgan Stanley analysts also raised the question of succession planning entering 2025, as CEO Brian Cornell recently passed 10 years in the top job. JPMorgan analysts said Cornell planned to stay for three more years as of September 2022, and said they believe an internal candidate to replace him is “most likely.”

Target shares are down about 18% over the last 12 months. They rose Friday, finishing the week a bit above $124 apiece.

Editor’s Note: This week has been volatile to say the least…

But if anything, that has me and my friends at TradeSmith even more fired up about the market ahead.

The fact is, we’re in a Mega Melt-Up. All the signs are there.

And if you make the right moves today, you’ll be set for a bull market that rivals the internet boom… while avoiding the inevitable bust.

TradeSmith CEO Keith Kaplan has some thoughts below on this week’s volatility… including how it’s convincing us even more that the Mega Melt-Up is on.

Read it below. And be sure to watch his biggest forecast in 20 years, in this brand-new special research presentation. He’ll also share 20 recommendations just for checking it out.

**************************

The market has taken us on a wild ride in 2025.

Between Chinese AI breakthroughs, radical shifts in trade policy, the Federal Reserve’s rate-cutting cycle, and now a surge in inflation expectations, the headlines have been all over the place.

Stocks are acting as you’d expect – soaring one week, shaking out weak hands the next.

All this wild price action has ultimately not taken us far. As I write, the Nasdaq 100 is basically flat from the start of the year…

And that’s especially painful, considering the 5.7% year-to-date gain we were looking at just a week ago.

All this chaos can’t help but make you wonder, “Are we heading for a crash?”

If you google that question, you’ll probably find a bunch of mainstream media headlines urging you to stay scared.

But I’m here to tell you something quite different:

This isn’t the beginning of a bear market.

On the contrary, it’s the setup for one of the biggest opportunities of your lifetime.

We’re smack in the middle of what my team has taken to calling a Mega Melt-Up.

We’ve gone through history and quantified the price action of the past few years. And what we found, shocking as it was, tells us that there’s only been two previous market environments like this one: the 1990s and the 1920s. And both were periods where individual companies rose thousands of percent in very short order.

If our research is correct, and I’m confident it is, the volatility we’ve seen this year isn’t a warning sign.

Instead, it’s even more evidence that we’re in a Mega Melt-Up… the kind that only comes around once or twice in a lifetime.

Three Bear Markets to a 1,000% Gain

Yes, the volatility we’re seeing right now actually supports the case for a Mega Melt-Up.

Let’s take a quick trip back in time.

Like what we’ve seen so far in the 2020s, the 1990s were a boom decade.

From 1995 to 2000, the Nasdaq 100 went up 1,000%.

But it wasn’t a straight shot up. In fact, there were more than two dozen major pullbacks in those five years…

Several of which you could consider an “official” bear market…

And each of which would prove a buying opportunity.

Let’s look at 1995-1996.

Starting in 1995, the Nasdaq 100 started to become a lot more volatile. From July 1995 to August 1996, the Nasdaq 100 posted drawdowns of 9.1%… 10.5%… 14%… 8.2%… and 14.4%. All in the span of one year:

What else happened back then? Well, in 1995 the Nasdaq 100 rose almost 40%. And the next year, it rose 22.7%.

Let’s skip ahead a bit to 1997-1998. We see the exact same thing.

Not only did the Nasdaq 100 retreat 20% in late 1997, creating a short-lived bear market… it saw two separate drawdowns of -22.2% and -19.1% within six months in 1998:

Yet once again, the index went up 21.6% in 1997 and 39.6% in 1998.

Finally, let’s look at 1999. Four major pullbacks in the double-digit range, and one final flush of nearly 9% before stocks took off into the end of the year:

What was the Nasdaq 100’s return in 1999? 101.95%… the highest ever.

The big takeaway from this is simple. You can’t have a Mega Melt-Up without massive price swings along the way.

This is exactly what we found in our research. Both the ‘90s Mega Melt-Up and the 1920s Mega Melt-Up were marked by a ton of volatility.

It’s the price you pay for the kind of extraordinary gains markets deliver in these times.

And, when you zoom out, it’s clear that it’s a small price to pay.

