If you’ve inherited some money—even if it isn’t a lot—congratulations! You could just go out and spend it, of course. Or you could invest it in something more meaningful to you.

Before doing anything with the money, give yourself a little time to regroup. Inheriting money—even a modest sum—can bring up emotional decisions, especially if it came from someone close to you. Taking a pause can help you make choices that align with your long-term goals.

Here are five simple steps to make a modest inheritance go the farthest.

Key Takeaways

When you inherit money, the first step is to pause and take a deep breath.

You might want to invest the money for a future goal or use it for a short-term one, such as paying down credit card debt.

Your time frame will guide your investment choices. The more distant your goal, the more risk you can take.

1. Don’t Rush

Take a moment to assess your financial picture and resist the urge to spend impulsively. A calm, thoughtful approach will help you make smarter choices.

2. Park It Someplace Safe

Rather than an everyday bank account, look for one that will at least earn you some interest. Mari Adam, a certified financial planner in Boca Raton, Fla., says a money market account at a discount brokerage firm can be ideal for that purpose. Another possibility is a high-yield savings account at an online bank. They’re both currently paying about 4%.

3. Be Aware of Any Tax Implications

Inheritances are generally tax-free to the recipient. However, as Adam points out, that can depend on how the inheritance comes to you. If it’s simply cash, you most likely don’t have to worry about taxes. If you’re the beneficiary of someone’s individual retirement account (IRA), however, you are subject to a different set of tax rules.

4. Consider Your Options

You may want to earmark the money for a future goal, such as a down payment on a home, your own or a child’s education, or your retirement. Or, you might want to put it to use right away, such as paying down any high-interest credit card debt you’ve been carrying.

If you don’t really need the money for more serious purposes, don’t hesitate to use it for something you’ve always dreamed of but could never afford—a special vacation trip, for example. “Someone felt enough of you to give you this gift,” Adam says. “They wanted you to enjoy it.”

5. Invest Accordingly

If your plan for the money is to buy a new car a year from now, you will want to invest it more conservatively than if it’s for a long-term goal, such as your retirement in 20, 30, or 40 years. In the former case, you might just leave it in the money market or high-yield savings account; in the latter case, you’ll have more options for potentially higher returns, such as a stock index mutual fund.

The Bottom Line

If you’ve inherited a little money, what you do with it next is up to you. You can spend it, save it for the time being, or invest it for the long haul. Whatever you end up doing, try to give it some thought before you act because once the money’s gone, it’s gone. And a modest inheritance can go pretty fast.

Editor’s Note:April didn’t bring the kind of market performance we’ve come to expect. Instead of historical gains, investors were met with headwinds: tariff battles, inflation concerns, and political uncertainty.

But just like the saying goes, April showers bring May flowers.

That is why I’d like to share a Market 360 article that my InvestorPlace colleague Louis Navellier shared with his reader’s last week. In it, Louis digs into the signs of life already sprouting beneath the surface.

He believes that this is a time for strategic thinking – not panic. And with the right insights, it’s possible to turn today’s uncertainty into tomorrow’s opportunity.

Take it away, Louis…

Historically, April is the second-strongest month of the year, with the S&P 500 gaining 1.7% on average in post-election years since 1950.

Unfortunately, the proverbial “April showers” drenched Wall Street and dampened investors’ moods, so April 2025 did not live up to this historical precedent.

I think it’s safe to say we all know why: Tariffs.

Now, I understand the uncertainty that many investors have felt about the tariffs. But I have been on record saying that the market’s response has been a gross overreaction.

Of course, President Trump is going to do what he does. But I have also said that if you are looking for reassurance, the person to watch during all of this is Treasury Secretary Scott Bessent.

Still, I think the negativity the financial media has flooded the airwaves with lately is responsible for much of the uncertainty. The foreign media has been particularly negative, as it is eager to blame the Trump administration for all of the problems in their respective economies which were already struggling.

So, when American investors wake up in the morning and see all of these negative headlines, it’s natural that they would feel gloomy.

However, as the old saying goes, with April showers come May flowers. And I think there will be some very beautiful flowers in the market in May, especially from my Growth Investor stocks. So, I want to talk about a few green shoots that are already emerging in the market.

Green Shoot #1: Thawing Tariff Tensions

As you know, the trade war between China and the U.S. escalated in early April.

China turned up the pressure by banning all rare earth exports to the U.S., which included rare earth magnets. This ban will hinder the electric vehicle (EV), technology, aerospace and defense industries. China also halted deliveries of Boeing Co. (BA) jets, with 10 new 737 Max jets grounded before they could be shipped to three Chinese airlines.

The Trump administration responded in kind, banning NVIDIA Corporation (NVDA) from delivering its H20 GPUs to China. The H20 chip was specifically developed for China after the Biden administration placed restrictions on AI chip shipments.

However, Treasury Secretary Scott Bessent recently told attendees at a closed-door investor summit that the tariff standoff with China cannot be sustained by both sides. He noted that the world’s two largest economies will have to find ways to de-escalate tensions – and this de-escalation will come soon.

Well, during a press conference, President Trump noted that the final tariffs on China will be a lot lower than current levels. He even added that if China and the U.S. cannot come to an agreement on tariffs, he may still lower key tariffs. Trump predicted that the final tariff on China would not be “anywhere near” the 145% level, and he added that “we’re going to be very nice” in negotiations.

I should also add that the U.K., the European Union (EU) and about 130 countries are all negotiating new trade agreements with the U.S. – and that should remove most trade barriers.

So, freer trade should be the end result.

