Companion bills were introduced in the U.S. House and Senate last week to create a new type of tax-free savings account for all Americans.

If passed, it would allow you to put annual contributions in a Universal Savings Account (USA), where your earnings could grow tax-free.

Offering the same tax benefits as a Roth IRA, a USA would be more flexible, allowing you to withdraw at any age without penalty.

Will this be better than a high-yield savings account? It all depends on what return you can earn with a USA and what tax bracket you’re in.

The full article continues below these offers from our partners.

A New Kind of Tax-Free Savings Account

On May 1, Sen. Ted Cruz (R-Texas) and Rep. Diana Harshbarger (R-Tenn.) introduced companion bills for a Universal Savings Account (USA) Act. The legislation proposes creating a new type of tax-advantaged account that would allow all Americans to put money in savings that can earn interest that isn’t taxed.

If that kind of tax benefit sounds familiar, you may be thinking of a Roth IRA, which is a retirement account that lets you contribute a certain amount each year into a retirement fund where money grows tax-free. But unlike a Roth, which requires you to wait until age 59-1/2 to withdraw your funds without penalty, a USA would allow withdrawals at any time, no matter your age.

The money you could put in a USA would be post-tax dollars, just like the money you put into a Roth IRA. That means you can’t claim a tax deduction for your contribution. Instead, the tax break comes from not having the earnings taxed.

As currently proposed, the contribution limit for a USA is larger than for a Roth. The USA Act indicates a maximum contribution in Year 1 of $10,000, to be increased $500 each year until reaching a maximum annual limit of $25,000. By contrast, the most you can put into a Roth IRA in 2025 is $7,000 (or $8,000 for those age 50 and older).

In addition, the USA Act does not indicate that eligibility to make contributions is tied to any income limits. That differs from Roth IRA rules, which begin phasing out eligibility once a single tax filer reaches a modified adjusted gross income (MAGI) of $150,000, or a married couple filing jointly has a MAGI of $236,000.

Universal Savings Account (USA) vs. High-Yield Savings Account

So, how would a possible Universal Savings Account stack up against one of today’s best high-yield savings accounts? As with many questions, the answer is that it depends. First, it depends on what you can earn with a USA. And second, your tax bracket matters.

Let’s say you can earn 4% with a standard high-yield savings account. The interest you earn from the bank or credit union would be taxed as regular income, meaning you’ll get to keep something less than 4%. How much less is a factor of your tax bracket, which you can look up using the table below based on your taxable income.

If you’re in, say, the 22% tax bracket, you’ll keep 78% of your interest earnings (100% minus your 22% tax rate). Multiplying 0.78 by 4% leaves you with a net interest rate of 3.12%. You can see all our calculations below for a starting taxable interest rate of 3% or 4%.

Your tax bracket

3.00% taxable interest

4.00% taxable interest

10%

2.70% after-tax

3.60% after-tax

12%

2.64% after-tax

3.52% after-tax

22%

2.34% after-tax

3.12% after-tax

24%

2.28% after-tax

3.04% after-tax

32%

2.04% after-tax

2.72% after-tax

35%

1.95% after-tax

2.60% after-tax

37%

1.89% after-tax

2.52% after-tax

Knowing these numbers allows you to see how much you’d have to earn in your USA in order to out-do a taxable high-yield savings account. If, for instance, you can only earn 2.00% in a USA, you’d be better off with a 3% taxable savings account that nets over 2%, unless you’re in the 35% or 37% tax bracket.

But if instead you can get close to the same rate with a USA as with a top high-yield savings account, or you are in a very high tax bracket, then a USA’s tax savings will pay off. It comes down to doing the math on what your after-tax interest rate will be for a standard account vs. your tax-free rate from a USA.

One Way a USA Could Be Huge Winner

You can likely benefit the most from a USA if you’re able to sock away money each year and not touch it for a while, allowing you to invest your money for bigger gains. Like Roth IRAs, USAs would allow the purchase of stocks, bonds, ETFs, etc., allowing much larger gains over time. However, this type of investment is not recommended for funds you may want to access in the short term.

For Now, Here’s Where You Can Earn the Most on Your Cash

Time will tell whether this proposed legislation passes, and whether Universal Savings Accounts will enter the marketplace and the tax code. In the meantime, it’s always smart to make sure you’re earning a competitive return on your money in the bank. We make that homework easy by publishing our national rankings of the highest bank deposit rates every business day.

Right now, our daily ranking of the best high-yield savings accounts includes 15 accounts that pay between 4.35% and 5.00% APY, all with the flexibility to withdraw your funds whenever you want.

In addition, you could commit a portion of your savings to a certificate of deposit (CD). The advantage of a CD is that your return is locked in for the duration of the CD, while savings account rates can drop at any time.

Say you open a 1-year CD today that earns 4.50%, which is the top rate in our ranking of the best nationwide CDs. That means that, no matter what happens to broader U.S. interest rates over the next year, your return of 4.50% will be guaranteed until next May.

Where Interest Rates Are Headed

The Federal Reserve opted this week to hold its benchmark interest rate steady, its third rate pause this year. But financial markets have priced in majority odds of three Fed rate cuts by year’s end, which would push savings and CD rates lower.

Daily Rankings of the Best CDs and Savings Accounts

We update these rankings every business day to give you the best deposit rates available:

Important

Note that the “top rates” quoted here are the highest nationally available rates Investopedia has identified in its daily rate research on hundreds of banks and credit unions. This is much different than the national average, which includes all banks offering a CD with that term, including many large banks that pay a pittance in interest. Thus, the national averages are always quite low, while the top rates you can unearth by shopping around are often 5, 10, or even 15 times higher.

How We Find the Best Savings and CD Rates

Every business day, Investopedia tracks the rate data of more than 200 banks and credit unions that offer CDs and savings accounts to customers nationwide and determines daily rankings of the top-paying accounts. To qualify for our lists, the institution must be federally insured (FDIC for banks, NCUA for credit unions), and the account’s minimum initial deposit must not exceed $25,000. It also cannot specify a maximum deposit amount that’s below $5,000.

Banks must be available in at least 40 states to qualify as nationally available. And while some credit unions require you to donate to a specific charity or association to become a member if you don’t meet other eligibility criteria (e.g., you don’t live in a certain area or work in a certain kind of job), we exclude credit unions whose donation requirement is $40 or more. For more about how we choose the best rates, read our full methodology.

For the ultra-wealthy, municipal bonds aren’t just about earning interest. They’re a way to lock in tax-free income, cover essential expenses, and free up the rest of their portfolio for higher-growth investments.

But even though muni bonds may offer stable income, they aren’t a perfect fit for every retiree, and they come with risks that are easy to overlook.

Key Takeaways

Municipal bonds offer steady, often tax-free income, but can come with hidden risks like liquidity issues and sometimes even unexpected taxes.

Wealthy investors often use muni bonds to cover basic living expenses while investing aggressively elsewhere to build more wealth.

Municipal bonds are best seen as one tool among many—not a complete retirement plan on their own.

Why the Wealthy Turn to Municipal Bonds

One major reason municipal bonds are popular with wealthy retirees? Taxes. “Municipal bonds can provide stable, high-quality, tax-free income,” says Noah Damsky, founder of California-based Marina Wealth Advisors, noting that they’re federally tax-free, but only occasionally state tax-free.

For example, munis may be exempt from state and local taxes if you live in the state where the bond is issued.

Reducing taxable income can make a huge difference for those in higher brackets, making munis a smart way to protect wealth without giving more away to taxes.

Plus, the relatively stable nature of many muni bonds—especially general obligation bonds backed by a government taxing authority (instead of revenue from a given project)—makes them an attractive way to fund day-to-day living expenses in retirement.

Risks and Common Pitfalls to Avoid

Despite their reputation for safety, municipal bonds aren’t foolproof. “While they’re often high quality, they’re not without risk,” Damsky cautions. “They can carry a substantial amount of interest rate risk and some credit risk.”

Liquidity is another concern many investors miss. “They can be hard to sell at a good price in big blocks, especially if the market is stressed,” Damsky says.

What’s more, buying the wrong type of muni can even trigger an unexpected tax bill—a surprise many retirees aren’t prepared for.

Before buying municipal bonds, find out if they are subject to the alternative minimum tax (AMT).

Why Home-State Bonds Aren’t Always Best

Many high-net-worth investors buy municipal bonds issued only in their home state to avoid paying state income taxes on interest earned, noted Damsky.

But concentrating too heavily can backfire. “While these bonds can be high quality, concentration in one particular state is not optimal,” he said.

