The states with the highest 30-year new purchase mortgage rates Thursday were Alaska, West Virginia, Maryland, South Dakota, Maine, Mississippi, North Dakota, and Wyoming. The range of rate averages for these eight priciest states was 7.00% to 7.08%.

Every other state, plus Washington, D.C., had a Thursday 30-year rate average below 7%. The cheapest of these were New York, Pennsylvania, Florida, Georgia, Texas, North Carolina, New Hampshire, and Oregon. The eight lowest-rate states registered averages between 6.73% and 6.92%.

Mortgage rates vary by the state where they originate. Different lenders operate in different regions, and rates can be influenced by state-level variations in credit score, average loan size, and regulations. Lenders also have varying risk management strategies that influence the rates they offer.

Since rates vary widely across lenders, it’s always smart to shop around for your best mortgage option and compare rates regularly, no matter the type of home loan you seek.

Important

The rates we publish won’t compare directly with teaser rates you see advertised online since those rates are cherry-picked as the most attractive vs. the averages you see here. Teaser rates may involve paying points in advance or may be based on a hypothetical borrower with an ultra-high credit score or for a smaller-than-typical loan. The rate you ultimately secure will be based on factors like your credit score, income, and more, so it can vary from the averages you see here.

National Mortgage Rate Averages

Following a two-day drop, 30-year new purchase mortgages inched up a minor 4 basis points Thursday, to a national average of 6.95%. That’s still better than mid-April, when rates surged 44 basis points in a week to average 7.14%—the most expensive level since May 2024.

In March, however, 30-year rates sank to 6.50%, their cheapest average of 2025. And in September, 30-year rates plunged to a two-year low of 5.89%.

Calculate monthly payments for different loan scenarios with our Mortgage Calculator.

What Causes Mortgage Rates to Rise or Fall?

Mortgage rates are determined by a complex interaction of macroeconomic and industry factors, such as:

The level and direction of the bond market, especially 10-year Treasury yields

The Federal Reserve’s current monetary policy, especially as it relates to bond buying and funding government-backed mortgages

Competition between mortgage lenders and across loan types

Because any number of these can cause fluctuations simultaneously, it’s generally difficult to attribute any change to any one factor.

Macroeconomic factors kept the mortgage market relatively low for much of 2021. In particular, the Federal Reserve had been buying billions of dollars of bonds in response to the pandemic’s economic pressures. This bond-buying policy is a major influencer of mortgage rates.

But starting in November 2021, the Fed began tapering its bond purchases downward, making sizable monthly reductions until reaching net zero in March 2022.

Between that time and July 2023, the Fed aggressively raised the federal funds rate to fight decades-high inflation. While the fed funds rate can influence mortgage rates, it doesn’t directly do so. In fact, the fed funds rate and mortgage rates can move in opposite directions.

But given the historic speed and magnitude of the Fed’s 2022 and 2023 rate increases—raising the benchmark rate 5.25 percentage points over 16 months—even the indirect influence of the fed funds rate has resulted in a dramatic upward impact on mortgage rates over the last two years.

The Fed maintained the federal funds rate at its peak level for almost 14 months, beginning in July 2023. But in September, the central bank announced a first rate cut of 0.50 percentage points, and then followed that with quarter-point reductions in November and December.

For its third meeting of the new year, however, the Fed opted to hold rates steady—and it’s possible the central bank may not make another rate cut for months. With a total of eight rate-setting meetings scheduled per year, that means we could see multiple rate-hold announcements in 2025.

Building on a profitable and dynamic 2023, when high interest rates buoyed bank lending margins, most Western European banks had a strong 2024, ending the year with a spurt in net income and revenue growth. Many increased their focus on sustainable finance (with green bonds as a major growth area), diversified their revenue streams, and invested in new banking technology—modernizing existing apps and exploring new possibilities.

Healthy profitability was particularly notable among larger banks with an extensive branch network and strong franchises, and among banks in Southern and Southeastern Europe with large shares of the local market. In addition, banks benefited from strong investor sentiment. According to global consultancy EY, between the fourth quarter of 2023 and the fourth quarter of 2024, European bank shares rose 18%, “outperforming US banks and broader European indices by 10 percentage points.”

EY pointed out that the strong underlying position of most European banks earlier in the year enabled them to face a changing outlook toward year-end. There was a strong uptick in geopolitical uncertainty and market volatility, helping to bolster trading revenues, which were up across the board in Western Europe. Interest rates fell in some cases, and interest rates will continue to fall into 2025.

Wealth management and investment banking were growth areas, according to Nigel Moden, banking and capital markets lead at EY. “Investment banking revenues at [European banks] reached their highest levels since 2009, driven by broad-based strength across fee-generating activities and trading operations. M&A and IPO fees increased by 32% compared to 2023, although they remain below their 10-year averages,” he posted on EY’s website.

At the end of 2024, the European Central Bank (ECB) published its annual Supervisory Review and Evaluation Process, with the authors concluding that the banks of the euro area—into which most of this year’s winners fall—remained resilient in 2024. “On average, banks maintained solid capital and liquidity positions, well above regulatory requirements,” they conclude. “The aggregate Common Equity Tier 1 (CET1) ratio stood at 15.8% in mid-2024, which is a slight improvement compared with the previous year. The leverage ratio increased slightly to 5.8%. Higher interest rates continued to sustain banks’ profitability.”

In a few notes of warning, they add that “concerns around banks’ governance, risk management—including climate and nature-related risks—and operational resilience persist and require swift remediation due to the uncertain risk environment.”

Regional Winner

Gonzalo Gortazar, CEO, CaixaBank

Best Bank in Western Europe | CAIXABANK

CaixaBank has repeated its win of the Best Bank in Western Europe award and Best Bank in its home country, Spain. The country’s third-largest bank, with assets of €631 billion (about $657 billion), has a broad international representation; but its focus continues to be domestic. The bank holds impressive positions in key consumer segments, including 23.4% of consumer lending, almost 25% of consumer deposits, 23.7% of investment funds, and 34.3% of pension plans. Given Spain’s strong economic performance, this domestic emphasis has helped play into profits—last year, these were nearly €5.8 billion, up 20.2% on 2023’s more than €4.8 billion—while gross income was almost €15.9 billion, up 11.5% from 2023. Net interest income in 2024 was up almost 10% at €11.1 billion, and return on equity (ROE) reached 15.4% from 13.2% in 2023. In December, Fitch Ratings upgraded the bank to A-, citing Spain’s improved operating environment and the bank’s improved profitability and asset quality.

CaixaBank has finished its integration of the Spanish stateowned Bankia, with which it merged in 2021. Related synergies have helped CaixaBank reduce costs relative to income: In 2024, the bank’s cost-income ratio stood at 38.5% against 2023’s 40.9%. Asset quality improved, with the nonperforming loan ratio in 2024 standing at 2.6%, below the target of 3% and down from 2023’s 2.7%.

Spain enjoyed some of the fastest economic growth in the eurozone in 2024, a standout year for the bank’s wealth management business. Revenues totaled €1.8 billion, up 12.1%, and wealth management balances rose strongly by 11.7% to €263.3 billion. Net inflows to mutual funds, savings insurance, and pension plans continued to grow strongly. As a result, CaixaBank extended its market-share leadership in wealth management, claiming 29.5% of the market and widening the gap with its competitors.

Between 2021 and the end of 2024, CaixaBank mobilized nearly €86.8 billion in sustainable finance, far exceeding its original target of €64 billion. The bank continues to press forward with ambitious sustainable banking targets, mobilizing nearly €36 billion in 2024 alone.

Rating agencies have recognized the strength and versatility of CaixaBank’s business model. Toward the end of 2024, Fitch and S&P each upgraded the bank’s credit ratings, citing the bank’s sound funding and liquidity. Fitch highlights CaixaBank’s “diversified business model [which] underpins its resilience through economic cycles” and its “risk control framework and limits [which] are comprehensive, sound and commensurate with its business model.” Fitch also praises the bank’s “sound and resilient profitability,” noting that it will further benefit from “higher business volumes and strong income generation from wealth management and insurance.”

Country, Territory and District Winners

Andorra | CREAND CREDIT ANDORRA

Returning for the fifth time in a row as the Best Bank in Andorra, Credit Andorra has fully integrated Vall Banc, the acquisition of which was completed three years ago. The bank is now widely known as Creand Credit Andorra. With over €51.7 billion under management, profit increased by over 60% to nearly €71.3 million in 2024.