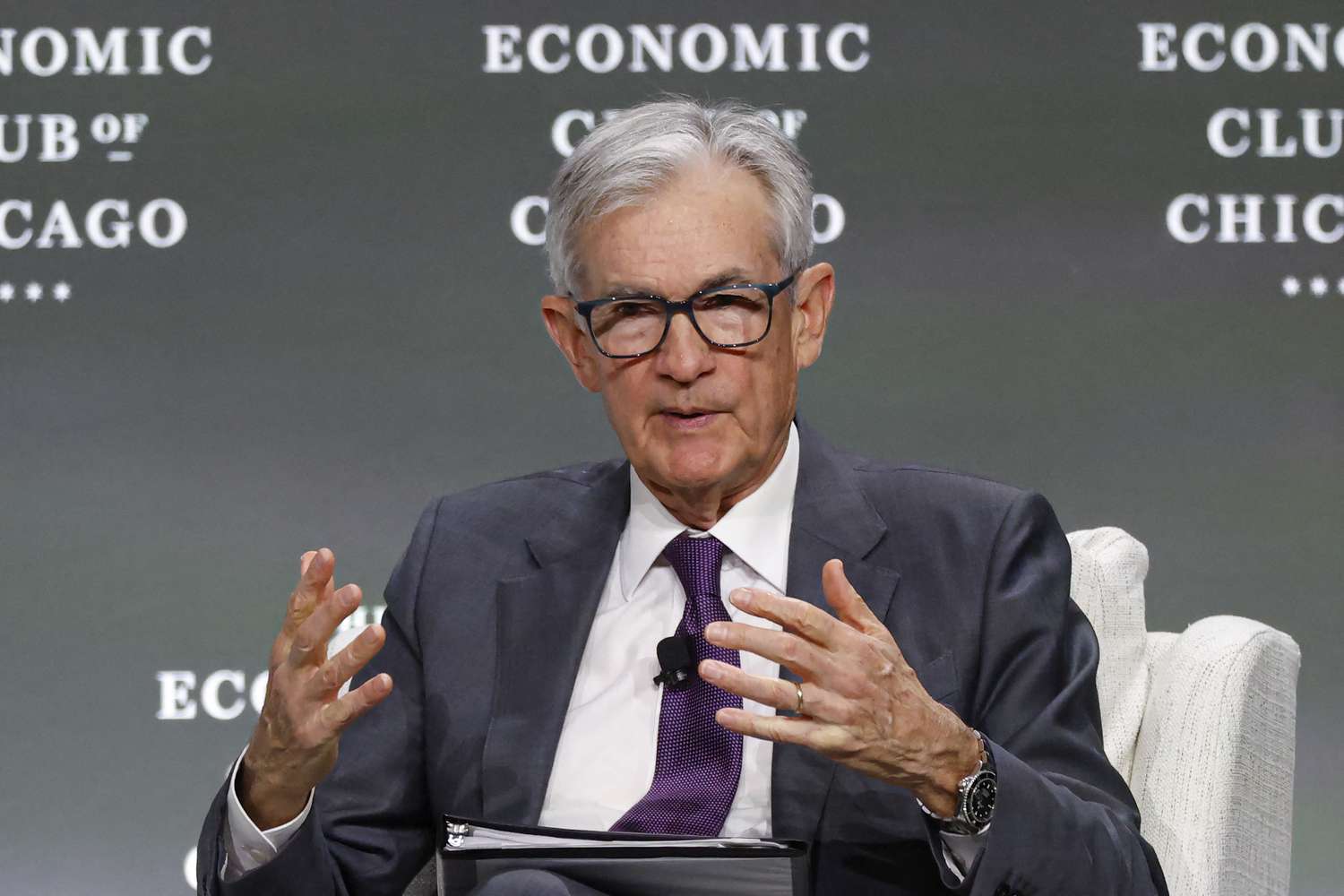

Green Shoot #2: Powell’s Job Is Secure… for now

Given that the Federal Reserve has sat on its hands this year, President Trump’s frustration was on display recently – and that ignited fears that Fed Chair Jerome Powell’s job was in jeopardy.

Powell appeared before the Economic Club of Chicago, where he said that there is a “strong likelihood” that Americans will face higher prices, and the U.S. economy will see higher unemployment due to tariffs. He continued saying that this environment would create a “challenging scenario” for the Fed because any adjustments to interest rates to address inflationary pressures could worsen unemployment and vice versa.

Powell concluded, “It’s a difficult place for a central bank to be, in terms of what to do.”

Clearly, the Fed and Powell remain concerned about inflation. But the reality is consumer and wholesale inflation both declined in March. Also, deflation has actually arrived in the wake of the lowest crude oil prices in four years.

So, the Fed, Powell and even our allies are needlessly worried about inflation.

It’s clear that Powell is not an economist, and that’s why President Trump responded on Truth Social, stating that “Powell’s termination can’t come quickly enough.” You may recall that Powell’s term as Fed Chair will expire in 2026. But there were concerns that President Trump could fire him, and that’s one of the reasons why the stock market was in a tizzy on Monday.

Thankfully, Trump quelled these fears in a press conference on Tuesday, where he stated that he has “no intention” of firing Powell.

It’s clear that Trump is frustrated that the Fed has not cut key interest rates this year, and he will likely blame the Fed and Powell if there is a recession. But for now, it looks like Powell will finish out his term as Fed Chair.

Green Shoot #3: Earnings Are Working

Now, the biggest green shoot is earnings.