Economic or political problems in one state could hit your portfolio harder than you expect. Diversification still matters—even for bonds that seem safe.

How the Ultra-Wealthy Structure Their Portfolios

For the ultra-rich, muni bonds aren’t the whole game plan. They’re often part of a bigger strategy to create a growth and income portfolio that relies on assets like alternatives too.

“I find that the ultra-wealthy like to barbell their portfolios,” Damsky explains. “They want to have their safe money in high-quality fixed income, and have their assets beyond living expenses in high-growth investments such as private equity, private infrastructure, and venture capital.”

Once they feel confident that they have secured their lifestyle with conservative investments, they turn to high-growth investments to continue to build generational wealth, he adds.

This approach effectively gives them a stable income while they pursue long-term growth.

When Munis Might Not Make Sense

If you’re trying to build wealth aggressively in retirement—not just to preserve it—relying heavily on munis might not be the best move.

“Municipal bonds can be great for sustaining existing wealth, but they are unlikely to compound wealth over the long term,” Damsky says.

Munis can be a powerful investment tool—but like any tool, they’re only right when they fit the job you’re trying to accomplish.

The Bottom Line

The ultra-wealthy use municipal bonds to create a reliable foundation of generally tax-free income, covering their essential needs while investing boldly elsewhere.

But muni bonds aren’t risk-free, and they’re not a one-size-fits-all investing solution. Understanding how they work and when they don’t can help you build a retirement plan that fits your goals.

Editor’s Note: On Wednesday, the Federal Open Market Committee (FOMC) chose to keep interest rates steady. I’m personally perplexed by this, since the latest inflation data shows it’s cooling down.

But my colleague, Luke Lango, sees a summer rally approaching – and he’s built an easy-to-use quant tool that you can use to profit. Every month, he’ll tell you what stocks to buy and sell based on a number of factors, including growing revenue, trending upward and gaining analysts’ attention. As a numbers guy, this is something I can get behind.

The tool is called Auspex, and you can learn more about it by clicking here.

Now, I’ll let Luke explain more about the summer rally that is fast approaching…

********************

Everyone was expecting fireworks on Wednesday afternoon…

Here’s what I said on Wednesday, before the FOMC rate decision announcement and Fed Chair Jerome Powell’s press conference, in the Daily Notes I send my paid-up members …

Powell’s press conference will provide some much-needed clarity as to what the Fed will do in June. He will either sound dovish and open the door for a rate cut – which will send stocks soaring higher. Or he will sound hawkish and sound hesitant on cutting rates – which will send stocks plunging lower.

But instead, Powell and the FOMC were… nothing but damp sparklers.

They kept their benchmark rate unchanged, at a target of 4.25% to 4.5%. That was as expected. The fireworks were supposed to come from the Fed’s statement and Powell’s press conference.

However, Powell said the same thing he’s been saying for months.

“We don’t think we need to be in a hurry,” he said with regard to the potential for cutting rates. He said that there are cases where it would be appropriate to cut… or to stand pat.

The stock market’s response was damp as well. All three major indices ended the day less than a percentage point up from where they started.

No “soaring” or “plunging.”

And while that may be ho-hum news for set-it-and-forget-it index investors, it’s great news for self-directed investors.

So, let’s do a few things today…

Let’s review how we got here… and why I think we’re headed into a summer rally.

Plus, I’ll tell you why this will remain a stock picker’s market despite that rally.

Also, let’s take a peek at the quant tool my team and I built to help us find the best stocks in the market. It works in volatile times like these… and it will work even better once we get past them.

Plus, I’ll reveal one stock my tool and I picked that was a winner for us last month… and that we picked again this month.

This underappreciated “space economy” play is already blasting off and outperforming the market this month as well…

The Building Summer Rally

Stocks just endured one of the fastest and most violent crashes in modern history.

In early April, stocks plummeted 10% in just two days.

As a matter of fact, until last week, stocks were tracking for their third-worst year on record after dropping more than 12% in the first 74 trading days…

But then came the biggest comeback rally in the past 100 years.

Signs that the global trade war is rapidly deescalating blew strong winds into Wall Street’s sails – sparking a historic rally. And, just as fast as they crashed, stocks staged an epic rebound.

And, I believe, momentum is building.

Let’s start with May, when we expect the “trade dam” to break.

The pressure that’s been building since “Liberation Day” is finally forcing a breakthrough on the trade front.

Over the past week, multiple White House officials have suggested that several trade deals are nearly complete – especially with key allies. We just heard about one with the United Kingdom Thursday morning, in fact (that lit off some fireworks).

We expect more of those deals to be announced in May.

They’ll do more than just ease tariffs. They’ll slam the brakes on inflation fears, cool the geopolitical heat, and give the Fed the economic clarity it’s been waiting for.

Then we’ll move into June, where two catalysts will converge – and ignite a major market rally.

First, we expect a terrible May jobs report. That’s good news.

Weak jobs data will show the true employment cost of the “Liberation Day” tariff blitz, which began just after the last payrolls survey.

This will give the Fed every reason it needs to pull the trigger on its first rate cut of 2025 at the June FOMC meeting… or at least provide the sort of post-meeting fireworks we were looking for on Wednesday.

But that’s not all.

As trade deals are signed, pressure will mount on the U.S. and China to come to terms. We believe the nations will announce a framework deal, which would serve as the clearest sign yet that the trade war is winding down.

Then in July, we will get the final piece of the puzzle: taxcuts.

We expect Congress to finalize a massive tax reform bill extending – and potentially expanding –the 2017 tax cuts. By then, lawmakers will have the cover to push this bill through.

These positive catalysts will lead us into the 2Q earnings season, which kicks off in mid-July. Those reports should reflect easing cost pressures, improved demand visibility, and a surge in forward confidence. As such, we expect strong earnings, better guidance, and reaccelerating growth.

But make no mistake…

The Stock Picker’s Top May Pick

This isn’t a “buy everything and hope for the best” market.

Volatility is the new norm. We’re living in the Age of Chaos

Traditional buy-and-hold strategies don’t work like they used to.

And so, my team and I have developed what we believe is the ultimate stock-picking engine — a quantitative, machine-driven screener that helps you get in, get out, and get paid month after month in this Age of Chaos.

It scans the market for the rarest type of opportunity – stocks that are simultaneously:

Growing earnings, revenues, and margins.

Trending up across short- and long-term technicals.

Getting attention from both analysts and traders.

These are the strongest stocks in the entire market at any given moment.

Then my team and I make the final call on which of those stocks we recommend to our subscribers.

And we’ve stress-tested it.

Over the past five years, it could have returned 1,054% — outpacing the S&P 500 by more than 10X. Even in rough stretches, it’s been able to sidestep crashes and capitalize on rebounds. In 2024, from July through December, while the S&P barely moved, it could have delivered a 24.3% return.

This model doesn’t require you to perform hours of research or constant monitoring. Just 30 minutes a month is enough to follow its signals.

In April, one of the most volatile months in stock market history, the S&P 500 dipped into bear market territory and then clawed its way back out to a just under 1% loss.

At the same time, one of this tool’s picks was Howmet Aerospace Inc. (HWM). In April, it took off for a 13.4% gain.

Our proprietary stock screener picked this aerospace and defense component specialist again earlier this month… and we agreed. So far in May, HWM shares are up 6.2% (and the top performer in our portfolio). Meanwhile, the S&P is up less than 2%.

We took this tool out of the “lab” and started using it live in June 2024. Since then, we’ve put it to the test in 10 monthly portfolios.

And with results like I just showed you with Howmet, it’s no surprise that this quant screener has, in six of those months, handily beat the market… and tied it once.

Bill Gates, worth over $100 billion, plans to leave his three children less than 1% of his vast fortune. While that still amounts to millions per child, it’s a surprisingly small fraction of what the Microsoft Corporation (MSFT) cofounder could give.

Gates’ explanation is straightforward: “It wouldn’t be a favor to them.” Instead of creating a “dynasty,” Gates says he wants the younger Gates—Jennifer, Rory, and Phoebe—to forge their own paths. We’ll get into his reasoning, along with where the rest of his wealth will go, below.

Key Takeaways

Gates’ three children will inherit less than 1% of his estimated $100 billion-plus fortune, which still translates to about a billion dollars.

Gates says that providing his children with a massive inheritance could undermine their ability to achieve their own success and develop their own identities.

How Much Is Bill Gates Worth?