Now, by comparison, what we’re seeing in stocks right now isn’t anything like what I just showed you. The S&P 500 is 3% off its highs and the Nasdaq 100 is nearly 7% off its highs.

They can absolutely go lower from here, and that would not change my thinking onthis Mega Melt-Up one bit.

In fact, there’s an argument that the Melt-Up we’re about to see could be even bigger than the one in the ‘90s.

Why This Melt-Up Could Be Bigger Than the 1990s

The 1990s had three powerful forces fueling stocks:

The birth of the internet (what we’ve been calling a General Purpose Technology) and the associated new companies taking advantage of the trend.

The rise of online trading, making stocks more accessible than ever.

Easier monetary policy, where the Fed’s interest-rate cuts fueled a consumer credit boom.

These three forces are what we call Melt-Up Multipliers. For a Melt-Up to be truly powerful, it must have these specific three factors.

The 1920s saw the same thing, with electrification being the major technological breakthrough… margin lending making it possible for investors to own more stocks than they could buy… and a consumer credit boom powering the economy.

Today, we have these same three melt-up multipliers… and one more.

Artificial Intelligence: AI is today’s Internet moment – a technology that’s changing everything, from medicine to finance.

Zero-Commission Trading & Apps Like Robinhood: More retail money is flooding into the markets than ever before.

The Fed’s Rate Cuts: The Federal Reserve is slashing rates again, just like it did in the mid-90s.

Oh, and there’s a “wild card” fourth factor… President Donald Trump. Like him or not, his policies are market-friendly… And the last time he took office in 2017, the Nasdaq 100 surged 31.5%.

This is the perfect storm for a Mega Melt-Up.

But there’s a tricky thing to understand about melt-ups… and especially Mega Melt-Ups…

All melt-ups end the same way – in a meltdown.

Ride the Melt-Up and Avoid the Meltdown

The 1990s Melt-Up ended with the 2000 crash. The Roaring ’20s Melt-Up ended in the 1929 crash… and, even worse, the Great Depression.

And yes, this melt-up will end in a crash, too.

But that doesn’t mean you should sit on the sidelines. It means you need the right tools to capture the upside – and know exactly when to get out.

That’s why we built Trade360, our all-in-one software suite that’s designed to help you make the most out of every market environment.

And we recently made two big upgrades specifically to make it the perfect trading tool for a Mega Melt-Up period like we’re seeing now.

One is a tool that clearly identifies whether markets are in Melt-Up mode or not… and alerts you when that condition changes.

With this, you don’t have to second-guess whether or not we’ve seen a major top. You’ll get an alert that tells you when it’s time to get out before stocks crash.

The other is an advanced trading strategy that’s perfectly suited to melt-up environments.

Remember all those drawdowns in the Nasdaq 100 I showed you earlier?

If we’re seeing all that selling in the benchmark, you better believe we’re seeing it in individual stocks, too.

So, we designed a strategy that takes advantage of these short-term, extreme pullbacks in otherwise quality stocks.

When prices fall by a certain amount and at a certain pace, the strategy buys in… and sells the stock 21 trading days later.

This simple strategy has a near 80% win rate and average gains of around 16% – counting winners and losers.

And it works whether stocks are in a bull market, or a bear market… as it targets those rare occurrences where prices reach irrational extremes.

More than a year after the first rate cuts by the European Central Bank (ECB) and the US Fed since the pandemic, Australia has finally joined the global rate cycle by trimming borrowing costs in the country by a quarter point in late February.

The Pacific country is one of the last developed economies in the world to pivot on its interest rate stance. The lone exception remains Japan, which is, in fact, raising capital costs after decades of negative rates and inflation.

The quarter-point cut will bring Australia’s cash rate target to 4.10% and the interest rate paid on exchange settlement balances to 4%, a tab lower than the Fed’s current 4.25% rate.

In her policy decision statement, Reserve Bank of Australia (RBA) governor Michele Bullock attributed the cuts to subsiding inflation, which has hit 3.2% in the latest report. She also mentioned continued “subdued growth in private demand,” as another key driver of the rate cut.