The early quarterly earnings announcements are always the best, and that’s certainly been the case so far. Of the S&P 500 companies that have reported so far, 71% have exceeded analysts’ earnings estimates, posting an average 6.1% earnings surprise. FactSet now anticipates that the S&P 500 will achieve at least 7.2% average earnings growth for the first quarter.

But what really has me excited is the fact that early results have shown “earnings are working.” In other words, when a company with superior fundamentals beats analysts’ expectations, the stock rallies strongly.

Case in point: In Growth Investor, two of our stocks climbed 4% higher and more than 8% higher in the wake of their quarterly earnings beats on Tuesday. Then on Thursday, one of our stocks rallied 4% higher and another one jumped more than 8% after both companies topped analysts’ expectations.

So, we can count on wave after wave of better-than-expected sales and earnings to continue to propel fundamentally superior stocks higher in the upcoming weeks.

Get Ready for May Flowers

With tariff negotiations proceeding well, and tensions thawing between the U.S. and China, I expect trade barriers to continue to fall. And when it becomes clear that oppressive tariffs will not derail the U.S. economy, I look for the positive earnings environment and falling interest rates to serve as an incredible one-two punch that drives fundamentally superior stocks substantially higher.

The bottom line: Spring has now arrived – and it is time to cheer up, folks!

So, the question is… where do you find the best stocks with superior fundamentals?

The fact is the stocks I recommend in this service remain backed by superior fundamentals. And the proof is in the numbers…

Our Buy List stocks are characterized by 24% average annual sales growth and 81.1% average annual earnings growth. That compares to the S&P 500, which is expected to achieve an estimated 4.6% revenue growth and a 7.2% average earnings growth rate for the first quarter.

I should also mention that analysts have increased earnings estimates by an average of 3.8% in the past three months. So, the analyst community remains very positive on these stocks.

The Editor hereby discloses that as of the date of this email, the Editor, directly or indirectly, owns the following securities that are the subject of the commentary, analysis, opinions, advice, or recommendations in, or which are otherwise mentioned in, the essay set forth below:

Every Thursday, Freddie Mac, a government-sponsored buyer of mortgage loans, publishes a weekly average of 30-year mortgage rates. This week’s reading dipped 5 basis points to 6.76%. Last September, the average sank as far as 6.08%. But back in October 2023, Freddie Mac’s average saw a historic rise, surging to a 23-year peak of 7.79%.

Freddie Mac’s average differs from what we report for 30-year rates because Freddie Mac calculates a weekly average that blends five previous days of rates. In contrast, our Investopedia 30-year average is a daily reading, offering a more precise and timely indicator of rate movement. In addition, the criteria for included loans (e.g., amount of down payment, credit score, inclusion of discount points) varies between Freddie Mac’s methodology and our own.

Calculate monthly payments for different loan scenarios with our Mortgage Calculator.

Important

The rates we publish won’t compare directly with teaser rates you see advertised online since those rates are cherry-picked as the most attractive vs. the averages you see here. Teaser rates may involve paying points in advance or may be based on a hypothetical borrower with an ultra-high credit score or for a smaller-than-typical loan. The rate you ultimately secure will be based on factors like your credit score, income, and more, so it can vary from the averages you see here.

What Causes Mortgage Rates to Rise or Fall?

Mortgage rates are determined by a complex interaction of macroeconomic and industry factors, such as:

The level and direction of the bond market, especially 10-year Treasury yields

The Federal Reserve’s current monetary policy, especially as it relates to bond buying and funding government-backed mortgages

Competition between mortgage lenders and across loan types

Because any number of these can cause fluctuations simultaneously, it’s generally difficult to attribute the change to any one factor.

Macroeconomic factors kept the mortgage market relatively low for much of 2021. In particular, the Federal Reserve had been buying billions of dollars of bonds in response to the pandemic’s economic pressures. This bond-buying policy is a major influencer of mortgage rates.

But starting in November 2021, the Fed began tapering its bond purchases downward, making sizable reductions each month until reaching net zero in March 2022.

Between that time and July 2023, the Fed aggressively raised the federal funds rate to fight decades-high inflation. While the fed funds rate can influence mortgage rates, it doesn’t directly do so. In fact, the fed funds rate and mortgage rates can move in opposite directions.

But given the historic speed and magnitude of the Fed’s 2022 and 2023 rate increases—raising the benchmark rate 5.25 percentage points over 16 months—even the indirect influence of the fed funds rate has resulted in a dramatic upward impact on mortgage rates over the last two years.

The Fed maintained the federal funds rate at its peak level for almost 14 months, beginning in July 2023. But in September, the central bank announced a first rate cut of 0.50 percentage points, and then followed that with quarter-point reductions in November and December.

For its second meeting of 2025, however, the Fed opted to hold rates steady—and it’s possible the central bank may not make another rate cut for months. At their March 19 meeting, the Fed released its quarterly rate forecast, which showed that, at that time, the central bankers’ median expectation for the rest of the year was just two quarter-point rate cuts. With a total of eight rate-setting meetings scheduled per year, that means we could see multiple rate-hold announcements in 2025.

Editor’s note: “Explosive Growth Ahead? What the May 7 Market Shift Means for AI Stocks” was previously published with the title“AI Stocks Could Explode After the May 7 Market Shakeup” in April 2025. It has since been updated to include the most relevant information available.

What happens when you mix the most transformational technological megatrend of our lives (AI) with arguably the most ambitious U.S. president we’ve ever seen (Trump)?

You could ignite a $7 trillion Summer Panic in the markets… the sort of surge that we haven’t seen since the 1997 internet boom.