Gates amassed his fortune primarily through Microsoft, the software company he co-founded with Paul Allen in 1975. Microsoft rapidly became the world’s largest software maker, helping to launch the personal computing industry. Gates became the world’s youngest self-made billionaire at age 32 in 1987, following Microsoft’s initial public offering and the explosive growth of its Windows operating system. Gates hasn’t been at Microsoft since 2000, when he stepped down from its board.

As of April 2025, Gates’ net worth is estimated to be $107.7 billion, making him the 13th richest person in the world. Gates has diversified his portfolio through Cascade Investment, his private holding company. Cascade manages stakes in dozens of public and private companies, including Canadian National Railway, Deere & Co., Ecolab, and real estate and energy assets.

The Philosophy Behind Limited Inheritance

In a 2025 interview on the “Figuring Out” podcast with Raj Shamani, Gates made his reasoning for leaving choice of how much to leave his children clear: “My kids got a great upbringing, education, but less than 1% of the total wealth because I decided it wouldn’t be a favor to them. It’s not a dynasty. I’m not asking them to run Microsoft.”

Gates said he’d like to leave them the freedom to forge their own paths. “I want to give them a chance to have their own earnings and success, be significant and not overshadowed by the incredible luck and good fortune I had,” he said.

Fast Fact

Asked about his legacy, Gates didn’t mention Microsoft or any of his business ventures. “Ideally, [those speaking of him after his death would] say that, wow, there were these diseases around, polio and malaria and malnutrition, and now we don’t have to think about that, partly because he championed putting more great thinking and resources into ending those problems.”

Where the Rest Will Go: The Gates Foundation

The vast majority of Gates’ wealth is directed toward the Gates Foundation (formerly the Bill & Melinda Gates Foundation). The foundation held $75.2 billion in its endowment as of December 2023 (the most recent public figures).

Established in 2000, the foundation focuses primarily on global health, education, and poverty reduction initiatives. The foundation has donated billions to combat diseases like malaria, HIV/AIDS, and polio.

Fast Fact

A longtime friend of Gates, Warren Buffett is a major funder of the Gates Foundation, having given over $39 billion since 2006.

Bottom Line

Bill Gates says he’s leaving less than 1% of his fortune to his children because it would do them more harm than good. But he also says he wants to prioritize the global impact his money can have for the causes that are his foundation’s focus. “The highest calling for these resources is to go back to the neediest through the foundation,” he said.

A wedding is meant to be a special, joyous occasion. However, the financial planning required for such a momentous day can feel a little less magical. According to a wedding study by The Knot, the national average cost of a wedding in 2025 is $33,000.

Daunting as it may seem, thoughtful budgeting and planning can ease the financial stress of wedding planning.

Key Takeaways

The average cost of a wedding in 2025 is $33,000

Set a total budget early and work backward to guide every spending decision.

Look for major savings opportunities like off-season dates or free venues from family or friends.

Prioritize what matters most to you—like food or photography—and allocate extra funds there.

It’s common knowledge that weddings have become expensive galas. The fact that the average age of first marriages continues to climb might have something to do with that financial investment. While the expectation of a lavish event is hard to escape, there are still ways to host a successful wedding without breaking the bank.

Note

The average age for a woman to get married has increased from about age 24 to age 28 from 1990 to 2024.

What I’m Telling My Clients

Just like with buying a house, a savings plan should be in place before anyone starts planning a wedding. Even with cutting corners and reducing costs, spending upwards of $10,000 is not hard.

In most cases, it’s good to begin with a total budget and work backward. For those who work with a wedding planner, presenting a spending cap will give that person a blueprint for piecing together your ceremony or reception. If the total is $20,000 and the dream venue costs $15,000, you know that everything else needs to be found via bargain shopping or the venue has to be reconsidered.

Finding ways to save is often the secret to a successful wedding. I encourage my clients to consider the following:

Search for an affordable venue owned by a family or a friend.

Set aside extra money for the most important things to you, such as catering, wedding attire, or photography.

Check venue prices during the off-season and try to negotiate the cost if you’re looking at a date that’s atypical for weddings. Cheaper months tend to be December and January.

Tip

According to The Knot Real Weddings Study, only 2% of weddings last year took place in January.

The Bottom Line

If you want a semi-traditional wedding, you have to plan on spending a little money. As long as you save and track down every available bargain, you can set a sensible budget and stick to it. The average cost of a wedding might be high, but you can find ways to manage it financially and still have the day you always dreamed of.

Editor’s note: “How to Build Wealth in a Volatile Stock Market” was previously published in March 2025 with the title, “Beyond the Ups and Downs: Building Wealth in a Volatile Stock Market.” It has since been updated to include the most relevant information available.

The stock market has been on quite the roller coaster ride since Donald Trump was inaugurated as the 47th President of the United States.

For about a month, stocks were flat. But it turns out that that was the calm before the storm.

With the threat of hefty tariffs looming large, investors feared that President Trump would ignite a global trade war and began selling stocks in droves. From mid-February to mid-March, the S&P 500 dropped 10% in 20 days.

And, of course, upon the rollout of his “Liberation Day” tariffs, Trump did indeed start a global trade war on April 2. This sparked a 10% market crash in just two days – its fifth-worst two-day crash ever.

But just as fast as stocks crashed, they recovered.

When Trump issued a 90-day pause on tariffs just one week after they were announced, the S&P rallied 9.5% in a single day. Then, stocks rallied 13% in 17 days – including the market’s best nine-day win streak in 100 years – as Trump issued exemption after exemption on various tariffs.

This has been arguably the most volatile and violent stock market ever. And given that Trump has been the trigger – and that he will be in the White House for the next four years – investors are naturally asking themselves:

Is this intense volatility Wall Street’s ‘new normal’?

A Bumpy Ride Higher: Why We Expect Stock Market Uncertainty to Continue

Don’t get me wrong. I think stocks are going higher over the next few years.

We’re somewhere in the middle of the AI Boom. Tech booms like these tend to last five to six years or longer. Just look at the Dot Com Boom, which started in 1995 and lasted through 1999 – five years of strong gains. The Nasdaq Composite rose about 582% during that time, while the S&P nearly tripled.

This AI Boom started in 2023. I think we have another two to three years of exceptional growth left in AI stocks. And that growth should drive the whole market higher.

However… I don’t think it’ll be a smooth ride higher…

Largely because of U.S. President Donald Trump, who promises to change a lot of things.

He wants to renegotiate trade deals and restructure global trade, rethink America’s global military presence, and cut federal spending. He wants to reduce taxes, expand America’s borders, and reshore manufacturing activity, among other things.

Clearly, he aims to change a lot.

Now, I won’t offer an argument as to whether these proposed changes are good, bad, or neutral.

But I will state the obvious: It’s a lot of change. And change is uncomfortable – especially for investors…

Because change equals uncertainty. That doesn’t mean this policy shakeup won’t push stocks higher in the long term. It may.

It simply means that, along the way, stocks will continue to be volatile – just like they’ve been over the past few months.

Stock Market Volatility by the Numbers: Record-Breaking Swings Under Trump

Since Trump was inaugurated earlier this year, we’ve seen:

One of the fastest 10% drops

Following the announcement of the “Liberation Day” tariffs on April 2, the S&P sharply declined, dropping over 12.1% in the subsequent four sessions.

One of the worst two-day crashes

On April 3-4, the market suffered a 10.5% setback, marking the fourth-worst two-day stretch since 1950.

One of the best single-day rallies

Following President Trump’s announcement of a 90-day pause on recently implemented tariffs, the S&P surged 9.5% on April 9, marking its strongest one-day performance since October 2008.

One of the best win streaks

On May 2, the S&P locked in its ninth straight day of gains – the longest winning streak in more than 20 years – rising roughly 10% over that stretch

One of the highest readings for the volatility index

The CBOE Volatility Index (VIX), often referred to as the market’s “fear gauge,” nearly doubled over six months, reaching a reading of 27.86.

This has been a three-month stretch for the record books.

If you think things will “mellow out” over the next 45 months, we think you’re sadly mistaken.

The Strategy for Surviving and Thriving in Today’s Market

Clearly, Trump isn’t playing around in his second term. He means business and intends to execute his vision, regardless of the short-term pain it may cause. That means that the volatility we’ve seen so far will likely persist throughout his tenure.

If you’re a buy-and-hold investor, that might sound scary. But that’s why I think you must become more than a buy-and-hold investor…

All these huge and violent swings in the market are giving traders lots of opportunities to buy low and sell high.

Of course, short-term trading can be risky – and notoriously hard to execute correctly. But what if you had a quant-powered system to help de-risk and simplify such a daunting endeavor?