Austria | UNICREDIT BANK AUSTRIA

Net profits for this year’s Austrian winner, UniCredit Bank Austria, were up 14.2% over 2024, reaching approximately €1.3 billion. This seals a very satisfactory year for the institution, whose total assets now stand at around €105.3 billion. In the year in which Bank Austria celebrated 20 years as part of the UniCredit group, the bank consolidated its leading position in corporate banking, wealth management, and private banking. With an extensive network of over 104 branches across Austria, it has become the national leader in mobile banking, with usage now at 63%, well above the market average of 55%. Already, 21% of Bank Austria customers see themselves as digital-only users, compared to the market average of 15%.

Belgium | BNP PARIBAS FORTIS

BNP Paribas Fortis has earned its award as the Best Bank in Belgium after an impressive and rewarding year. This continued into early 2025 when the bank released the latest version its Easy Banking App. It enables users to look at their financial activities in real time and load their activities with other banking groups (like ING, Belfius, or KBC) through the app. The bank worked with Swedish fintech company Tink to develop the app.

Cyprus | BANK OF CYPRUS

With assets of just under €26 billion, the Bank of Cyprus—the primary beneficiary of Cyprus’ 2012-14 financial crisis—had another great year, with preliminary results for 2024 suggesting a 4% increase in after-tax profits to a record €508 million. The Bank of Cyprus is a key financial actor on the island: The bank now has 38% of deposits and 43% of loans, while its digital sales platform Genius enables seamless connection of its customers and businesses with suppliers and other companies. In a strategic repositioning, the Bank of Cyprus—whose market capitalization is now €2.3 billion—has moved its listing from the London to the Athens Stock Exchange.

Denmark | DANSKE BANK

Danske Bank—our winner in Denmark—consolidated its lead over domestic rivals, reporting total assets of over 3.7 trillion Danish kroner (about $518 billion) by the end of 2024 with solid results, building on 2023’s recovery. For 2024, the bank reported net profits of 23.6 billion kroner, up 11.1%; and total income of 56.4 billion kroner, up 7.8%. ROE in 2024 was 13.4% against 2023’s 12.7%.

Finland | NORDEA

The Best Bank in Finland, Nordea, which has benefitted from the country’s membership in the European Single Market, further consolidated its dominance of the sector with total assets worth €623.4 billion, up €39 billion in 2023, and a nearly 62.7% market share (based on total assets). The bank’s 2024 operating profit was over €6.5 billion, up 2.5% year on year.

France | BNP PARIBAS

BNP Paribas won this year’s award as Best Bank in France, despite sluggish growth in its commercial and retail operations in 2024, reflecting the broader economic picture in France. However, the division rebounded in the final quarter, recording growth of 4.7%. A revival in investment banking helped the bank to lift its profits by more than 15% in the fourth quarter. The bank, France’s largest lender, said it would launch a new strategic plan to boost the profitability of its domestic business, increasing the profitability of commercial and personal banking in France to the level of the wider group. Growth at BNP is expected to be boosted by the integration of Axa Investment Managers, acquired from French insurer Axa last year in a €5.1 billion deal.

Germany | COMMERZBANK

For our German winner, Commerzbank, Germany’s thirdlargest bank, last year was big, with assets of €555 billion in 2024. Its net profits hit a record €2.7 billion, a rise of 20% over 2023 and an increase of more than 50% from 2022. The bank aims to increase its net result to €4.2 billion by 2028. With its upgraded “Momentum” strategy, Commerzbank has set significantly more-ambitious targets than before, focusing strongly on small businesses and on private customers and wealth management. The return on tangible equity (ROTE) is expected to improve to 15% by 2028. This means that the bank will earn significantly more than its cost of capital and be a well-established player among the successful European banks.

The bank entered 2025 fighting a hostile bid from our Italian winner, UniCredit. The latter received ECB approval in March to up its stake in the German bank to 29.9%. However, UniCredit has indicated it will probably wait until 2026 before announcing its future strategy.

Greece | EUROBANK

The winner as Best Bank in Greece, Eurobank, has earned the title after an impressive 2024. With a vast international presence in Bulgaria, the UK, Luxemburg, and Cyprus, Eurobank Holdings had assets of nearly €100 billion, as of September 2024. The bank reported net earnings of €1.45 billion in 2024, up 27% on 2023. In early 2025 it completed the purchase of an additional 37.5% of Hellenic Bank in Cyprus, bringing its total holding close to 100%. The entity is to be merged with Eurobank Cyprus to compete against Bank of Cyprus, the other main bank on the island.

Eurobank argues that its business success reflects its wide range of activities, including “egg” (enter, grow, go), a business startup plan aimed at small and midsize enterprises and now the second-largest such scheme in Eastern Europe. Another bank initiative is Trade Corridors, a “phygital” business network aimed at helping Greek businesses locate and do business with potential global partners.

Iceland| LANDSBANKINN

Iceland’s largest bank, Landsbankinn returns as the Best Bank in Iceland for a second consecutive year. Holding some 40% of the domestic retail market, profit in 2024 was 37.5 billion Icelandic krónur (about $271 million) after taxes, up from 33.2 billion krónur in 2023. ROE in 2024 was 12.1%, lending was up 10.8%, and customer deposits increased by 17.2%. The Smart Savings app saw customer usage rise by almost 40% last year.

Ireland | AIB

Allied Irish Bank (AIB) has earned the title of Best Bank in Ireland for the second year in a row. It delivered a strong 2024 performance with a profit after tax of €2.35 billion, a 26.7% ROTE, and total 2024 distributions to shareholders of €2.6 billion. Buoyed by a vibrant economy, new lending grew by 17% to €14.5 billion, while the customer base reached its highest level at 3.35 million.

Italy | UNICREDIT

Our winner in Italy, UniCredit had another impressive year, with full-year net profit up 2% to reach €9.7 billion. Net revenue grew 4% to €24.2 billion, up 4% fiscal year over fiscal year, driven by fees at €8.1 billion, up 8% on the year, reflecting strong client activity and broad product offering to the bank’s more than 15 million customers across Europe. The bank is firmly committed to sustainability and other environmental, social, and governance principles. UniCredit seeks to boost digitalization across the group. Fitch upgraded the bank to BBB+ in October 2024.

The record-breaking performance marked the 16th consecutive quarter of sustainable, profitable growth. This reflects the potential unlocked during the initial phase of the UniCredit Unlocked transformation plan. UniCredit became a unique pan-European model increasingly active in Central and Eastern Europe and in Germany. Diversified fees and high-quality net revenue growth, high organic capital generation, strong ROTE, and generous total distributions have all set the path for UniCredit to enter its next acceleration phase from 2025 to 2027. As 2025 got underway, UniCredit Italy is reported to have bought a stake in insurance giant Generali Group and to be separately trying to take over Milan lender Banco BPM, in which both groups also own a stake.

Liechtenstein | LGT

Liechtenstein’s LGT, the principality’s largest bank, owned wholly by the royal family, has had a good few years. It started 2024 with more than 58.1 billion Swiss francs (over $64 billion) in assets. To boost its asset management business in Austria, LGT is looking for acquisition opportunities in Switzerland and Germany.

Luxembourg | SPUERKEESS (BCEE)

Spuerkeess (BCEE) returns as the Best Bank in Luxembourg for the fourth consecutive year. Better known as Banque et Caisse d’Epargne de l’Etat, state owned and established in 1856, BCEE has dominated banking in the duchy for decades and currently controls around 50% of the retail banking and mortgage market. BCEE successfully issued a €500 million 6NC5 senior preferred green bond on March 12, marking a significant milestone in its capital markets strategy. The bond, which was oversubscribed 3.6 times and issued under BCEE’s newly launched Green Bond Framework, will be listed on the Luxembourg Stock Exchange.

Malta | HSBC

HSBC takes home the award for the Best Bank in Malta after a record 2023 in which pretax profits rose 141% to €133.9 million on the back of increased net interest margins and higher earnings from its insurance subsidiary. Last year, the bank posted another pretax profit increase, of 15% to €154.5 million, and ROE was slightly up at 17.5% against 17.1% in 2023. Customer deposits increased by €16.8 million to almost €6.2 billion as of December 31, 2024. Management attributes the increase in profits to growth across all revenue lines, mainly due to higher interest rates, increased customer activity, and higher insurance subsidiary results. HSBC Malta’s strong performance hasn’t gone unnoticed; takeover talks were in the air. However, government officials were said to be opposed, arguing that Malta needs more rather than less competition among its banks.