And we think that panic could unfurl as soon as next week, on May 7, when the White House is expected to kickstart an AI acceleration.

In short, investors are sitting on a record $7 trillion in cash, waiting for the opportunity to jump in. Private equity alone is holding at least $2.62 trillion, according to S&P Global Market Intelligence.

That means we could see an enormous return of this cash to the stock market this summer.

Because here’s the truth: What we’ve seen in 2025 isn’t the stock market’s first “crash” in recent years.

The 2010 Flash Crash. 2011’s U.S. debt ceiling downgrade, the 2015 yuan devaluation, and 2018’s Fed hike panic. The 2020 Covid crash and ‘22’s inflation meltdown.

All were buying opportunities for those who knew where to look.

In fact, it was during many of the last decade’s stock market crashes that I nailed the rise of the “Magnificent 7” stocks…

Finding Opportunity Amid the Market Volatility

Amid the commodity crisis of the mid-2010s, I picked out Meta Platforms Inc. (META), Apple Inc. (AAPL), Amazon.com Inc. (AMZN), and Microsoft Corp. (MSFT) as long-term winners. All four have recorded max gains of somewhere between 800% and 1,000% since.

Then, in February 2018, the stock market found itself in one of its fastest 10% corrections ever. On the other side of that plunge, I pinpointed Google as a long-term winner. It went on to soar nearly 300%.

And in the summer of 2019, stocks were stuck in another small selloff. That’s when I homed in on Tesla Inc. (TSLA) and Nvidia Corp. (NVDA) as great plays. Since then, Tesla has recorded a max gain of more than 3,700%, while Nvidia has shot up as much as 4,000%.

In other words, I called the Magnificent 7 before they were the Mag 7, and I did so during periods of elevated market volatility.

I don’t say this to brag but, rather, to highlight a truth that people often forget: Volatility creates opportunity.

Every selloff feels scary in the moment. But in hindsight, it’s clear to see that it was a blessing in disguise.

This time will be no different.

Beneath the surface of today’s market chaos, the next great tech rally is forming… but not in the Mag 7 stocks. Those are yesterday’s trades – not tomorrow’s big breakout.

In this new wave, the biggest winners will be what I’m calling the “MAGA 7.” I’m talking “Make AI Great in America” stocks.

The MAGA 7: AI Stocks Set to Soar From the Next Market Shock

AI is already very good in the United States. But in the next phase of the AI boom, it will become great. We will Make AI Great in America (MAGA) over the next few years.

My MAGA 7 are seven smaller AI stocks to watch – several of which you’ve likely never heard of – that are about to ride a wave of federal funding, corporate spending, and reshoring urgency into the spotlight.

These companies are building the tools. Laying the fiber. Supplying the chips. Automating the factories. And powering the intelligence behind America’s next great tech renaissance.

Very few are watching them right now. But after the panic hits on May 7, everyonecould be.

And if you get in beforethat moment…

Well, you know how this story goes.

Amazon in 1998, Nvidia in 2015, Tesla in 2019.

This is a rare chance to harness a massive market windfall.

According to McKinsey, generative AI could add up to $4.4 trillion to the global economy annually.

Meanwhile, the Biden administration has already committed over $140 billion toward U.S. semiconductor and AI-related infrastructure. With Trump likely to double down on reshoring and defense-grade AI, this opportunity could expand exponentially.

Of course, not every tech wave results in lasting gains; the 2000 crash taught us that. But today’s AI leaders are backed by real earnings, transformative use cases, and government contracts – not just clicks and eyeballs.

Andjust a few days ago, I heldan urgent briefingto help you get positioned for more AI stock profits.

We delved into:

The $7 trillion market panic that could ignite on May 7…

The real reason Trump’s actions are tied to the AI Boom…

And the MAGA 7 stocksthat I believe could soar as this chaos turns into opportunity.

After an April of roller coaster swings, 30-year refinance rates have been bobbing in a narrow range for the last week. Dipping 2 basis points Thursday, the flagship refi average is down to 7.03%. That’s better than April 11, when a week-long surge pushed the average to 7.31%—its most expensive level since July 2024.

Given the 30-year refi average fell as low as 6.71% in early March, however, today’s rates are elevated. The 30-year refi average is also more than a percentage point above last September’s two-year low of 6.01%.

Rates moved down for several other refi loan types as well. The 15-year and 20-year refi averages each slid a single basis point, while jumbo 30-year rates sank 21 points on average.

National Averages of Lenders’ Best Rates – Refinance

Occasionally some rate averages show a much larger than usual change from one day to the next. This can be due to some loan types being less popular among mortgage shoppers, such as the 10-year fixed rate, resulting in the average being based on a small sample size of rate quotes.

Important

The rates we publish won’t compare directly with teaser rates you see advertised online since those rates are cherry-picked as the most attractive vs. the averages you see here. Teaser rates may involve paying points in advance or may be based on a hypothetical borrower with an ultra-high credit score or for a smaller-than-typical loan. The rate you ultimately secure will be based on factors like your credit score, income, and more, so it can vary from the averages you see here.

Since rates vary widely across lenders, it’s always wise to shop around for your best mortgage refinance option and compare rates regularly, no matter the type of home loan you seek.

Calculate monthly payments for different loan scenarios with our Mortgage Calculator.

What Causes Mortgage Rates to Rise or Fall?