That’s exactly what we’ve worked to build.

Meet Auspex, a quantitative, machine-driven screener that helps you get in, get out, and get paid month after month in this Age of Chaos.

It scans the market for the rarest type of opportunity – stocks that are simultaneously:

Growing earnings, revenues, and margins

Trending up across short- and long-term technicals

Getting attention from both analysts and traders

These are the strongest stocks in the entire market at any given moment.

And all it takes is about 30 minutes a month to make sure your portfolio is positioned for gains. It’s very easy to execute – and potentially very profitable.

We’re confident this is the system you need to survive – and even thrive – in today’s volatile markets.

Chairman and CEO Randall Atkins sits down with Global Finance to discuss the company’s entry into the sector.

When Nasdaq-listed, Kentucky-headquartered metallurgical coal developer Ramaco Resources announced in 2023 that it discovered rare earth elements in its Wyoming coal mine—where they weren’t expected—the developer became the latest participant in the estimated $7.2 billion rare earths market. The company, which posted $11.2 million in net profit on $666.3 million in revenue in 2024, plans to begin pilot production and processing of rare earth metals later this year.

Global Finance: It sounds like Ramaco Resources had a happy accident discovering rare earth elements in its Brook Mine project in Wyoming.

Randall Atkins: It was certainly a surprise. The way that the discovery evolved is that we were doing various research with the Department of Energy’s National Energy Technology Laboratory (NETL) on carbon products that could be made from the carbon within coal.

And part of NETL’s directive, I guess it goes back to about 2017 or 2018, was that the [US] Department of Defense had tasked them to discover where rare earth and critical minerals might be able to be found in the continental US because the Defense Department is concerned about supply lines of rare earths based on China’s dominance in the space.

They had asked us for coal core samples from our mine in Wyoming and, of course, from mines in West Virginia and Virginia. They did the same for several other mining groups, certainly not us specifically.

About a year later, they came back saying, “We’ve analyzed these [samples] pretty thoroughly, and we think we have discovered that you, in your deposit in Wyoming, may have some of the highest concentrations of medium and heavy rare earths that we’ve seen anywhere outside of Western China.”

GF: Has the latest round of tariffs changed the economics of developing this site?

Atkins: Well, it certainly has in the short term and likely will in the longer term. So, since the tariffs were announced, China has imposed an embargo on selling all rare earth elements that might have potential dual civilian and military use to the US.

We have about seven rare earth elements and critical minerals at the top of our list, and five of those seven have now been banned from export by China. As part of that ban, their prices have increased because people can’t get their hands on them.

GF: Ramaco is focusing on the heavier metals that China no longer exports to the US?

Atkins: We’re focusing on the medium and heavy rare earths. I mean, I’ll give you some names: neodymium, praseodymium, dysprosium, and terbium. Those are the four primary rare earths; the primary critical minerals are gallium, germanium and scandium. Those are the seven that we have and that we’re focused on. However, we have about 11 additional rare earths. Things like cerium, gadolinium, yttrium, et cetera, that are not as valuable as the seven that I first named.

GF: Can private industry develop the necessary infrastructure to process these ores independently, or is a public-private partnership needed?

Atkins: We were involved with NETL in discovering this. We have had conversations with the [US] government about other ways that they might get involved as we go further up the development chain, either from partnering with us in some fashion financially as we develop the processing or getting involved somehow in the procurement through the Defense Department, which is trying to establish new supply lines.

GF: Does this give you pause to see if you have thrown away rare earths from other mines?

Atkins: Yeah, great point. And indeed, NETL and others have looked at various coal seams across the country, and there has been discussion about finding rare earths in coal ash from power plants or acid mine drainage, without the need to extract new coal. Of course, the short answer to your question is no, we did not find rare earth in our other deposits back in the East … nor has anybody else, in sufficient concentration in those coal seams to make it economic.

GF: Where does Ramaco fit in the mine-to-magnet supply chain?

Atkins: Think of the supply chain as a food chain: once the ore is extracted from the ground in its raw form, it’s then beneficiated and processed into a concentrate. The concentrate then has all the elements mixed together. The next step is to separate the rare earth from the concentrate to make oxides, which are used to make metals.

The long answer is “Yes.” We will look at the possibility of taking this from mine to magnets because of the size of the overall deposit. We could also potentially go from mine to semiconductors because we could make semiconductor wafers. In addition to the rare earths, we have three critical minerals, which are now banned from exporting by China, gallium, germanium, and scandium, that can be used in the semiconductor process. So, given the size of what we’ve got over some time, certainly not on day one, we will try to take it as far up the value chain as we can.

GF: How long will it take to develop the necessary processing capabilities?

Atkins: We have been working on this with the Fluor Corporation for about a year and a half to identify the appropriate flow sheet and the refining models that would be used. And indeed, they’re in the process of designing the pilot plant.

So, what we will do from a development standpoint is we’ll start large-scale mining in June, and the larger material will then be used in a pilot plant, which we will start in August or September. Hopefully, we’ll have the pilot facility start the initial processing by the end of the year. That will run for a better part of a year. We plan to transition from the pilot to a full-scale commercial facility by the end of 2026. That would probably take about a year and a half to construct. So, we’re looking at probably the second half of 2028 before we would be in commercial production. Still, given the magnitude of what we would be building, that’s a reasonably quick timeframe.

The states with the highest 30-year new purchase mortgage rates Thursday were Alaska, West Virginia, Maryland, South Dakota, Maine, Mississippi, North Dakota, and Wyoming. The range of rate averages for these eight priciest states was 7.00% to 7.08%.

Every other state, plus Washington, D.C., had a Thursday 30-year rate average below 7%. The cheapest of these were New York, Pennsylvania, Florida, Georgia, Texas, North Carolina, New Hampshire, and Oregon. The eight lowest-rate states registered averages between 6.73% and 6.92%.

Mortgage rates vary by the state where they originate. Different lenders operate in different regions, and rates can be influenced by state-level variations in credit score, average loan size, and regulations. Lenders also have varying risk management strategies that influence the rates they offer.

Since rates vary widely across lenders, it’s always smart to shop around for your best mortgage option and compare rates regularly, no matter the type of home loan you seek.

Important

The rates we publish won’t compare directly with teaser rates you see advertised online since those rates are cherry-picked as the most attractive vs. the averages you see here. Teaser rates may involve paying points in advance or may be based on a hypothetical borrower with an ultra-high credit score or for a smaller-than-typical loan. The rate you ultimately secure will be based on factors like your credit score, income, and more, so it can vary from the averages you see here.

National Mortgage Rate Averages

Following a two-day drop, 30-year new purchase mortgages inched up a minor 4 basis points Thursday, to a national average of 6.95%. That’s still better than mid-April, when rates surged 44 basis points in a week to average 7.14%—the most expensive level since May 2024.

In March, however, 30-year rates sank to 6.50%, their cheapest average of 2025. And in September, 30-year rates plunged to a two-year low of 5.89%.

Calculate monthly payments for different loan scenarios with our Mortgage Calculator.

What Causes Mortgage Rates to Rise or Fall?

Mortgage rates are determined by a complex interaction of macroeconomic and industry factors, such as:

The level and direction of the bond market, especially 10-year Treasury yields

The Federal Reserve’s current monetary policy, especially as it relates to bond buying and funding government-backed mortgages

Competition between mortgage lenders and across loan types

Because any number of these can cause fluctuations simultaneously, it’s generally difficult to attribute any change to any one factor.

Macroeconomic factors kept the mortgage market relatively low for much of 2021. In particular, the Federal Reserve had been buying billions of dollars of bonds in response to the pandemic’s economic pressures. This bond-buying policy is a major influencer of mortgage rates.

But starting in November 2021, the Fed began tapering its bond purchases downward, making sizable monthly reductions until reaching net zero in March 2022.

Between that time and July 2023, the Fed aggressively raised the federal funds rate to fight decades-high inflation. While the fed funds rate can influence mortgage rates, it doesn’t directly do so. In fact, the fed funds rate and mortgage rates can move in opposite directions.

But given the historic speed and magnitude of the Fed’s 2022 and 2023 rate increases—raising the benchmark rate 5.25 percentage points over 16 months—even the indirect influence of the fed funds rate has resulted in a dramatic upward impact on mortgage rates over the last two years.

The Fed maintained the federal funds rate at its peak level for almost 14 months, beginning in July 2023. But in September, the central bank announced a first rate cut of 0.50 percentage points, and then followed that with quarter-point reductions in November and December.