Monaco | CFM INDOSUEZ WEALTH MANAGEMENT

Monaco’s CFM Indosuez Wealth Management, owned mainly by Credit Agricole, has won the laurels as the Best Bank in Monaco. The principality’s leading commercial bank, serving two out of three businesses—unsurprisingly, given its history and location—puts wealth management center stage. However, it also launched its StartUp Connections last year, a digital platform offering simplified access to an international network of startups in Monaco, Belgium, Luxembourg, and Switzerland.

Netherlands | ING

Our Dutch winner, ING, with over 60,000 employees serving 40 million customers globally, is familiar to anyone who does business with or visits the Netherlands. Over 2024, the bank consolidated its position as market leader. Global assets reached approximately €1 trillion, but annual net profits for the year came in below market expectations at €6.4 billion. Income is expected to hold steady this year on the back of falling interest rates, according to CEO Steven van Rijswijk, who says the bank is looking for acquisitions this year to help boost overall performance.

Throughout 2024, the bank said it would increase focus on wholesale, personal, and private banking. In March 2025, ING announced that it had reached an agreement with Reggeborgh Groep on the acquisition of a 17.6% stake in Van Lanschot Kempen, a specialist wealth manager serving private, institutional, and investment banking clients, operating predominantly in the Netherlands and Belgium. With an existing 2.7% stake, ING will hold a 20.3% stake in Van Lanschot Kempen after the completion of the transaction.

ING has also reiterated its commitment to its climate goals, advising clients that it will either restrict or stop providing finance, on a case-by-case basis, to companies that fail to address their carbon footprint. This stands in sharp contrast to many other financial institutions that have loosened some climate targets.

Norway | DNB

Last year was a good year to be a banker in the Nordic region, with improvements in asset quality and overall performance driven by a broadly benign economic environment and market dominance for the key players. The Norwegian winner, DNB, had another solid year as the leading bank in Norway with a year-end market capitalization of 336 billion Norwegian kroner (about $29.7 billion), up from 328 billion kroner in 2023; and post-tax profits of 45.8 million kroner, up on 2023’s approximately 39.5 million kroner, a result reflecting Norway’s GDP growth of 2.1% last year against just 0.1% in 2023.

Portugal | BANCO SANTANDER TOTTA

The winner for Portugal, Banco Santander Totta, is the third-largest bank in the country by assets (€56 billion), with some 4.7 million customers. Its net profits for last year were up again, by 10.7% over 2023, to reach €990 million, an impressive reflection on the bank’s performance and Portugal’s ongoing economic recovery. The bank actively courts the youth market, offering work cafes, and is well ahead of competitors in its digital offerings. However, it has not forgotten seniors, launching a new health insurance product for them. Fitch gives Banco Santander Totta the Portuguese bank sector’s highest score, A.

Sweden | SWEDBANK

Swedbank, the country’s third-largest domestic bank, is the winner in Sweden on the back of solid results: After-tax profits for 2024 were up 2.2% to 34.1 billion kronor (about $3.1 billion), while total assets reached 3 trillion kronor, with 7.4 million private customers.

Switzerland | UBS

UBS returns for the fifth year in a row as the Best Bank in Switzerland and reflects another strong year—the complex takeover of Credit Suisse is now almost complete—in which it increased its local market share by 40% and became the world’s largest wealth management bank. The bank’s 2024 net profits were $5.1 billion, lower than the previous year but better than expected—an otherwise normal year but impacted by the ongoing Credit Suisse integration. UBS plans to buy back $1 billion of shares in the first half of 2025 and up to $2 billion in the second if there are no “material and immediate changes” to Swiss capital rules that the authorities are considering to require UBS to hold more capital.

UK | HSBC

On the back of impressive group results, HSBC wins the Best Bank in the UK award. The Group, which reports in dollars, posted a post-tax profit increase of $400 million over the previous year to $25 billion, and total group assets topped $3 trillion by the end of 2024. Last year saw several initiatives in the UK market. These included the launch of Flexipay, which lets consumers spread the cost of a large point-of-sale purchase at one of the bank’s merchant partners, whether or not the customer has an existing HSBC relationship; the relaunch of the bank’s fee-free Premier Account; and the debut of new benefits for its Premier World Elite credit card. HSBC UK also revealed its plans to double assets under management to £100 billion ($134 billion) by 2028.

So, it was another strong year for Western Europe’s leading banks. Most have positioned themselves well for 2025; although with rising geopolitical uncertainty, a possible tariff war and other negatives, 2025 looks to be very different from 2024. In its look ahead to 2025, Fitch in December noted that 80% of the region’s banks have a stable outlook, with just 4% on a negative outlook and 15% on a positive one. The rating agency also suggested that “business conditions for the banks will remain sound, resulting in another year of good performance” and maybe an increased prospect of consolidation.

The improving outlook is particularly pronounced in the southern countries, Greece, Portugal, and Spain, on the back of continued business growth. The Nordic region and the Benelux countries are facing a neutral outlook with continued strong profitability and resilient asset quality. Banks in Germany and Italy have a neutral outlook with “resilience amidst weak economic performance” (Germany) or “subdued credit demand” (Italy). By contrast, French banks face a deteriorating outlook amid “macro uncertainties and political risk.”

With the overall macro-outlook in early 2025 more uncertain than it has been in many years, it was perhaps unsurprising that the ECB announced in January that it would stress test some 96 eurozone banks over the year. The ECB’s priorities for the sector in 2025 include, among other things, strengthening bank resilience to macro-financial and geopolitical shocks, and ensuring banks address digital transformation and climate change in an efficient and meaningful way. In a fast-changing world, the healthiest West European banks—like banks everywhere else—will demonstrate genuine foresight and flexibility.

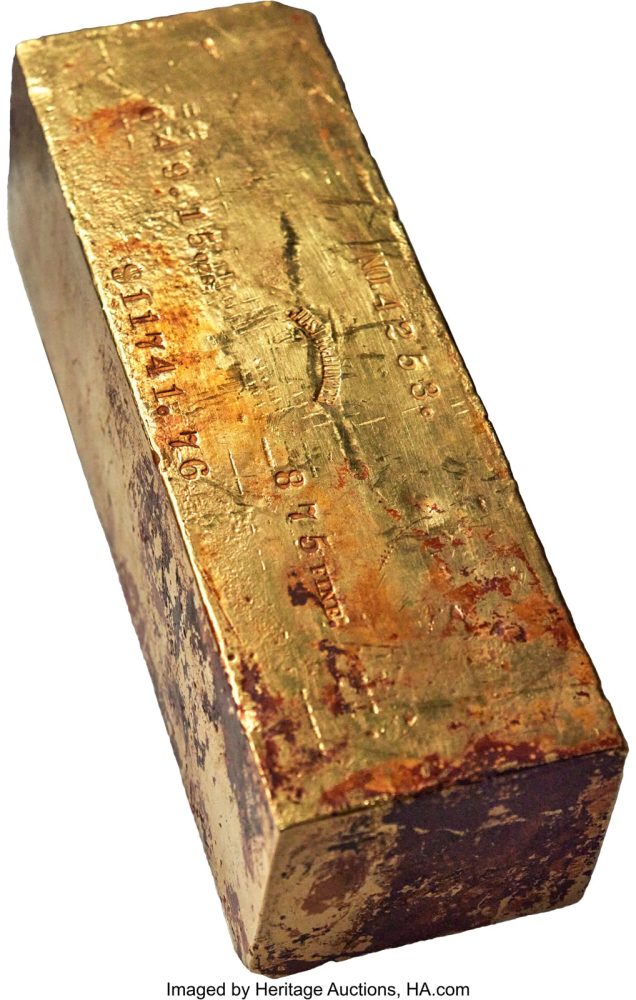

Serious collectors know a must-have treasure when they see one, and that was exactly what happened when a massive Justh & Hunter gold ingot crossed the auction block at Heritage Auctions’ April 30-May 4 CSNS US Coins Signature® Auction in which numerous new auction records were set. The last of 60 bids drove the final result for the ingot to $2.13 million to lead the total for the event to $31,691,002.