Mortgage rates are determined by a complex interaction of macroeconomic and industry factors, such as:

The level and direction of the bond market, especially 10-year Treasury yields

The Federal Reserve’s current monetary policy, especially as it relates to bond buying and funding government-backed mortgages

Competition between mortgage lenders and across loan types

Because any number of these can cause fluctuations at the same time, it’s generally difficult to attribute any single change to any one factor.

Macroeconomic factors kept the mortgage market relatively low for much of 2021. In particular, the Federal Reserve had been buying billions of dollars of bonds in response to the pandemic’s economic pressures. This bond-buying policy is a major influencer of mortgage rates.

But starting in November 2021, the Fed began tapering its bond purchases downward, making sizable reductions each month until reaching net zero in March 2022.

Between that time and July 2023, the Fed aggressively raised the federal funds rate to fight decades-high inflation. While the fed funds rate can influence mortgage rates, it doesn’t directly do so. In fact, the fed funds rate and mortgage rates can move in opposite directions.

But given the historic speed and magnitude of the Fed’s 2022 and 2023 rate increases—raising the benchmark rate 5.25 percentage points over 16 months—even the indirect influence of the fed funds rate has resulted in a dramatic upward impact on mortgage rates over the last two years.

The Fed maintained the federal funds rate at its peak level for almost 14 months, beginning in July 2023. But in September, the central bank announced a first rate cut of 0.50 percentage points, and then followed that with quarter-point reductions in November and December.

For its second meeting of 2025, however, the Fed opted to hold rates steady—and it’s possible the central bank may not make another rate cut for months. At their March 19 meeting, the Fed released its quarterly rate forecast, which showed that, at that time, the central bankers’ median expectation for the rest of the year was just two quarter-point rate cuts. With a total of eight rate-setting meetings scheduled per year, that means we could see multiple rate-hold announcements in 2025.

Last month, I wrote about five stocks to “buy the dip.” Our quantitative systems signaled April’s selloff had gone too far and that low prices would be enough to trigger a market rally.

Since then, these five firms have performed splendidly, largely outperforming the S&P 500’s 8% rise.

InvestorPlace Senior Analyst Luke Lango believes this is just the start.

He predicts a major event on May 7 will trigger a flood of cash – as much as $7 trillion – to rush back into U.S. stocks. It’s a catalyst that could change the entire market dynamic and create a new summer “panic” of the sort not seen since 1997.

This is why he held a special 2025 Summer Panic Summiton Thursday. At this event, Luke explained why he believes this catalyst on May 7 will be a game-changer. Plus, he revealed a new set of stocks that he believes are primed to lead the next wave of growth. (You can watch a replay of the event here.)

Now, I can’t tell you what this catalyst is. You’ll have to see it for yourself in Luke’s special presentation. But if this panic buying he describes does take off, several of my top long-term picks are certain to benefit.

Let’s revisit two of them today – and a new one as well…

The Leveraged Play

The first is Sabre Corp. (SABR), one of the three firms that run the world’s Global Distribution System (GDS) for hotels and flights. Virtually all travel agents and online booking systems use GDS to book flights since it’s the only platform with real-time data on available seats, rooms, and prices. That means industry profits are generally stable and very high. (Even Alphabet Inc. [GOOGL] failed to create a rival system and now uses Sabre to power Google Flights.)

That’s why private equity decided to take Sabre off the public markets in 2007. They saw a cash cow that could be loaded with debt to make large profits even bigger. And it worked, at least in the short run.

Sabre returned to public markets in 2014 with 50% higher net income, and the stock surged another 70% the following year as profits continued to climb.

Then, two things happened.

Covid-19. The once-in-a-century pandemic brought air travel to a near standstill, slashing Sabre’s revenues and making debts impossible to service.

Rising rates. The following year, the U.S. Federal Reserve began hiking interest rates to stave off inflation, making it harder for Sabre to pay off existing debts and roll them into new deals.

That crushed Sabre’s share price, which has fallen 90% since early 2020. Its debts are now worth almost six times more than its equity… a situation usually associated with near-bankrupt companies.

But if Luke’s calculations are right, things could soon turn around for this equity “stub.”

In fact, since the company is so financially leveraged, a 10% increase in enterprise value will translate into a 58% increase in share price.

That makes Sabre an incredible “option-like” play. In the worst case, the stock goes to zero… but in the best case, SABR shares could rise 2X… 5X… or even 10X.

The Real Estate Kings

The May 7 catalyst will also be felt among real estate companies that rely on more traditional debt financing.

My two favorites are on opposite ends of the risk spectrum. I would recommend both as complements.

Realty Income Corp. (O). This real estate investment trust (REIT) is arguably the most conservative of its kind. Leases are made on a “triple net” basis, meaning tenants are responsible for almost all costs, and the company attracts blue-chip tenants by offering minimal rent increases. Its dividend is paid monthly and sits at a stunningly high 5.6%.

Digital Realty Trust Inc. (DLR). Meanwhile, DLR is one of the most aggressive REITs thanks to its single-minded pursuit of growth in AI data centers. Gross income more than doubled to $2.9 billion in 2024, and analysts expect another 50% surge to $4.5 billion by 2027. Cloud computing firms like Microsoft Corp. (MSFT) are still starved for computing power, and Digital Realty has grown as quickly as possible to service that need. Dividends are lower at 3% to reflect this potential.

These two firms are well run. Realty Income has played the long game by focusing on grocery stores (10% of its portfolio), convenience stores (9%), non-retail stores (i.e., industrial and services) (21%), and other businesses resistant to e-commerce competition.