For its third meeting of the new year, however, the Fed opted to hold rates steady—and it’s possible the central bank may not make another rate cut for months. With a total of eight rate-setting meetings scheduled per year, that means we could see multiple rate-hold announcements in 2025.

Building on a profitable and dynamic 2023, when high interest rates buoyed bank lending margins, most Western European banks had a strong 2024, ending the year with a spurt in net income and revenue growth. Many increased their focus on sustainable finance (with green bonds as a major growth area), diversified their revenue streams, and invested in new banking technology—modernizing existing apps and exploring new possibilities.

Healthy profitability was particularly notable among larger banks with an extensive branch network and strong franchises, and among banks in Southern and Southeastern Europe with large shares of the local market. In addition, banks benefited from strong investor sentiment. According to global consultancy EY, between the fourth quarter of 2023 and the fourth quarter of 2024, European bank shares rose 18%, “outperforming US banks and broader European indices by 10 percentage points.”

EY pointed out that the strong underlying position of most European banks earlier in the year enabled them to face a changing outlook toward year-end. There was a strong uptick in geopolitical uncertainty and market volatility, helping to bolster trading revenues, which were up across the board in Western Europe. Interest rates fell in some cases, and interest rates will continue to fall into 2025.

Wealth management and investment banking were growth areas, according to Nigel Moden, banking and capital markets lead at EY. “Investment banking revenues at [European banks] reached their highest levels since 2009, driven by broad-based strength across fee-generating activities and trading operations. M&A and IPO fees increased by 32% compared to 2023, although they remain below their 10-year averages,” he posted on EY’s website.

At the end of 2024, the European Central Bank (ECB) published its annual Supervisory Review and Evaluation Process, with the authors concluding that the banks of the euro area—into which most of this year’s winners fall—remained resilient in 2024. “On average, banks maintained solid capital and liquidity positions, well above regulatory requirements,” they conclude. “The aggregate Common Equity Tier 1 (CET1) ratio stood at 15.8% in mid-2024, which is a slight improvement compared with the previous year. The leverage ratio increased slightly to 5.8%. Higher interest rates continued to sustain banks’ profitability.”

In a few notes of warning, they add that “concerns around banks’ governance, risk management—including climate and nature-related risks—and operational resilience persist and require swift remediation due to the uncertain risk environment.”

Regional Winner

Gonzalo Gortazar, CEO, CaixaBank

Best Bank in Western Europe | CAIXABANK

CaixaBank has repeated its win of the Best Bank in Western Europe award and Best Bank in its home country, Spain. The country’s third-largest bank, with assets of €631 billion (about $657 billion), has a broad international representation; but its focus continues to be domestic. The bank holds impressive positions in key consumer segments, including 23.4% of consumer lending, almost 25% of consumer deposits, 23.7% of investment funds, and 34.3% of pension plans. Given Spain’s strong economic performance, this domestic emphasis has helped play into profits—last year, these were nearly €5.8 billion, up 20.2% on 2023’s more than €4.8 billion—while gross income was almost €15.9 billion, up 11.5% from 2023. Net interest income in 2024 was up almost 10% at €11.1 billion, and return on equity (ROE) reached 15.4% from 13.2% in 2023. In December, Fitch Ratings upgraded the bank to A-, citing Spain’s improved operating environment and the bank’s improved profitability and asset quality.

CaixaBank has finished its integration of the Spanish stateowned Bankia, with which it merged in 2021. Related synergies have helped CaixaBank reduce costs relative to income: In 2024, the bank’s cost-income ratio stood at 38.5% against 2023’s 40.9%. Asset quality improved, with the nonperforming loan ratio in 2024 standing at 2.6%, below the target of 3% and down from 2023’s 2.7%.

Spain enjoyed some of the fastest economic growth in the eurozone in 2024, a standout year for the bank’s wealth management business. Revenues totaled €1.8 billion, up 12.1%, and wealth management balances rose strongly by 11.7% to €263.3 billion. Net inflows to mutual funds, savings insurance, and pension plans continued to grow strongly. As a result, CaixaBank extended its market-share leadership in wealth management, claiming 29.5% of the market and widening the gap with its competitors.

Between 2021 and the end of 2024, CaixaBank mobilized nearly €86.8 billion in sustainable finance, far exceeding its original target of €64 billion. The bank continues to press forward with ambitious sustainable banking targets, mobilizing nearly €36 billion in 2024 alone.

Rating agencies have recognized the strength and versatility of CaixaBank’s business model. Toward the end of 2024, Fitch and S&P each upgraded the bank’s credit ratings, citing the bank’s sound funding and liquidity. Fitch highlights CaixaBank’s “diversified business model [which] underpins its resilience through economic cycles” and its “risk control framework and limits [which] are comprehensive, sound and commensurate with its business model.” Fitch also praises the bank’s “sound and resilient profitability,” noting that it will further benefit from “higher business volumes and strong income generation from wealth management and insurance.”

Country, Territory and District Winners

Andorra | CREAND CREDIT ANDORRA

Returning for the fifth time in a row as the Best Bank in Andorra, Credit Andorra has fully integrated Vall Banc, the acquisition of which was completed three years ago. The bank is now widely known as Creand Credit Andorra. With over €51.7 billion under management, profit increased by over 60% to nearly €71.3 million in 2024.

Austria | UNICREDIT BANK AUSTRIA

Net profits for this year’s Austrian winner, UniCredit Bank Austria, were up 14.2% over 2024, reaching approximately €1.3 billion. This seals a very satisfactory year for the institution, whose total assets now stand at around €105.3 billion. In the year in which Bank Austria celebrated 20 years as part of the UniCredit group, the bank consolidated its leading position in corporate banking, wealth management, and private banking. With an extensive network of over 104 branches across Austria, it has become the national leader in mobile banking, with usage now at 63%, well above the market average of 55%. Already, 21% of Bank Austria customers see themselves as digital-only users, compared to the market average of 15%.

Belgium | BNP PARIBAS FORTIS

BNP Paribas Fortis has earned its award as the Best Bank in Belgium after an impressive and rewarding year. This continued into early 2025 when the bank released the latest version its Easy Banking App. It enables users to look at their financial activities in real time and load their activities with other banking groups (like ING, Belfius, or KBC) through the app. The bank worked with Swedish fintech company Tink to develop the app.

Cyprus | BANK OF CYPRUS

With assets of just under €26 billion, the Bank of Cyprus—the primary beneficiary of Cyprus’ 2012-14 financial crisis—had another great year, with preliminary results for 2024 suggesting a 4% increase in after-tax profits to a record €508 million. The Bank of Cyprus is a key financial actor on the island: The bank now has 38% of deposits and 43% of loans, while its digital sales platform Genius enables seamless connection of its customers and businesses with suppliers and other companies. In a strategic repositioning, the Bank of Cyprus—whose market capitalization is now €2.3 billion—has moved its listing from the London to the Athens Stock Exchange.

Denmark | DANSKE BANK

Danske Bank—our winner in Denmark—consolidated its lead over domestic rivals, reporting total assets of over 3.7 trillion Danish kroner (about $518 billion) by the end of 2024 with solid results, building on 2023’s recovery. For 2024, the bank reported net profits of 23.6 billion kroner, up 11.1%; and total income of 56.4 billion kroner, up 7.8%. ROE in 2024 was 13.4% against 2023’s 12.7%.

Finland | NORDEA

The Best Bank in Finland, Nordea, which has benefitted from the country’s membership in the European Single Market, further consolidated its dominance of the sector with total assets worth €623.4 billion, up €39 billion in 2023, and a nearly 62.7% market share (based on total assets). The bank’s 2024 operating profit was over €6.5 billion, up 2.5% year on year.

France | BNP PARIBAS

BNP Paribas won this year’s award as Best Bank in France, despite sluggish growth in its commercial and retail operations in 2024, reflecting the broader economic picture in France. However, the division rebounded in the final quarter, recording growth of 4.7%. A revival in investment banking helped the bank to lift its profits by more than 15% in the fourth quarter. The bank, France’s largest lender, said it would launch a new strategic plan to boost the profitability of its domestic business, increasing the profitability of commercial and personal banking in France to the level of the wider group. Growth at BNP is expected to be boosted by the integration of Axa Investment Managers, acquired from French insurer Axa last year in a €5.1 billion deal.