The ingot that led the U.S. Coins event, from The Marcello and Luciano Collection, is a behemoth, measuring 218 mm (nearly 8.6 inches) and weighing in 649.15 troy ounces, or just over 44.5 pounds.

“This is a magnificent result for a magnificent treasure, the second-largest ingot from the S.S. Central America that ever has been brought to auction,” says Todd Imhof, Executive Vice President at Heritage Auctions. “It is one of just 13 in the Colossal Size weight class (more than 500 ounces), and an appropriate leader for this event.”

The ingot was just one of four lots that topped $1 million, the other three coming from The Bruce S. Sherman Collection, Part II, a treasure trove assembled by Sherman, Chairman and principal owner of Major League Baseball’s Miami Marlins, that has been called “one of the most remarkable achievements in numismatics.”

The top lot from the Sherman collection was an 1835 HM-5, JD-1 Half Eagle, PR67+ Deep Cameo PCGS. CAC that is the finest of just three known examples and climbed to $1.8 million, smashing the previous auction record of $822,500. Few proof Classic Head half eagles are known, and of those, the example from the Sherman collection is believed to be finest, regardless of date. Of the 20 on Heritage’s roster, five are museum pieces, including one in the British Museum and four in the Smithsonian.

1835 HM-5, JD-1 Half Eagle, PR67+ Deep Cameo PCGS CAC

Another seven-figure record-setter was a 1792 Copper Disme, Judd-11, MS64 Red and Brown PCGS. CAC from the Sherman collection that drew 43 bids before ending at $1.5 million, surpassing the previous auction record of $1,057,500 set by Heritage in 2015. It is the finest by a wide margin of just three known examples of an outstanding rarity in the U.S. pattern series. The Mint experimented with reeded and plain edges on the copper dismes of this year, and the plain edge pieces are considerably scarcer.

1792 Copper Disme, Judd-11, MS64 Red and Brown PCGS CAC

The fourth lot to exceed $1 million was an 1803 Proof Draped Bust Dollar or Novodel, PR66 PCGS that is tied for the finest among just four known survivors and sold for $1.11 million – well above the previous auction record of $851,875 set by Heritage in 2013. Proof silver dollars from 1801-03 are known today as “novodels,” which are among the rarest and most valuable issues in the U.S. federal coinage series.

1803 Proof Dollar or Novodel, PR66

Another popular coin from the Sherman collection was an 1879 Coiled Hair Stella, Judd-1638, PR62 PGGS, a prize in such high demand that it drew 59 bids before closing at $576,000. Before it was acquired by Sherman, it was part of the famed Richmond Collection.

One of just 16 examples traced of an 1876-CC Twenty Cent Piece, MS64 reached $444,000. A landmark rarity in the U.S. silver series, the 1876-CC twenty cent piece often is mentioned in the same class as the famous 1804 dollar, 1913 Liberty Head nickel, and the 1894-S Barber dime and earned the “Duke of Carson City Coins” moniker from Rusty Goe. This example’s history, before ending up with Sherman, included stops in the collections of Louis E. Eliasberg and Eugene Gardner.

1876-CC Twenty Cent Piece, MS64

Nearly 100 bids poured in for a 1792 Half Disme, Judd-7, MS64 PCGS before it achieved $432,000. The 1792 half disme is among the most important issues in all of American coinage, was the first circulating coinage struck by the authority of the U.S. Congress, and is listed among the 100 Greatest U.S. Coins. The example in this auction has not been offered at auction in more than 20 years.

1792 Half Disme, Judd-7, MS64 PCGS

A 1794 B-1, BB-1 Silver Dollar, XF40 PCGS. CAC, the Gainsborough Specimen of America’s first silver dollar, brought a winning bid of $384,000. One of 10 lots in the auction from The Texas Republic Ranch Collection, it is a magnificent example of one of the historically significant pieces of American coinage, each personally handled by Mint Director David Rittenhouse.

1794 B-1, BB-1 Silver Dollar, XF40 PCGS CAC

A 1798 Draped Bust Small Eagle Dollar, MS62 PCGS brought $360,000. That figure surpassed the previous auction record of $216,000 for a 1798 Small Eagle, 15 Stars dollar that was set by Heritage in 2024, and also set a new auction record for any 1798 Small Eagle dollar.

1798 Draped Bust Small Eagle Dollar, MS62 PCGS

Complete results for the CSNS U.S. Coins event can be found at HA.com/1393.

This spectacular note is among the top offerings from the collection of Charlton Buckley, the former San Francisco-area businessman who pursued National Bank notes, large and small, as well as large and small size U.S. type notes, resulting in a trove of California Nationals and notes, including California Gold Bank Notes and Federal Reserve Notes.

“High-denomination notes always have exceptional appeal among collectors, and this is example is the perfect combination of collector demand and exceptional grade,” says Dustin Johnston, Senior Vice President of Numismatic at Heritage Auctions. “It has exceptional eye appeal, and when our consignor acquired it in in 2015, was one of the nicest offered $10,000s in the preceding half decade. Now, it’s a magnificent addition to a new collection.”

Also from the Buckley collection was a Fr. 2221-E $5,000 1934 Federal Reserve Note. PMG Choice Uncirculated 63 that drew a winning bid of $240,000. Prior to this event, it had appeared at auction just once before. The PMG Population Report includes 15 graded examples, with just one Fr. 2221-E graded equal and two graded higher.

A San Francisco, CA – $50 1870 Fr. 1160 The First National Gold Bank Ch. # 1741 PMG Fine 12 from the Buckley collection ended at $180,000. It is one of only seven $50 National Gold Bank Notes – six of which are from this San Francisco bank – listed in the National Currency Foundation census; one of the overall seven reported $50 National Gold Bank Note survivors is in multiple pieces and another likely off the market forever in the ANA museum, thus resulting in only five obtainable examples.

San Francisco, CA – $50 1870 Fr. 1160 The First National Gold Bank

A Fr. 2221-E $5,000 1934 Federal Reserve Note. PMG Very Fine 25 from the Buckley collection reached $144,000. Its serial number, E00000170A, is the highest among the 13 valid serial numbers listed in Track & Price. This event marked just the second time this note has been offered at auction.

Fr. 2221-E $5,000 1934 Federal Reserve Note. PMG Very Fine 25

Another collection featured in the event was the auction will include 54 lots from the Ronald R. Gustafson Collection, which produced 49 lots sold in the auction, including a Fr. 2220-A $5,000 1928 Federal Reserve Note. PMG Choice About Unc 58 that brought a winning bid of $288,000. One of just three documented Boston Series 1928 $5,000s, its popularity is due to the combination of grade and rarity. PMG has graded less than two dozen Series 1928 $5,000s, and this example is among the finest known of that small population.

Fr. 2220-A $5,000 1928 Federal Reserve Note. PMG Choice About Unc 58

Fr. 2231-F $10,000 1934 Federal Reserve Note. PMG Very Fine 30

Not all of the top results in the auction were for lots from featured collections. For example: a Fr. 187j $1,000 1880 Legal Tender PMG Very Fine 30 Net that ended at $180,000. This high-denomination rarity has a vignette of Columbus in His Study and a portrait of DeWitt Clinton, who was governor of New York during the years of 1825-28 and had earlier served three stints as the mayor of New York City. Track & Price lists 15 different serial numbers for this Friedberg number, one of which is part of an institutional collection.

Fr. 187j $1,000 1880 Legal Tender PMG Very Fine 30 Net

Fr. 2231-H $10,000 1934 Federal Reserve Note. PMG Extremely Fine 40

Fr. 2220-D $5,000 1928 Federal Reserve Note. PMG Very Fine 25

A beautiful Cincinnati, OH – $100 1875 Fr. 460 The Metropolitan National Bank Ch. # 2542 PMG About Uncirculated 55, an outstanding example of this very rare type and denomination, reached $120,000. Just one other is listed in the census with a CU grade, but that note, on a New York bank, never has appeared at public sale. Either way, the National Currency Foundation census does not list any other 1875 $100s above the 55 level, meaning this example very well could be the finest known.

Cincinnati, OH – $100 1875 Fr. 460 The Metropolitan National Bank

Complete results from the US Currency event can be found at HA.com/3598.