On its part, Digital Realty realized early on that cloud computing customers would need dense colocation data centers (where powered, connected warehouse space is rented out to firms that bring their own servers) and quickly moved to offer that service.

That means both firms should see a surge in buying interest on a May 7 catalyst. Despite their differences, these REITs are economically sensitive firms. And if Luke is right, a summer panic could send these types of companies soaring.

This high-quality biotech firm was created in 2003 in a mega-merger of Biogen and automation company Idec. Shares rose as much as 1,200% through the biotech boom of the mid-2010s as blockbusters like cancer drug Rituxan and MS therapy Avonex came onto the market. Biogen also proved reasonably adept at acquiring and partnering with other biotech firms, though a 2019 acquisition of Nightstar did end with two clinical failures.

Challenges began to mount after 2023 on rising research costs and high interest rates. Suddenly, new therapies became far more expensive to finance. A lackluster launch of Alzheimer’s drug Leqembi also spooked investors. So did recent staffing cuts at the U.S. Food and Drug Administration (FDA), which will increase the time and barriers for new drug approvals.

Biogen’s stock has dropped 60% over the past two years and trades at 8X forward earnings, compared to a long-term average of 13.3X.

The May 7 catalyst could change part of that equation.

This summer, we could see investors return to this beat-up stock whose forward price-earnings ratio now looks more like an automaker’s than a top-tier biotech’s. Biogen’s pipeline and several new launches look reasonably strong. Recently approved drugs like Skyclarys, used in neurology, and Zurzuvae, for postpartum depression, should reduce the impact of expiring drugs and Leqembi’s slower-than-expected success.

It’s also worth noting that large biotechs like Biogen have significant marketing and production scale that make them attractive partners, allowing them to snap up promising smaller firms at a discount.

Of course, many of Biogen’s challenges will remain. Biotech is an industry that generates enormous paydays and equally significant flops. I’m also not expecting a quick return to “normal” at the FDA.

Still, if you had told me two years ago that Biogen would be on sale at 8X forward earnings, I wouldn’t have believed you. And now, it’s something worth taking advantage of.

The Summer Panic of 1997

In May 1997, the Asian Financial Crisis was getting started. Currency speculators were dumping the Thai baht, forcing that country’s central bank to defend their currency exchange rate with a dwindling supply of foreign reserves. By July, these reserves had run out, triggering a devaluation and market mayhem. It only took several months for the crisis to spread to South Korea, Hong Kong, and beyond. Asian stock markets collapsed.

Yet, none of this affected the dot-com boom. Over the same period, the tech-heavy Nasdaq Composite surged 20% to a new record as American investors began recognizing the promises of the internet. Retail investors were more panicked about missing out than with some faraway financial crisis.

Luke Lango believes we’re approaching a new version of this two-sided “panic.”

Today, bearish institutional investors are dumping tariff-impacted companies as global macro fears kick in. Shares of Norwegian Cruise Line Holdings Ltd. (NCLH) have dropped 38%, while those of shoe retailer Deckers Outdoor Corp. (DECK) have sunk 45%.

Meanwhile, retail investors are aggressively buying the dip every chance they get. On April 3, individual investors bought $4.7 billion of equities following President Donald Trump’s “Liberation Day” selloff. And on Wednesday, a negative U.S. GDP report was quickly buried as these same mom-and-pop investors snapped up shares.

That’s because there’s a lot of money sitting on the sidelines. And there are a lot of bullish investors waiting to buy up stock.

This could come to a head on May 7, when Luke predicts an event will trigger a new cascade of retail buying.

Understandably, everyone is focused on short-term moves in the midst of a fast-paced market. But there’s something bigger happening behind the scenes…

Thomas Yeung is a market analyst and portfolio manager of the Omnia Portfolio, the highest-tier subscription at InvestorPlace. He is the former editor of Tom Yeung’s Profit & Protection, a free e-letter about investing to profit in good times and protecting gains during the bad.

The two states with the cheapest 30-year new purchase mortgage rates Thursday were New York and Washington. After that, the lowest rates were available in Tennessee, Texas, California, Florida, Michigan, North Carolina, and Pennsylvania. The nine states registered averages between 6.68% and 6.85%.

Meanwhile, the states with the highest Thursday rates were Alaska, West Virginia, Washington, D.C., Maryland, North Dakota, Rhode Island, and New Mexico. The range of averages for these states was 6.94% to 7.04%.

Mortgage rates vary by the state where they originate. Different lenders operate in different regions, and rates can be influenced by state-level variations in credit score, average loan size, and regulations. Lenders also have varying risk management strategies that influence the rates they offer.

Since rates vary widely across lenders, it’s always smart to shop around for your best mortgage option and compare rates regularly, no matter the type of home loan you seek.

Important

The rates we publish won’t compare directly with teaser rates you see advertised online since those rates are cherry-picked as the most attractive vs. the averages you see here. Teaser rates may involve paying points in advance or may be based on a hypothetical borrower with an ultra-high credit score or for a smaller-than-typical loan. The rate you ultimately secure will be based on factors like your credit score, income, and more, so it can vary from the averages you see here.

National Mortgage Rate Averages

After a dramatic up-and-down April, 30-year new purchase mortgages have calmed down, bobbing in a narrow range for the past week. Dipping 2 basis points Thursday, the 30-year national average is now 6.88%. In early April, rates surged 44 basis points in a week, shooting the average up to 7.14%—its most expensive level since May 2024.

In March, however, 30-year rates sank to 6.50%, their cheapest average of 2025. And in September, 30-year rates plunged to a two-year low of 5.89%.