Germany | COMMERZBANK

For our German winner, Commerzbank, Germany’s thirdlargest bank, last year was big, with assets of €555 billion in 2024. Its net profits hit a record €2.7 billion, a rise of 20% over 2023 and an increase of more than 50% from 2022. The bank aims to increase its net result to €4.2 billion by 2028. With its upgraded “Momentum” strategy, Commerzbank has set significantly more-ambitious targets than before, focusing strongly on small businesses and on private customers and wealth management. The return on tangible equity (ROTE) is expected to improve to 15% by 2028. This means that the bank will earn significantly more than its cost of capital and be a well-established player among the successful European banks.

The bank entered 2025 fighting a hostile bid from our Italian winner, UniCredit. The latter received ECB approval in March to up its stake in the German bank to 29.9%. However, UniCredit has indicated it will probably wait until 2026 before announcing its future strategy.

Greece | EUROBANK

The winner as Best Bank in Greece, Eurobank, has earned the title after an impressive 2024. With a vast international presence in Bulgaria, the UK, Luxemburg, and Cyprus, Eurobank Holdings had assets of nearly €100 billion, as of September 2024. The bank reported net earnings of €1.45 billion in 2024, up 27% on 2023. In early 2025 it completed the purchase of an additional 37.5% of Hellenic Bank in Cyprus, bringing its total holding close to 100%. The entity is to be merged with Eurobank Cyprus to compete against Bank of Cyprus, the other main bank on the island.

Eurobank argues that its business success reflects its wide range of activities, including “egg” (enter, grow, go), a business startup plan aimed at small and midsize enterprises and now the second-largest such scheme in Eastern Europe. Another bank initiative is Trade Corridors, a “phygital” business network aimed at helping Greek businesses locate and do business with potential global partners.

Iceland| LANDSBANKINN

Iceland’s largest bank, Landsbankinn returns as the Best Bank in Iceland for a second consecutive year. Holding some 40% of the domestic retail market, profit in 2024 was 37.5 billion Icelandic krónur (about $271 million) after taxes, up from 33.2 billion krónur in 2023. ROE in 2024 was 12.1%, lending was up 10.8%, and customer deposits increased by 17.2%. The Smart Savings app saw customer usage rise by almost 40% last year.

Ireland | AIB

Allied Irish Bank (AIB) has earned the title of Best Bank in Ireland for the second year in a row. It delivered a strong 2024 performance with a profit after tax of €2.35 billion, a 26.7% ROTE, and total 2024 distributions to shareholders of €2.6 billion. Buoyed by a vibrant economy, new lending grew by 17% to €14.5 billion, while the customer base reached its highest level at 3.35 million.

Italy | UNICREDIT

Our winner in Italy, UniCredit had another impressive year, with full-year net profit up 2% to reach €9.7 billion. Net revenue grew 4% to €24.2 billion, up 4% fiscal year over fiscal year, driven by fees at €8.1 billion, up 8% on the year, reflecting strong client activity and broad product offering to the bank’s more than 15 million customers across Europe. The bank is firmly committed to sustainability and other environmental, social, and governance principles. UniCredit seeks to boost digitalization across the group. Fitch upgraded the bank to BBB+ in October 2024.

The record-breaking performance marked the 16th consecutive quarter of sustainable, profitable growth. This reflects the potential unlocked during the initial phase of the UniCredit Unlocked transformation plan. UniCredit became a unique pan-European model increasingly active in Central and Eastern Europe and in Germany. Diversified fees and high-quality net revenue growth, high organic capital generation, strong ROTE, and generous total distributions have all set the path for UniCredit to enter its next acceleration phase from 2025 to 2027. As 2025 got underway, UniCredit Italy is reported to have bought a stake in insurance giant Generali Group and to be separately trying to take over Milan lender Banco BPM, in which both groups also own a stake.

Liechtenstein | LGT

Liechtenstein’s LGT, the principality’s largest bank, owned wholly by the royal family, has had a good few years. It started 2024 with more than 58.1 billion Swiss francs (over $64 billion) in assets. To boost its asset management business in Austria, LGT is looking for acquisition opportunities in Switzerland and Germany.

Luxembourg | SPUERKEESS (BCEE)

Spuerkeess (BCEE) returns as the Best Bank in Luxembourg for the fourth consecutive year. Better known as Banque et Caisse d’Epargne de l’Etat, state owned and established in 1856, BCEE has dominated banking in the duchy for decades and currently controls around 50% of the retail banking and mortgage market. BCEE successfully issued a €500 million 6NC5 senior preferred green bond on March 12, marking a significant milestone in its capital markets strategy. The bond, which was oversubscribed 3.6 times and issued under BCEE’s newly launched Green Bond Framework, will be listed on the Luxembourg Stock Exchange.

Malta | HSBC

HSBC takes home the award for the Best Bank in Malta after a record 2023 in which pretax profits rose 141% to €133.9 million on the back of increased net interest margins and higher earnings from its insurance subsidiary. Last year, the bank posted another pretax profit increase, of 15% to €154.5 million, and ROE was slightly up at 17.5% against 17.1% in 2023. Customer deposits increased by €16.8 million to almost €6.2 billion as of December 31, 2024. Management attributes the increase in profits to growth across all revenue lines, mainly due to higher interest rates, increased customer activity, and higher insurance subsidiary results. HSBC Malta’s strong performance hasn’t gone unnoticed; takeover talks were in the air. However, government officials were said to be opposed, arguing that Malta needs more rather than less competition among its banks.

Monaco | CFM INDOSUEZ WEALTH MANAGEMENT

Monaco’s CFM Indosuez Wealth Management, owned mainly by Credit Agricole, has won the laurels as the Best Bank in Monaco. The principality’s leading commercial bank, serving two out of three businesses—unsurprisingly, given its history and location—puts wealth management center stage. However, it also launched its StartUp Connections last year, a digital platform offering simplified access to an international network of startups in Monaco, Belgium, Luxembourg, and Switzerland.

Netherlands | ING

Our Dutch winner, ING, with over 60,000 employees serving 40 million customers globally, is familiar to anyone who does business with or visits the Netherlands. Over 2024, the bank consolidated its position as market leader. Global assets reached approximately €1 trillion, but annual net profits for the year came in below market expectations at €6.4 billion. Income is expected to hold steady this year on the back of falling interest rates, according to CEO Steven van Rijswijk, who says the bank is looking for acquisitions this year to help boost overall performance.

Throughout 2024, the bank said it would increase focus on wholesale, personal, and private banking. In March 2025, ING announced that it had reached an agreement with Reggeborgh Groep on the acquisition of a 17.6% stake in Van Lanschot Kempen, a specialist wealth manager serving private, institutional, and investment banking clients, operating predominantly in the Netherlands and Belgium. With an existing 2.7% stake, ING will hold a 20.3% stake in Van Lanschot Kempen after the completion of the transaction.

ING has also reiterated its commitment to its climate goals, advising clients that it will either restrict or stop providing finance, on a case-by-case basis, to companies that fail to address their carbon footprint. This stands in sharp contrast to many other financial institutions that have loosened some climate targets.

Norway | DNB

Last year was a good year to be a banker in the Nordic region, with improvements in asset quality and overall performance driven by a broadly benign economic environment and market dominance for the key players. The Norwegian winner, DNB, had another solid year as the leading bank in Norway with a year-end market capitalization of 336 billion Norwegian kroner (about $29.7 billion), up from 328 billion kroner in 2023; and post-tax profits of 45.8 million kroner, up on 2023’s approximately 39.5 million kroner, a result reflecting Norway’s GDP growth of 2.1% last year against just 0.1% in 2023.

Portugal | BANCO SANTANDER TOTTA

The winner for Portugal, Banco Santander Totta, is the third-largest bank in the country by assets (€56 billion), with some 4.7 million customers. Its net profits for last year were up again, by 10.7% over 2023, to reach €990 million, an impressive reflection on the bank’s performance and Portugal’s ongoing economic recovery. The bank actively courts the youth market, offering work cafes, and is well ahead of competitors in its digital offerings. However, it has not forgotten seniors, launching a new health insurance product for them. Fitch gives Banco Santander Totta the Portuguese bank sector’s highest score, A.

Sweden | SWEDBANK

Swedbank, the country’s third-largest domestic bank, is the winner in Sweden on the back of solid results: After-tax profits for 2024 were up 2.2% to 34.1 billion kronor (about $3.1 billion), while total assets reached 3 trillion kronor, with 7.4 million private customers.