The latest quarter-on-quarter GDP report for the country came in at 0.3%, well below general expectations of a 0.5% increase. Year-on-year economic growth figures also disappointed, showing a 0.8% increase against a 1.1% expectation.

Despite the milestone move by the RBA, the market interpreted the news as a “hawkish” cut, as Bullock was quick to dampen expectations for deeper rate cuts in the next few meetings.

“The market is expecting quite a few more interest rate cuts in the middle of next year, about three more on top of this,” said Bullock in the news conference that followed the RBA statement. “Whether or not that eventuates is going to depend very much on the data. Our feeling at the moment is that that is far too confident.”

As a consequence, the market adapted its expectations for rate cuts in the country, pushing the Australian dollar upward against the US dollar, an unusual follow-up to a rate cut. “Interest rate swaps markets now price in fewer than two further rate cuts from the RBA this year, with the second of the cycle not fully priced until August,” explained David Scutt, an analyst at Forex.com.

Consumer confidence has fallen as Americans worry that companies will pass on the cost of tariffs, increasing their costs and inflation.

Many companies that serve companies say they would raise at least some prices, including: Steve Madden, Sally Beauty and home appliance company Hamilton Beach.

Some companies say they’re confident they can navigate a market reshaped by tariffs.

American consumers are anxious about tariffs. The companies that serve them are, too, though not all of them are bracing for the worst.

Consumer sentiment in February took the biggest monthly hit seen in three years, according to The Conference Board’s Consumer Confidence survey, which showed that Americans are concerned tariffs will spur inflation.

Businesses are exploring how to protect their profits through supply chain changes and price increases, executives said during recent conference calls. While some consumer-focused companies worry tariffs will hurt business, others are confident they can handle—or even reap rewards from—higher import costs.

President Donald Trump said this week that he plans to impose a 25% tariff on products from Mexico and Canada, beginning Tuesday. He also said the U.S. would raise a tariff on goods from China to 20% and has recently talked about adding tariffs to items from other regions, including the European Union.

Tariffs Would Lead to Price Hikes at Some Companies

Many companies said they’d raise at least some prices if tariffs were enacted—from the cosmetic company Sally Beauty (SBH) to Hamilton Beach Brands (HBB), which sells small household appliances.

A number of businesses said they worked to blunt the potential blow by diversifying their supply chains. Steve Madden (SHOO) diminished sourcing from China by about 20% since the last quarter, CEO Edward Rosenfeld said. But selective price increases will still be necessary, he said.

Higher prices may not dramatically alter the outlook for some companies. Birkenstock (BIRK), which finishes its shoe assembly in Germany, has been able to raise prices without consequence in the past, CFO Ivica Krolo said on an earnings conference call last month.

“The good news here [is] that we have, historically, [had] the ability to take pricing action globally that offsets these inflationary pressures, including tariffs, without any impact on our business,” Krolo said, according to a transcript made available by AlphaSense.

‘We’ve Been Through This Before’

Some large companies see their size as an advantage in navigating tariffs. Coca-Cola (KO) could rely more on plastic bottles than cans, CEO James Quincey said on an earnings conference call in February. He added that even if the company pays more for aluminum, it’s “not going to radically change a multibillion dollar U.S. business.”

Walmart (WMT) knows how to find value for consumers amid tariffs, executives said. So does Home Depot (HD), executive vice president of merchandising Billy Bastek said on an earnings call this week.

“We’ve been through this before,” Bastek said, according to a transcript made available by AlphaSense. “With our scale, we feel that we’re as well or better positioned than anyone in the marketplace.”

Some Companies See Chance to Benefit

A few companies said they may even benefit from tariffs.

Roku (ROKU) doesn’t expect tariffs to impact its product margins. But they could raise the cost of “higher end” TVs, prompting people to move to less expensive options and driving up demand for Roku, said Mustafa Ozgen, president of devices, products and technology.

Newell Brands (NWL), which sells Yankee candles, believes tariffs present both headwinds and potential benefits. The company has ramped up its production capacity in the U.S., CEO Christopher Peterson said. This gives Newell an advantage over competitors—and potential clients—he said on an earnings call in February.

The company has been informing retailers it can quickly add manufacturing capacity in the U.S. “on a first come, first serve basis,” Peterson said.