Calculate monthly payments for different loan scenarios with our Mortgage Calculator.

What Causes Mortgage Rates to Rise or Fall?

Mortgage rates are determined by a complex interaction of macroeconomic and industry factors, such as:

The level and direction of the bond market, especially 10-year Treasury yields

The Federal Reserve’s current monetary policy, especially as it relates to bond buying and funding government-backed mortgages

Competition between mortgage lenders and across loan types

Because any number of these can cause fluctuations simultaneously, it’s generally difficult to attribute any change to any one factor.

Macroeconomic factors kept the mortgage market relatively low for much of 2021. In particular, the Federal Reserve had been buying billions of dollars of bonds in response to the pandemic’s economic pressures. This bond-buying policy is a major influencer of mortgage rates.

But starting in November 2021, the Fed began tapering its bond purchases downward, making sizable monthly reductions until reaching net zero in March 2022.

Between that time and July 2023, the Fed aggressively raised the federal funds rate to fight decades-high inflation. While the fed funds rate can influence mortgage rates, it doesn’t directly do so. In fact, the fed funds rate and mortgage rates can move in opposite directions.

But given the historic speed and magnitude of the Fed’s 2022 and 2023 rate increases—raising the benchmark rate 5.25 percentage points over 16 months—even the indirect influence of the fed funds rate has resulted in a dramatic upward impact on mortgage rates over the last two years.

The Fed maintained the federal funds rate at its peak level for almost 14 months, beginning in July 2023. But in September, the central bank announced a first rate cut of 0.50 percentage points, and then followed that with quarter-point reductions in November and December.

For its first meeting of the new year, however, the Fed opted to hold rates steady—and it’s possible the central bank may not make another rate cut for months. With a total of eight rate-setting meetings scheduled per year, that means we could see multiple rate-hold announcements in 2025.

The Walt Disney Company is set to report fiscal second-quarter results Wednesday morning, and analysts are largely bullish on the media and entertainment giant’s stock.

Analysts expect revenue to have risen from the year-ago quarter, but profit to have declined.

UBS analysts said they expect a strong quarter, but said a recession would pose risks to Disney’s advertising and experiences segments.

The Walt Disney Company (DIS) is scheduled to report fiscal second-quarter results before the opening bell Wednesday, and analysts are largely bullish on the media and entertainment giant’s stock.

Five of the seven analysts tracked by Visible Alpha who cover Disney rate the stock as a “buy,” while the other two dub it a “hold.” Their average price target is $120, a nearly 30% premium to the stock’s closing level Friday, suggesting analysts think shares will reverse their roughly 19% decline since the end of February.

The conglomerate is expected to report second-quarter revenue of $23.17 billion, up 5% year-over-year, while adjusted earnings per share are expected to have declined by a penny to $1.20.

Analysts Expect Solid Q2 But Warn of ‘Recession Risk’ Ahead

UBS analysts recently reiterated their “buy” rating in a note previewing Disney’s earnings, but trimmed their price target to $105 from $130. The analysts said they expect the firm’s second quarter to “reflect resilient demand across the parks, initial upside from the new cruise ship and solid sports advertising,” but see “recession risk” in the second half of the fiscal year that could hit advertising revenue and park visits.

Last quarter, Disney’s revenue and profit topped estimates, but it reported a slight drop in Disney+ subscribers to 124.6 million, and said it expected another “modest decline” in the second quarter. Visible Alpha consensus calls for 123.7 million Disney+ subscribers at the end of the second quarter.

President Donald Trump’s tariff policies and attacks on the Federal Reserve have sown doubts that U.S. assets are as safe as they have been historically.

This threatens the dollar’s status as the most widely used currency in global trade and weakens the dollar against a basket of foreign currencies.

However, analysts say it is unlikely to substantially shift the dollar’s role in the global economy.

As investors recover from a volatile month of tariff headlines, the lingering question on Wall Street is how much the U.S. dollar’s status as the pre-eminent global currency has weakened.

“King Dollar” is unlikely to be dethroned anytime soon given the lack of a reasonable alternative, analysts say. The dollar remains the most widely used currency in global trade, a role it’s held since the aftermath of World War II, and past efforts to replace it have sputtered.

Even so, President Donald Trump’s tariff policies and attacks on the Federal Reserve have sown doubts in global financial markets, fracturing that dominance. While he’s since eased up on both counts and U.S. stock markets have somewhat recovered, the doubts among global investors don’t seem to be fully going away.

“It is hard to put the genie back in the bottle once such concerns are raised,” Morgan Stanley strategist Vishwanath Tirupattur wrote in a note to clients last week.

However, he wrote, “practical realities” will make it difficult to massively shift the dollar’s role.

The Dollar Could Just Be Facing Temporary Weakness…

Since the dollar is integral to global trade, countries and their central banks hold large amounts of dollars in their coffers. The U.S. dollar made up about 57% of foreign exchange reserves last year, according to the International Monetary Fund, compared to 20% for the Euro, 6% for the Japanese yen and 5% for the Pound sterling.

The U.S. dollar was involved in about 90% of transactions in 2022 in the market where investors and companies trade foreign currencies, according to the Bank for International Settlements.

There is “really no alternative” to the dollar, said Brent Coggins, chief investment officer at Triad Wealth Partners in Kansas. The Euro is “very fragmented,” China’s currency doesn’t float freely in markets and the yen “doesn’t have scale” to compete, he said.

Dollar dominance has long irked some countries—and not just those subject to U.S. sanctions such as Russia or Iran. In the 1960s, a French official said the dollar’s reign gives the United States an “exorbitant privilege,” a moniker that’s stuck ever since.