Switzerland | UBS

UBS returns for the fifth year in a row as the Best Bank in Switzerland and reflects another strong year—the complex takeover of Credit Suisse is now almost complete—in which it increased its local market share by 40% and became the world’s largest wealth management bank. The bank’s 2024 net profits were $5.1 billion, lower than the previous year but better than expected—an otherwise normal year but impacted by the ongoing Credit Suisse integration. UBS plans to buy back $1 billion of shares in the first half of 2025 and up to $2 billion in the second if there are no “material and immediate changes” to Swiss capital rules that the authorities are considering to require UBS to hold more capital.

UK | HSBC

On the back of impressive group results, HSBC wins the Best Bank in the UK award. The Group, which reports in dollars, posted a post-tax profit increase of $400 million over the previous year to $25 billion, and total group assets topped $3 trillion by the end of 2024. Last year saw several initiatives in the UK market. These included the launch of Flexipay, which lets consumers spread the cost of a large point-of-sale purchase at one of the bank’s merchant partners, whether or not the customer has an existing HSBC relationship; the relaunch of the bank’s fee-free Premier Account; and the debut of new benefits for its Premier World Elite credit card. HSBC UK also revealed its plans to double assets under management to £100 billion ($134 billion) by 2028.

So, it was another strong year for Western Europe’s leading banks. Most have positioned themselves well for 2025; although with rising geopolitical uncertainty, a possible tariff war and other negatives, 2025 looks to be very different from 2024. In its look ahead to 2025, Fitch in December noted that 80% of the region’s banks have a stable outlook, with just 4% on a negative outlook and 15% on a positive one. The rating agency also suggested that “business conditions for the banks will remain sound, resulting in another year of good performance” and maybe an increased prospect of consolidation.

The improving outlook is particularly pronounced in the southern countries, Greece, Portugal, and Spain, on the back of continued business growth. The Nordic region and the Benelux countries are facing a neutral outlook with continued strong profitability and resilient asset quality. Banks in Germany and Italy have a neutral outlook with “resilience amidst weak economic performance” (Germany) or “subdued credit demand” (Italy). By contrast, French banks face a deteriorating outlook amid “macro uncertainties and political risk.”

With the overall macro-outlook in early 2025 more uncertain than it has been in many years, it was perhaps unsurprising that the ECB announced in January that it would stress test some 96 eurozone banks over the year. The ECB’s priorities for the sector in 2025 include, among other things, strengthening bank resilience to macro-financial and geopolitical shocks, and ensuring banks address digital transformation and climate change in an efficient and meaningful way. In a fast-changing world, the healthiest West European banks—like banks everywhere else—will demonstrate genuine foresight and flexibility.

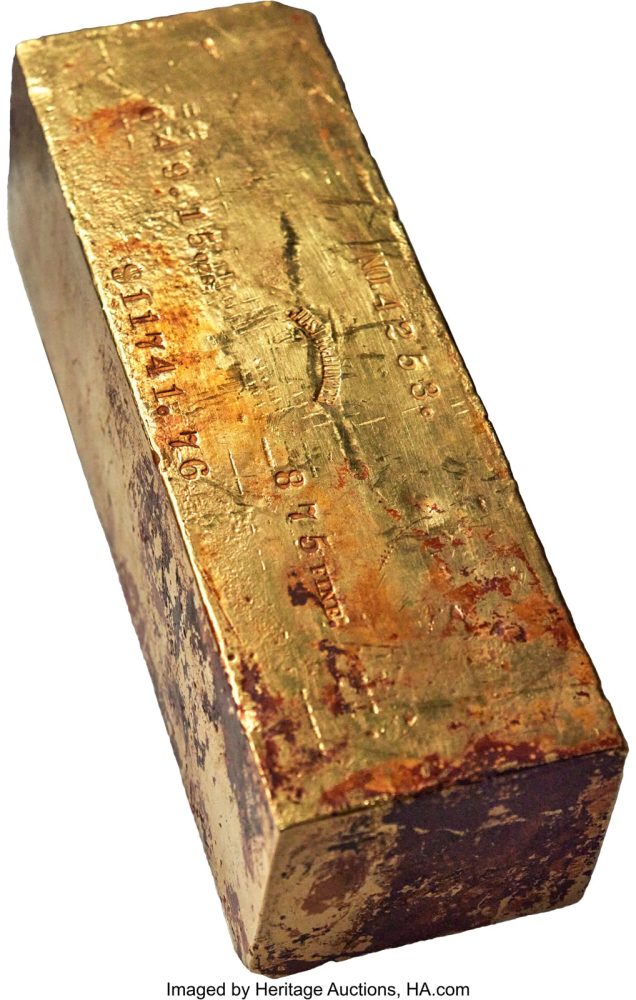

Serious collectors know a must-have treasure when they see one, and that was exactly what happened when a massive Justh & Hunter gold ingot crossed the auction block at Heritage Auctions’ April 30-May 4 CSNS US Coins Signature® Auction in which numerous new auction records were set. The last of 60 bids drove the final result for the ingot to $2.13 million to lead the total for the event to $31,691,002.

The ingot that led the U.S. Coins event, from The Marcello and Luciano Collection, is a behemoth, measuring 218 mm (nearly 8.6 inches) and weighing in 649.15 troy ounces, or just over 44.5 pounds.

“This is a magnificent result for a magnificent treasure, the second-largest ingot from the S.S. Central America that ever has been brought to auction,” says Todd Imhof, Executive Vice President at Heritage Auctions. “It is one of just 13 in the Colossal Size weight class (more than 500 ounces), and an appropriate leader for this event.”

The ingot was just one of four lots that topped $1 million, the other three coming from The Bruce S. Sherman Collection, Part II, a treasure trove assembled by Sherman, Chairman and principal owner of Major League Baseball’s Miami Marlins, that has been called “one of the most remarkable achievements in numismatics.”

The top lot from the Sherman collection was an 1835 HM-5, JD-1 Half Eagle, PR67+ Deep Cameo PCGS. CAC that is the finest of just three known examples and climbed to $1.8 million, smashing the previous auction record of $822,500. Few proof Classic Head half eagles are known, and of those, the example from the Sherman collection is believed to be finest, regardless of date. Of the 20 on Heritage’s roster, five are museum pieces, including one in the British Museum and four in the Smithsonian.

1835 HM-5, JD-1 Half Eagle, PR67+ Deep Cameo PCGS CAC

Another seven-figure record-setter was a 1792 Copper Disme, Judd-11, MS64 Red and Brown PCGS. CAC from the Sherman collection that drew 43 bids before ending at $1.5 million, surpassing the previous auction record of $1,057,500 set by Heritage in 2015. It is the finest by a wide margin of just three known examples of an outstanding rarity in the U.S. pattern series. The Mint experimented with reeded and plain edges on the copper dismes of this year, and the plain edge pieces are considerably scarcer.

1792 Copper Disme, Judd-11, MS64 Red and Brown PCGS CAC

The fourth lot to exceed $1 million was an 1803 Proof Draped Bust Dollar or Novodel, PR66 PCGS that is tied for the finest among just four known survivors and sold for $1.11 million – well above the previous auction record of $851,875 set by Heritage in 2013. Proof silver dollars from 1801-03 are known today as “novodels,” which are among the rarest and most valuable issues in the U.S. federal coinage series.

1803 Proof Dollar or Novodel, PR66

Another popular coin from the Sherman collection was an 1879 Coiled Hair Stella, Judd-1638, PR62 PGGS, a prize in such high demand that it drew 59 bids before closing at $576,000. Before it was acquired by Sherman, it was part of the famed Richmond Collection.

One of just 16 examples traced of an 1876-CC Twenty Cent Piece, MS64 reached $444,000. A landmark rarity in the U.S. silver series, the 1876-CC twenty cent piece often is mentioned in the same class as the famous 1804 dollar, 1913 Liberty Head nickel, and the 1894-S Barber dime and earned the “Duke of Carson City Coins” moniker from Rusty Goe. This example’s history, before ending up with Sherman, included stops in the collections of Louis E. Eliasberg and Eugene Gardner.

1876-CC Twenty Cent Piece, MS64

Nearly 100 bids poured in for a 1792 Half Disme, Judd-7, MS64 PCGS before it achieved $432,000. The 1792 half disme is among the most important issues in all of American coinage, was the first circulating coinage struck by the authority of the U.S. Congress, and is listed among the 100 Greatest U.S. Coins. The example in this auction has not been offered at auction in more than 20 years.

1792 Half Disme, Judd-7, MS64 PCGS

A 1794 B-1, BB-1 Silver Dollar, XF40 PCGS. CAC, the Gainsborough Specimen of America’s first silver dollar, brought a winning bid of $384,000. One of 10 lots in the auction from The Texas Republic Ranch Collection, it is a magnificent example of one of the historically significant pieces of American coinage, each personally handled by Mint Director David Rittenhouse.