Victoria gold Proof “Una and the Lion” 5 Pounds 1839 PR62 Ultra Cameo

Among the most recognizable types in world numismatics, it remains an artistic masterpiece nearly two centuries after its creation.

“William Wyon is revered as one of the most accomplished and important engravers in all of British coinage,” says Cris Bierrenbach, Executive Vice President of International Numismatics at Heritage Auctions, “and this is a beautiful example of the coin that is considered his crowning achievement, one that exhibits his extraordinary technical skill and artistry. This is the kind of coin that immediately becomes a centerpiece of a collection.”

A Louis XIII gold 10 Louis d’Or 1640-A AU Details (Cleaned) NGC drew a winning bid of $264,000. This is a Draped Bust variety of this rarity, offered at Heritage for the first time, which helps to explain the immense demand for the type. As early as 1690, F. Leblanc suggested that they were fantasy pieces possibly struck for the king’s pleasure rather than for circulation. Later scholarship reversed course and posited the likelihood that these were struck for commerce, though the possibility remains that they remain fantasy pieces or trial strikes. Documents from the French National Archives confirm Jean Warin as the original engraver in 1640.

Louis XIII gold 10 Louis d’Or 1640-A AU Details (Cleaned) NGC

An Edward VIII bronze Matte Proof Pattern 1/2 Penny 1937 PR64 Brown NGC, from the Cara Collection of highly provenanced British Rarities, blew past pre-auction estimates when it climbed to $180,000 – a record for any minor of Edward VIII. This magnificent coin is just the fourth example of any Edward VIII coinage offered at Heritage in the last half decade, and is presumed to be unique, as no other Matte Proofs of this denomination have surfaced; examples even have eluded the British Museum and Royal Mint collections, in which only brilliant Proofs reside.

Edward VIII bronze Matte Proof Pattern 1/2 Penny 1937 PR64 Brown NGC

Also from the Cara Collection was an Oliver Cromwell gold Proof Pattern Broad of 20 Shillings 1656 PR63 PCGS that drew nearly two dozen bids on its way to $126,000. This coin is one of the most sought-after British gold types, not only due to its sheer rarity, but its historical implications from one of the most tumultuous eras in English history. This example is tied with three others atop the PCGS population report.

Oliver Cromwell gold Proof Pattern Broad of 20 Shillings 1656 PR63

The collection produced half of the six-figure results in the auction, a list that also included an Anne gold Pattern Guinea 1702 AU55 NGC that ended at $102,000. A treasure of English numismatics, it is the first Guinea Pattern ever struck by the Royal Mint, with fewer than five known examples. This auction marked the first time this type ever had been offered at Heritage. This type carries considerable cache, considering it was minted under the management of famed physicist and then-mint master Sir Isaac Newton.

Anne gold Pattern Guinea 1702 AU55

Other top lots from the Cara Collection included, but were not limited to:

A Victoria gold Proof 5 Pounds 1887 PR66+ Deep Cameo PCGS, the finest certified example of the most revered emission from Victoria’s legendary Golden Jubilee Proof Set, ended at $168,000. This remarkable example is so void of abrasions or other blemishes that it looks like it could have been struck yesterday.

Victoria gold Proof 5 Pounds 1887 PR66+ Deep Cameo

Other highlights in the auction included, but were not limited to:

Complete results for the World & Ancient Coins event can be found at can be found at HA.com/3123.

About Heritage Auctions

Heritage Auctions is the largest fine art and collectibles auction house founded in the United States, and the world’s largest collectibles auctioneer. Heritage maintains offices in New York, Dallas, Beverly Hills, Chicago, Palm Beach, London, Paris, Amsterdam, Brussels, Munich, Hong Kong and Tokyo.

Heritage also enjoys the highest Online traffic and dollar volume of any auction house on earth (source: SimilarWeb and Hiscox Report). The Internet’s most popular auction-house website,HA.com, has more than 1,960,000 registered bidder-members and searchable free archives of more than 7,000,000 past auction records with prices realized, descriptions and enlargeable photos.

TKO Group reported better-than-expected first-quarter revenue but profit fell short.

The WWE and UFC parent also closed its acquisition of some properties from Endeavor Group Holdings in the quarter.

TKO Group lifted its revenue and adjusted EBITDA outlook for the full year, excluding the impact of the new businesses.

TKO Group Holdings (TKO) posted a mixed earnings report after the bell Thursday, as revenue came in well above estimates but profit fell short.

The owner of World Wrestling Entertainment and Ultimate Fighting Championship generated $1.27 billion in revenue, above Visible Alpha estimates of $899.6 million. However, TKO reported earnings per share of $0.69 when analysts were expecting $0.77.

“Our conviction in our portfolio of assets is strong and we are now focused on integration, driving synergies, the domestic media rights deal for UFC, and our capital return programs,” CEO Ariel Emanuel said.

TKO Lifts Full-Year Revenue, Adjusted EBITDA Outlook

TKO closed its acquisition of several properties from Endeavor Group Holdings during the quarter, including IMG, On Location, and Professional Bull Riders. The growing sports conglomerate was also one of the four companies added to the S&P 500 in the quarter.

Excluding the impact of the new businesses, TKO lifted its full-year revenue forecast to a range of $3.005 billion to $3.075 billion, up from the prior $2.930 billion to $3.000 billion. It also lifted its 2025 adjusted EBITDA forecast to $1.390 billion to $1.430 billion from $1.350 billion to $1.390 billion.

Shares initially rose Friday morning but turned lower and recently were down nearly 6%. They have gained about 12% since the start of the year.

Ron Bain is CFO of Vaalco Energy, a Houston-based upstream oil and gas company with a strong presence in Africa and Canada. Founded in 1985, Vaalco is dual-listed on the New York and London stock exchanges.

Global Finance: You have been CFO for almost four years. How has Vaalco’s competitive position changed during your tenure?

Ron Bain: It’s been an active period during which we have delivered several transformative transactions that increased scale and diversified the asset portfolio. We completed a value-accretive corporate merger with Transglobe in 2022 that saw us acquire operating assets in Egypt and Canada. More recently, we acquired a non-operating interest in a producing field in Cote d’Ivoire through the acquisition of Svenska AB.

“In addition, we continue to drive organic growth across the portfolio with drilling campaigns, while expanding our footprint by adding new licenses that provide long-term upside potential. All of this leaves Vaalco well placed to consolidate its position as a leading independent exploration and production company.”

GF: What makes this business and industry a distinctive challenge for a CFO?

Bain: It’s a very exciting, fluid, and cyclical sector in which there is a lot of deal-making, a lot of investment, and the requirement to deploy material capital across the portfolio to deliver growth. The role of the CFO is to ensure access to capital to support growth objectives as well as work with the finance team and executive to mitigate risk: for example, through implementation of hedging instruments to protect the company against commodity downside.

GF: What absorbs most of your energy and time?

Bain: Most of my time is spent ensuring we maintain a robust balance sheet that balances organic and inorganic growth alongside our commitment to shareholder return. Vaalco is dual-listed in London and New York, so I also spend a lot of time engaging with our investors and wider stakeholders, overseeing our regulatory commitments to those listings, and playing a big role in the development of our strategy and our ESG agenda.

GF: What makes for a great finance team?

Bain: It’s important to have good communication within the team, so everybody knows the objectives and their respective roles in achieving those objectives. I am fortunate to have a great finance team across all our areas. I also have a close working relationship with our CEO, George Maxwell, having worked alongside him at our previous company, Eland Oil & Gas, which achieved a good exit for all stakeholders a few years ago.

GF: What is the role of AI in the finance function? How do you see it evolving at Vaalco?

Bain: AI is already in use in finance at Vaalco. We use AI-powered software to handle data entry as well as invoice processing with optical character recognition that extracts process data from receipts and documents with minimal human intervention. We implemented a global ERP system in 2024 and are collecting huge amounts of datasets through it. With the internet of things and the ability to integrate meter readings and monitoring gauges, we see machine learning models reading and learning from these large datasets to improve our decision-making.

GF: What keeps you up at night?

Bain: Economic and market uncertainty, together with an increased administrative burden via greater government regulation. My responsibility is, first, to ensure the company is performing for the benefit of all of our stakeholders. We have a lot of employees, so we must demonstrate that we are good corporate citizens and oversee a safe working environment.

We see ourselves as partners to the host governments in the countries where we operate, so we have a responsibility to the people of those countries to deliver a positive impact through our activities. As an operator of material-producing assets, we must always demonstrate operational excellence and environmental stewardship.

On June 11, 2025, Lugano will host the third edition of MetaForum, the event organized by FinLantern with the partnership of The Cryptonomist, taking place at the Hotel De La Paix.

After the success of the previous editions, the event is confirmed as a point of reference for enthusiasts and professionals in the blockchain, crypto, and digital innovation sector.

MetaForum 2025 will focus on highly topical issues, including the evolution of the cryptocurrency market, asset tokenization, privacy and regulatory compliance (KYC/AML), the synergies between artificial intelligence and blockchain, smart contracts, decentralized finance (DeFi), NFTs, and the metaverse.

The event will offer a day full of conferences, panels, workshops, and high-level networking moments, with the participation of speakers of international prominence. Among the confirmed speakers are experts such as Giacomo Zucco, Ferdinando Ametrano, Amelia Tomasicchio, but also representatives from companies like Binance, SwissBorg and many others.

Among the sponsors of the event, we also find Best Wallet, CheckSig, Avatrade and exceptional partners such as the association Crypto Valley. The program also includes thematic panels on topics such as communication in Web 3.0, the use of the metaverse by brands, and the regulation of cryptocurrencies in the European Union.

MetaForum is aimed at a diverse audience, which includes international experts in crypto and blockchain, investors, family offices, venture capitalists specialized in fintech, CTOs, CIOs, tech startups, digital transformation managers, and technology enthusiasts.

The event represents a unique opportunity to deepen knowledge, create professional connections, and discover the latest trends in the sector.

Currently, the ticket is on sale at the price of 87 CHF.

For further information and to register for the event, you can visit the official website of MetaForum.

Expedia Group shares fell sharply Friday morning, a day after the travel booking platform fell short of first-quarter estimates.

Revenue and gross bookings came in lower than forecast, and the company’s net loss widened from the same time last year.

Executives said demand has been weak in the U.S. to start the year, as Expedia also lowered its booking and revenue growth forecasts.

Shares of Expedia Group (EXPE) tumbled 10% in premarket trading Friday, a day after the travel platform’s first-quarter results came in worse than expected and it lowered its full-year outlook amid weak U.S. demand.

The company behind its namesake travel booking platform and others like Vrbo and Hotels.com reported revenue of $2.99 billion and $31.45 billion in total bookings, both up from the same time last year but below what analysts polled by Visible Alpha had expected.

Expedia posted adjusted earnings per share of $0.40, up 90% year-over-year and better than Visible Alpha consensus, but its reported net loss per share of $1.56 was more than triple the $0.42 that analysts had forecast.

‘Weaker Than Expected’ US Demand Leads to Lowered Outlook

CEO Ariane Gorin said the company managed to grow bookings and revenue “despite weaker than expected demand in the U.S.” as consumer sentiment has worsened amid tariff-fueled uncertainty. Gorin added on the earnings call that travel trends continued to be soft through April, and said more European customers appear to be traveling to other locales like Latin America rather than the U.S., according to a transcript provided by AlphaSense.

CFO Scott Schenkel said Expedia projects 2% to 4% bookings growth and 3% to 5% revenue growth in the second quarter, but the company trimmed its full-year forecast for both metrics to 2% to 4% growth from the 4% to 6% rate they laid out in last quarter’s earnings call.

Shares entered the day down more than 9% since the start of the year.

The Federal Reserve (Fed) remains in wait-and-see mode, letting economic conditions play out before making any policy moves. Unlike 2019, when it acted pre-emptively, the Fed claims that there’s no urgency for intervention, and stagflation concerns aren’t front and center, at least not yet. Still, Powell’s worst fears could already be unfolding, with ISM manufacturing price trends potentially informing inflation in the coming weeks, even as front-running distorts short-term data.

Markets are riding a wave of optimism, with US stocks rallying Thursday on hopes of lower tariffs. The White House is framing this as a trade war victory, buoyed by the UK trade deal announcement and upcoming talks with China. The S&P 500 and Nasdaq 100 both gained over 1%, erasing earlier losses and hitting their highest levels since March. However, the baseline 10% tariff remains unchanged, signaling that double-digit tariffs are likely here to stay. The deal grants preferential tariff access for UK-imported vehicles and partial relief for steel and aluminum products. In exchange, the UK opened its market to $5 billion in US exports, primarily in agriculture, chemicals, and machinery. The big question remains, are markets getting ahead of themselves? While sentiment is strong, the true economic impact of tariffs has yet to unfold. Time will tell if this optimism can sustain markets through the summer.

The dollar, which didn’t have the same level of participation in the recent rally, has rebounded this week on trade optimism, climbing past 100 for a second straight session, fueled by hopes that the US-UK trade deal could be the first of several. Yesterday, the greenback gained most against the yen and Canadian dollar but gains against the British pound were limited after the Bank of England (BoE) delivered a widely expected rate cut while striking a surprisingly hawkish tone.

CAD hinges on dollar strength

Kevin Ford – FX & Macro Strategist

After the Fed meeting on Wednesday, the Loonie extended its losses, reinforcing downward pressure. The UK-US trade deal discussions triggered a stronger rebound, pushing the DXY back above the 100 level and sending USD/CAD to 1.393—its highest point of the week. As previously noted, short-term rate differentials between the U.S. and Canada continue to widen, solidifying 1.38 as a key support level. The Loonie may pause around 1.394 before making a potential move toward 1.40 in the coming days. With DXY reclaiming the 100 level and VIX easing, upward momentum now appears more likely.

On the macro side, the Bank of Canada’s annual Financial System Survey offers a snapshot of key financial risks, resilience, and emerging trends, drawing insights from senior risk management experts. This year’s results highlighted concerns over rising household debt and the growing influence of leveraged hedge funds in government-bond auctions, factors that have cooled expectations for an imminent rate cut and reinforced a more cautious stance on monetary policy.

The Canadian bond market didn’t take the news well, with 10-year government bond yields jumping above 3.22%, hitting a two-week high. A mix of domestic and regional pressures continues to push longer-term borrowing costs higher. Meanwhile, the government’s ramped-up bond issuance to finance fiscal initiatives is adding to supply, keeping yields elevated.

UK-US trade deal is symbolic at best

George Vessey – Lead FX & Macro Strategist

It is the first trade deal agreed after President Trump began his second presidential term in January, and after he imposed strict tariffs on countries around the world in April. It is symbolic for this reason, but we think it reinforces our view that tariffs are unlikely to go away anytime soon. Still, markets are cheering the news. The main beneficiary in the FX space has been the US dollar, with GBP/USD erasing its earlier gains to trade closer to $1.32. Elsewhere, sterling appreciated across the board, finally hurdling the €1.18 handle versus the euro and jumping over 1% against the Japanese yen, though these gains have been partially eroded overnight.

The final details of the UK-US trade pact will still be negotiated over the coming weeks, but here’s what we know. The UK steel and aluminium industries will no longer face any tariffs after they had 25% duties placed on them. The deal appears to centre predominantly around cars, the US’ sixth-top export to the UK and the UK’s top export to the US. The first 100,000 vehicles imported into the US by UK car manufacturers each year are subject to the reciprocal rate of 10% and any additional vehicles each year are subject to 25% rates. That’s a change from the 25% tariff in place for foreign cars shipped to the US but still leaves UK carmakers worse off than before.

Moreover, in our view, given 10% tariffs will remain on most other UK goods into the US, this trade deal is not a positive indicator for broader tariff de-escalation. With the US running a $12bn goods trade surplus with Britain in 2024, the UK’s inability to negotiate a lower rate suggests nations with US trade deficits may face even tougher terms.

CPI points to slowing easing cycle

Kevin Ford – FX & Macro Strategist

Mexico’s inflation has settled below 4%, though it still sits above the central bank’s target of 3%. In April, core annual inflation ticked up to 3.93%, slightly above forecasts—with monthly inflation rising by 0.49%. Prices for food, beverages, tobacco, and services have edged higher, even though energy and agricultural goods have dipped slightly. This marks the sharpest annual price increase so far this year, reinforcing many policymakers’ careful approach amid easing trade tensions.