1794 B-1, BB-1 Silver Dollar, XF40 PCGS CAC

A 1798 Draped Bust Small Eagle Dollar, MS62 PCGS brought $360,000. That figure surpassed the previous auction record of $216,000 for a 1798 Small Eagle, 15 Stars dollar that was set by Heritage in 2024, and also set a new auction record for any 1798 Small Eagle dollar.

1798 Draped Bust Small Eagle Dollar, MS62 PCGS

Complete results for the CSNS U.S. Coins event can be found at HA.com/1393.

This spectacular note is among the top offerings from the collection of Charlton Buckley, the former San Francisco-area businessman who pursued National Bank notes, large and small, as well as large and small size U.S. type notes, resulting in a trove of California Nationals and notes, including California Gold Bank Notes and Federal Reserve Notes.

“High-denomination notes always have exceptional appeal among collectors, and this is example is the perfect combination of collector demand and exceptional grade,” says Dustin Johnston, Senior Vice President of Numismatic at Heritage Auctions. “It has exceptional eye appeal, and when our consignor acquired it in in 2015, was one of the nicest offered $10,000s in the preceding half decade. Now, it’s a magnificent addition to a new collection.”

Also from the Buckley collection was a Fr. 2221-E $5,000 1934 Federal Reserve Note. PMG Choice Uncirculated 63 that drew a winning bid of $240,000. Prior to this event, it had appeared at auction just once before. The PMG Population Report includes 15 graded examples, with just one Fr. 2221-E graded equal and two graded higher.

A San Francisco, CA – $50 1870 Fr. 1160 The First National Gold Bank Ch. # 1741 PMG Fine 12 from the Buckley collection ended at $180,000. It is one of only seven $50 National Gold Bank Notes – six of which are from this San Francisco bank – listed in the National Currency Foundation census; one of the overall seven reported $50 National Gold Bank Note survivors is in multiple pieces and another likely off the market forever in the ANA museum, thus resulting in only five obtainable examples.

San Francisco, CA – $50 1870 Fr. 1160 The First National Gold Bank

A Fr. 2221-E $5,000 1934 Federal Reserve Note. PMG Very Fine 25 from the Buckley collection reached $144,000. Its serial number, E00000170A, is the highest among the 13 valid serial numbers listed in Track & Price. This event marked just the second time this note has been offered at auction.

Fr. 2221-E $5,000 1934 Federal Reserve Note. PMG Very Fine 25

Another collection featured in the event was the auction will include 54 lots from the Ronald R. Gustafson Collection, which produced 49 lots sold in the auction, including a Fr. 2220-A $5,000 1928 Federal Reserve Note. PMG Choice About Unc 58 that brought a winning bid of $288,000. One of just three documented Boston Series 1928 $5,000s, its popularity is due to the combination of grade and rarity. PMG has graded less than two dozen Series 1928 $5,000s, and this example is among the finest known of that small population.

Fr. 2220-A $5,000 1928 Federal Reserve Note. PMG Choice About Unc 58

Fr. 2231-F $10,000 1934 Federal Reserve Note. PMG Very Fine 30

Not all of the top results in the auction were for lots from featured collections. For example: a Fr. 187j $1,000 1880 Legal Tender PMG Very Fine 30 Net that ended at $180,000. This high-denomination rarity has a vignette of Columbus in His Study and a portrait of DeWitt Clinton, who was governor of New York during the years of 1825-28 and had earlier served three stints as the mayor of New York City. Track & Price lists 15 different serial numbers for this Friedberg number, one of which is part of an institutional collection.

Fr. 187j $1,000 1880 Legal Tender PMG Very Fine 30 Net

Fr. 2231-H $10,000 1934 Federal Reserve Note. PMG Extremely Fine 40

Fr. 2220-D $5,000 1928 Federal Reserve Note. PMG Very Fine 25

A beautiful Cincinnati, OH – $100 1875 Fr. 460 The Metropolitan National Bank Ch. # 2542 PMG About Uncirculated 55, an outstanding example of this very rare type and denomination, reached $120,000. Just one other is listed in the census with a CU grade, but that note, on a New York bank, never has appeared at public sale. Either way, the National Currency Foundation census does not list any other 1875 $100s above the 55 level, meaning this example very well could be the finest known.

Cincinnati, OH – $100 1875 Fr. 460 The Metropolitan National Bank

Complete results from the US Currency event can be found at HA.com/3598.

Victoria gold Proof “Una and the Lion” 5 Pounds 1839 PR62 Ultra Cameo

Among the most recognizable types in world numismatics, it remains an artistic masterpiece nearly two centuries after its creation.

“William Wyon is revered as one of the most accomplished and important engravers in all of British coinage,” says Cris Bierrenbach, Executive Vice President of International Numismatics at Heritage Auctions, “and this is a beautiful example of the coin that is considered his crowning achievement, one that exhibits his extraordinary technical skill and artistry. This is the kind of coin that immediately becomes a centerpiece of a collection.”

A Louis XIII gold 10 Louis d’Or 1640-A AU Details (Cleaned) NGC drew a winning bid of $264,000. This is a Draped Bust variety of this rarity, offered at Heritage for the first time, which helps to explain the immense demand for the type. As early as 1690, F. Leblanc suggested that they were fantasy pieces possibly struck for the king’s pleasure rather than for circulation. Later scholarship reversed course and posited the likelihood that these were struck for commerce, though the possibility remains that they remain fantasy pieces or trial strikes. Documents from the French National Archives confirm Jean Warin as the original engraver in 1640.

Louis XIII gold 10 Louis d’Or 1640-A AU Details (Cleaned) NGC

An Edward VIII bronze Matte Proof Pattern 1/2 Penny 1937 PR64 Brown NGC, from the Cara Collection of highly provenanced British Rarities, blew past pre-auction estimates when it climbed to $180,000 – a record for any minor of Edward VIII. This magnificent coin is just the fourth example of any Edward VIII coinage offered at Heritage in the last half decade, and is presumed to be unique, as no other Matte Proofs of this denomination have surfaced; examples even have eluded the British Museum and Royal Mint collections, in which only brilliant Proofs reside.

Edward VIII bronze Matte Proof Pattern 1/2 Penny 1937 PR64 Brown NGC

Also from the Cara Collection was an Oliver Cromwell gold Proof Pattern Broad of 20 Shillings 1656 PR63 PCGS that drew nearly two dozen bids on its way to $126,000. This coin is one of the most sought-after British gold types, not only due to its sheer rarity, but its historical implications from one of the most tumultuous eras in English history. This example is tied with three others atop the PCGS population report.

Oliver Cromwell gold Proof Pattern Broad of 20 Shillings 1656 PR63

The collection produced half of the six-figure results in the auction, a list that also included an Anne gold Pattern Guinea 1702 AU55 NGC that ended at $102,000. A treasure of English numismatics, it is the first Guinea Pattern ever struck by the Royal Mint, with fewer than five known examples. This auction marked the first time this type ever had been offered at Heritage. This type carries considerable cache, considering it was minted under the management of famed physicist and then-mint master Sir Isaac Newton.

Anne gold Pattern Guinea 1702 AU55

Other top lots from the Cara Collection included, but were not limited to:

A Victoria gold Proof 5 Pounds 1887 PR66+ Deep Cameo PCGS, the finest certified example of the most revered emission from Victoria’s legendary Golden Jubilee Proof Set, ended at $168,000. This remarkable example is so void of abrasions or other blemishes that it looks like it could have been struck yesterday.

Victoria gold Proof 5 Pounds 1887 PR66+ Deep Cameo

Other highlights in the auction included, but were not limited to:

Complete results for the World & Ancient Coins event can be found at can be found at HA.com/3123.

About Heritage Auctions

Heritage Auctions is the largest fine art and collectibles auction house founded in the United States, and the world’s largest collectibles auctioneer. Heritage maintains offices in New York, Dallas, Beverly Hills, Chicago, Palm Beach, London, Paris, Amsterdam, Brussels, Munich, Hong Kong and Tokyo.

Heritage also enjoys the highest Online traffic and dollar volume of any auction house on earth (source: SimilarWeb and Hiscox Report). The Internet’s most popular auction-house website,HA.com, has more than 1,960,000 registered bidder-members and searchable free archives of more than 7,000,000 past auction records with prices realized, descriptions and enlargeable photos.