Weak domestic demand and growing economic slack are keeping upward price pressures in check, while lower oil prices and favorable base effects provide some relief. Although last year’s peso depreciation pushed inflation higher, recent peso gains since December suggest these effects may be short-lived. Overall, the latest CPI data point to a cautious outlook when it comes to Banxico’s easing cycle.

A widening negative output gap and slower global growth, fueled by U.S. tariffs, support the idea of lower interest rates, though persistent inflation risks may limit how far rates can drop. Banxico may need to moderate its pace of rate cuts as conditions evolve, while recent Q1 GDP growth and a new fiscal support package are expected to boost domestic demand over the coming months.

The Mexican peso reacted to the CPI data by drifting toward 19.50, its five-year average, and approaching a six-month high. Earlier in the week, the peso tested 19.78 before retreating, showing a steady move toward 19.50 as the week wrapped up. With expectations of a more dovish Banxico, markets are now anticipating a shift in the central bank’s stance as it looks to balance inflation and growth over the medium term.

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quothave a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Pinterest shares are jumping 13% in premarket trading Friday, a day after the social media service reported first-quarter revenue and global monthly active user figures that topped estimates.

Monthly active users surged 10% year-over-year to a record 570 million.

Pinterest shares entered Friday down 4% year-to-date.

Pinterest (PINS) shares are jumping 13% in premarket trading Friday, a day after the social media service reported first-quarter revenue and global monthly active user figures that topped estimates.

The company posted earnings per share (EPS) of $0.01 on revenue that increased 17% year-over-year on a constant currency basis to $855.0 million. Analysts polled by Visible Alpha projected a loss of a penny per share on revenue of $846.9 million. Adjusted EPS of $0.23 missed estimates.

The San Francisco-based firm’s monthly active users increased 10% to a record 570 million, beating estimates of 563.4 million.

Q2 Revenue Projection Tops Estimates

Pinterest, which has rolled outartificial intelligence (AI) tools for advertisers, said it expects second-quarter revenue between $960 million and $980 million, which would represent 12% to 15% growth. The midpoint of the range exceeded Visible Alpha consensus of $964.2 million.

“The fundamentals in the business are strong and we’re continuing to see healthy growth,” Pinterest CEO Bill Ready said. “Our AI advancements are helping users take action and make more intentional shopping decisions.”

Pinterest shares entered Friday down 4% year-to-date.

A potential thawing in trade relations between the US and China boosted sentiment. Chinese and US negotiators will meet in Switzerland from May 9–12 for trade negotiations, chaired by Chinese Vice Premier He Lifeng.

US President Donald Trump said he expected “substantive” reduction in Chinese tariffs and highlighted a UK-US trade deal as an example of the benefits of his tariff policies.

On the macro front, any chance of a Federal Reserve rate cut in May was eliminated by a stronger than expected US nonfarm payrolls result.

As such, the Federal Reserve kept interest rates on hold at its 7 May meeting and indicated that the current uncertain environment means the central bank cannot provide guidance around further cuts.

Across the pond, the Bank of England did cut rates, but the BoE’s cautious commentary saw the move characterised as a “hawkish cut”.

In FX markets, the initial focus was on Asia. The US dollar was hit in a historic sell-off in the USD/TWD pair, causing the Taiwanese dollar to surge higher. The move corresponded with US-Taiwan trade talks and some commentators suggested the Taiwan government might allow the TWD to rise – “appreciation by stealth”.

The USD staged a recovery following the Fed decision with the USD index reaching a one-month high at the end of the week. The euro and British pound were the underperformers.

Global Macro Global central banks diverge

Fed holds amid scrutiny. After holding rates steady for the third consecutive meeting, the Fed acknowledged growing uncertainty in the economic outlook, emphasizing the increasing risks of both higher unemployment and rising inflation. During the press conference, Powell faced pressure on questions about soft data and the rationale behind pre-emptive rate cuts by other central banks. He reiterated the Fed’s stance that soft data, while informative, has yet to be reflected in hard data, justifying a cautious approach. Powell also reminded markets that current conditions are not comparable to 2019, when three pre-emptive rate cuts were necessary. Market expectations for rate cuts have adjusted, with investors pricing in three reductions by the end of 2025. However, the likelihood of the first cut occurring in July has diminished, reflecting the Fed’s commitment to a no-rush, hard-data driven strategy.

BoE hawkish cut. The Bank of England (BoE) cut interest rates by a quarter point to 4.25% as expected. The BoE’s nine-person Monetary Policy Committee was split between the five members who supported the quarter-point cut, two who favored a bigger, half-point reduction and two who wanted rates to stay at 4.50%. Most market participants reckoned a near-unanimous vote for at least a 25-basis point cut. However, it turns out the picture was more complex, with two voting for rates to be held – meaning the decision leaned more hawkish than expected.

Inflationary pressures in ISM. ISM Services PMI surprised to the upside, rising to 51.6 in April from a nine-month low of 50.8 in March, exceeding forecasts of 50.6. New orders and inventories accelerated, reaching 52.3 and 53.4, respectively, while business activity held in expansion territory at 53.7. Price pressures remain a concern, prices charged, as measured by the ISM Manufacturing PMI Price Index, climbed for the fifth straight month.

Regional outlook: US & UK Handshake trade deal

Symbolic. It is the first trade deal agreed after President Trump began his second presidential term in January, and after he imposed strict tariffs on countries around the world in April. It is symbolic for this reason, but the details reinforce our view that tariffs are unlikely to go away anytime soon.

Details subject to revisions. The final details of the pact will still be negotiated over the coming weeks, but here’s what we know. The UK steel and aluminium industries will no longer face any tariffs after they had 25% duties placed on them. The deal appears to centre predominantly around cars, the US’ sixth-top export to the UK and the UK’s top export to the US. The first 100,000 vehicles imported into the US by UK car manufacturers each year are subject to the reciprocal rate of 10% and any additional vehicles each year are subject to 25% rates. That’s a change from the 25% tariff in place for foreign cars shipped to the US but still leaves UK carmakers worse off than before.

Markets are upbeat. Markets are riding a wave of optimism though, with US stocks rallying on hopes of lower tariffs. The White House is framing this as a trade war victory, buoyed by the UK trade deal announcement and upcoming talks with China. The S&P 500 and Nasdaq 100 both gained over 1%, erasing earlier losses and hitting their highest levels since March.

Premature celebration? However, could it be that investors are too optimistic about trade talks? The baseline 10% tariff remains unchanged on the UK, signaling that double-digit tariffs are likely here to stay. With the US running a $12bn goods trade surplus with Britain in 2024, the UK’s inability to negotiate a lower rate suggests nations with US trade deficits may face even tougher terms.

Week ahead Inflation and growth metrics dominate the agenda

Inflation data in focus. Key inflation readings across major economies will be closely monitored this week. In the US, the Consumer Price Index (CPI) for April is due on Tuesday, with the year-on-year rate expected to remain steady at 2.4%, while the month-on-month rate is forecasted to tick up slightly to 0.3% from -0.1%. Germany will release its final April CPI figures on Wednesday. France will follow suit on Thursday. These figures will provide critical insights into the inflation trajectory across the Eurozone as the ECB continues to monitor price pressures.

Growth readings to highlight economic momentum. A suite of GDP data releases will give markets important signals about global growth trends. Japan reveals its preliminary Q1 GDP figures on Friday, where the annualized growth rate is expected to decelerate to -0.4% from 2.2%. The UK’s Q1 preliminary GDP data on Thursday is expected to show marginal growth, with both quarterly and annualized rates were at 0.1% and 1.5%, respectively. The Eurozone will also release its Q1 second estimate GDP data on the same day as well.

Labor markets and consumer sentiment. The UK will also report key labor market data on Tuesday. Average weekly earnings for March was last reported at 5.6% year-on-year, while the unemployment rate was at 4.4%. In the US, initial jobless claims will be released on Thursday, offering further signals on the state of the labor market. Additionally, US consumer sentiment will be gauged through the preliminary release of the University of Michigan’s Sentiment Index on Friday, expected to show a slight improvement to 53 from 52.2.

Central bank watch. While no major central bank decisions are scheduled, the upcoming economic data will be closely watched for its implications on monetary policy. Australia’s employment data on Thursday could influence RBA expectations, with consensus forecasting a 25k increase in employment and an unemployment rate holding steady at 4.1%.

FX Views Positive trade news boosts dollar

USD Bear market correction?The US dollar index rose to a 4-week high, boosted by trade optimism following the US-UK trade deal. But another key talking point this week was the massive rally in the Taiwanese dollar – raising concerns of USD-rich Asian countries being the catalyst for the next broader USD decline. The USD’s slide this year has pressured heavily exposed economies like Taiwan, prompting investors to ramp up hedging and diversify beyond US assets, which fits into the structurally bearish USD case. Meanwhile, the Fed’s decision to hold rates unchanged and markets paring easing bets had minimal positive impact on the buck. Indeed, the dollar’s lackluster rebound relative to US equities is noteworthy too, suggesting a weak USD bear market correction is in play. The risk of a structural USD bear market remains elevated for three main reasons. 1) US policymakers seem inclined toward a weaker dollar. 2) Policy credibility is under strain due to fiscal uncertainty, erratic tariff policy, and Fed independence concerns. 3) The fading narrative of US exceptionalism. US inflation data will be a key focus in the upcoming week.

EUR Fading volatility is a drag. The euro continues to oscillate between $1.12 and $1.14 versus the US dollar, lacking a fresh positive catalyst to drive it higher for now. EUR/USD closed below the 21-DMA for the first time in three weeks, but this could be a sign of a healthy correction. Indeed, the premium to own bullish euro exposure versus the dollar remains elevated. Broadly speaking, the euro’s 9% surge this year has fuelled concerns over stretched positioning, but the real threat is fading volatility. Gains for the common currency have been supported by Germany’s fiscal pivot and diversification away from US assets, but a sizable chunk of the upside move has come from the volatility regime itself. The Bloomberg EURO index shows its strongest correlation to a one-month FX volatility gauge in nearly five years. With volatility drifting lower, the euro’s upside momentum is losing steam, even as options markets still reflect dollar bearishness. A dip below $1.13 appears corrective rather than a trend reversal, provided the $1.1200–$1.1220 support zone holds. Ultimately, the bullish momentum is under pressure, but we think the direction remains intact.

GBP Trade optimism & hawkish BoE. The pound marginally outperformed most of its peers when the news of a UK-US trade deal broke. However, the initial move higher in sterling faded given the limited nature of the agreement. The bottom line is that post-deal tariffs on the UK will remain substantially higher than before Liberation Day. The dollar was the main beneficiary of the trade optimism as well, dragging GBP/USD towards $1.32 after the pair tested its 100-DMA at $1.3337 following the hawkish BoE rate cut. The pair has closed below its 21-DMA in a sign of near-term bullish moment waning. However, in the options space, GBP long-term sentiment hit the least bearish since 2014. Elsewhere, with tariff-induced volatility subsiding, rate differentials could return to the driving seat for GBP/EUR. Monetary policy divergence means GBP/EUR could close the gap on UK-DE rate spreads. The swap differential suggests the pair should be trading above €1.19. Coming up, a big week of UK data beckons with labour market figures and Q1 GDP results under the microscope.

CHF Negative rates not ruled out. It’s been a quiet week for the safe haven Swiss franc amidst the rebound in global risk appetite. But the main story to watch over the next few weeks is how the Swiss National Bank (SNB) will respond to the sharp 9% rise of the franc versus the US dollar year-to-date, which hit a decade high last month. According to the SNB President Martin Schlegel recently – policymakers remain ready to intervene in FX markets if needed for price stability. The most recently available data, for the final quarter of 2024, showed the central bank largely keeping out of FX markets for a year. An alternative to dissuade flows into the franc would be to cut borrowing costs again but the challenge is clear – policy rates are already at 0.25%, leaving little room to manoeuvre without dipping into negative territory. A move below zero could strain the banking sector, eroding profitability and complicating financial conditions.

CADLoonie rebounds on USD strength. USD/CAD posted a strong performance in April, but it remains the weakest among its G10 peers, making it the worst-performing major currency in 2025. After the Fed meeting on Wednesday, the Loonie extended its losses, reinforcing downward pressure. The UK-US trade deal discussions triggered a stronger rebound, pushing the DXY back above the 100 level and sending USD/CAD to 1.393—its highest point of the week. As previously noted, short-term rate differentials between the U.S. and Canada continue to widen, solidifying 1.38 as a key support level. The Loonie may pause around 1.394 before making a potential move toward 1.40 in the coming days. With DXY reclaiming the 100 level and VIX easing, upward momentum now appears more likely.

Meanwhile, Canada’s macro outlook remains fragile. Recent data confirmed a fifth straight month of private-sector contraction, with the S&P Global Composite PMI dipping to 41.7 in April from 42 in March—its sharpest decline since June 2020. Both manufacturing and services posted similar slowdowns, while new orders saw a steep drop, adding further weight to concerns about growth.

AUD Labor party victory spurs fiscal optimism. The Australian Labor Party’s significant election victory reinforces the likelihood of continued fiscal stimulus, which is supportive of the Australian economy. Markets will watch for the passing of key legislation, including higher taxes on superannuation balances above AUD 3 million. On the economic front, robust fiscal spending may provide additional tailwinds to growth. AUD/USD still hovering above 0.6400 handle, converging toward the upper Bollinger Band with increased upward momentum. Price action remains above the Ichimoku Cloud, affirming a positive bias. Key support levels lie at the 200-day EMA (0.6409) and 21-day EMA (0.6384), while resistance targets include 0.6545 and 0.6688. Upcoming data on Australian employment and trade balance will be key.

CNYPBoC rate cuts spur negative momentum. The PBoC’s recent rate cuts, including a 50bp cut in the reserve requirement ratio and a 10bp cut to the seven-day reverse repo rate, aim to inject liquidity and support economic recovery. Measures to mitigate the impact of US tariffs and stimulate domestic growth are likely to weigh on the yuan in the medium term. USD/CNH has rebounded and is now on track to test next daily key resistance levels of 200-day EMA of 7.2518, followed by 21-day EMA of 7.2635. Downside targets extend to 7.1475. USD/CNH is still more than 2% away from its mid April 2025 daily highs of 7.4290. Focus will shift to trade balance, CPI, and PPI data for further cues on the yuan’s trajectory.

JPY USD/JPY struggles as BoJ balances risks. Bank of Japan (BOJ) Governor Kazuo Ueda reiterated concerns about price deflation risks and uncertainties surrounding high inflation, signaling caution in monetary policy adjustments. Ueda highlighted Japan’s inflation trajectory, projecting it to near the 2% target in the latter half of the three-year outlook period ending March 2028. While the BOJ remains committed to gradual policy normalization, the central bank is balancing this with external risks, including weaker global growth and geopolitical uncertainties, which could threaten Japan’s fragile recovery. USD/JPY however, has struggled to sustain its upward momentum. It is now hovering at its 21-day EMA (144.09) with the next key resistance levels of 50-day EMA (146.17) and 200-day EMA (150.03) next. A potential head-and-shoulders pattern on the weekly chart suggests deeper declines if support at 140.85 (near eight-month of the weekly lows) fails. Market participants will monitor Japan’s current account, GDP, and industrial production data closely.

MXN. Peso steady at 5-year average.

Mexico’s inflation has settled below 4%, though it still sits above the central bank’s target of 3%. In April, core annual inflation ticked up to 3.93%, slightly above forecasts—with monthly inflation rising by 0.49%. Prices for food, beverages, tobacco, and services have edged higher, even though energy and agricultural goods have dipped slightly. This marks the sharpest annual price increase so far this year, reinforcing many policymakers’ careful approach amid easing trade tensions.

Weak domestic demand and growing economic slack are keeping upward price pressures in check, while lower oil prices and favorable base effects provide some relief. Although last year’s peso depreciation pushed inflation higher, recent peso gains since December suggest these effects may be short-lived. Overall, the latest CPI data point to a cautious outlook when it comes to Banxico’s easing cycle.

The Mexican peso reacted to the CPI data by drifting toward 19.50, its five-year average, and approaching a six-month high. Earlier in the week, the peso tested 19.78 before retreating, showing a steady move toward 19.50 as the week wrapped up. With expectations of a more dovish Banxico, markets are now anticipating a shift in the central bank’s stance as it looks to balance inflation and growth over the medium term.

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.