More recently, the BRICS countries—which include Brazil, Russia, India, and China—have reportedly dropped the idea of developing a common currency even as they seek to bolster their local currencies in trading arrangements rather than the U.S. dollar. It was the latest victory for the U.S. dollar, which Coggins noted has thus far outlived a series of would-be alternatives.

“Even though it’s going through a disruption right now and people are challenging it, it’s dealt with challenges before, and it’s always come out ahead,” Coggins said. “We don’t see this being any different.”

…But It Still Faces A ‘Confidence Crisis’

Despite its historical dominance, the dollar is up against a broader “confidence crisis” in U.S. assets, said Arun Sai, senior multi-asset strategist at the European firm Pictet Asset Management.

Investors are questioning whether U.S. Treasury bonds—which the government issues to finance its deficits—are still the “safe haven” they used to be. They’re also shedding some of their holdings in U.S. stocks, with tech firms getting hit hard and worries over the U.S. economy clouding the outlook for others.

The selling of U.S. dollar assets has pressured the dollar, which has weakened 8% this year against a basket of foreign currencies.

Some analysts think the worst of it may be over. The dollar sell-off was “atypical and likely temporary,” Wells Fargo international economist Nick Bennenbroek wrote in a research note.

While Sai said the U.S. financial markets and “absolutely exceptional companies” still warrant investment, global asset managers like Pictet are rethinking their heavy U.S. exposures and weighing alternatives. Some are buying gold, which is hitting record highs. German bonds are also a popular option for those seeking a safe haven. Emerging markets are also seeing inflows.

Stocks closer to home are becoming a more attractive option as U.S. uncertainty rises, Sai said, adding that Trump’s policies have “incentivized capital to stay domestic.” When looking to deploy cash, Sai said he’s weighing assets in Europe and the U.K. “a little bit more than I would have last year.”

However, that could turn around, analysts said.

“We certainly understand why financial markets may be interested in reallocating away from U.S. assets at this particular time, but we ultimately think this shift is tactical rather than a fundamental reassessment of U.S. assets,” Bennenbroek wrote.

The Federal Reserve’s decision on interest rates is expected Wednesday.

Ford, Palantir, Advanced Micro Devices, Uber Technologies and Walt Disney are some of the companies set to report earnings this week.

Investors will also be watching for data on consumer credit, productivity and the U.S. trade balance.

Wednesday’s expected decision on interest rates from the Federal Reserve, along with earnings from several large tech and entertainment companies, could highlight a busy week ahead for investors.

Palantir (PLTR), Advanced Micro Devices (AMD), Uber Technologies (UBER) and Walt Disney (DIS) are some of the companies scheduled to report earnings. The week is also set to bring fresh data on consumer credit, productivity and the U.S. trade balance.

Monday, May 5

S&P services PMI (April)

ISM services PMI (April)

Palantir, Vertex Pharmaceuticals (VRTX), Ford (F), Tyson Foods (TSN), Clorox (CLX) and Onsemi (ON) are scheduled to report earnings

Tuesday, May 6

Federal Open Market Committee (FOMC) meeting begins

U.S. trade deficit (March)

Advanced Micro Devices, Ferrari (RACE), Arista Networks (ANET), Duke Energy (DUK), Marriott International (MAR) and Electronic Arts (EA) are scheduled to report earnings

Wednesday, May 7

FOMC interest rate decision

Fed Chair Jerome Powell press conference

Consumer credit (March)

Novo Nordisk (NVO), Uber Technologies, Walt Disney, Arm Holdings (ARM), AppLovin (APP), DoorDash (DASH), Carvana (CVNA) and Occidental Petroleum (OXY) are scheduled to report earnings

Thursday, May 8

Initial jobless claims (Week ending May 3)

U.S. productivity (Q1)

Wholesale inventories (March)

Shopify (SHOP), ConocoPhillips (COP), Anheuser-Busch InBev (BUD), Coinbase (COIN) and Kenvue (KVUE) are scheduled to report earnings

Friday, May 9

Federal Reserve Govs. Lisa Cook and Christopher Waller, New York Fed President John Williams, Cleveland Fed President Beth Hammack, St. Louis Fed President Alberto Musalem and Chicago Fed President Austan Goolsbee are scheduled to deliver remarks

Fed’s Interest Rate Decision Comes Amid Political Pressure to Lower Rates

The Federal Reserve’s interest rate decision on Wednesday comes as the central bank faces increasing political pressure to lower interest rates. But so far, investors don’t expect the Fed will lower rates from its current levels of 4.25%-4.5%, according to the CME Group’s FedWatch tool.

The Fed’s decision comes after the central bank got more encouraging inflation news last week when March’s inflation rate was in line with expectations, though still above the target. U.S. employers also added more jobs than expected in April, Friday’s jobs report showed.

Federal Reserve Chair Jerome Powell’s comments after the decision follow weeks of scrutiny from President Trump, which has raised questions over whether the president could remove the Fed chair from his position and what that would mean for central bank independence.

On Friday, the Federal Reserve’s blackout period ends with a noteworthy event that will feature a string of speakers that include Federal Reserve Governors Lisa Cook and Christopher Waller, New York Fed President John Williams, Cleveland Fed President Beth Hammack and St. Louis Fed President Alberto Musalem. Also speaking at the event is former Fed Governor Kevin Warsh, a key adviser to Trump who has been critical of the Federal Reserve and is thought to be one of the president’s candidates to succeed Powell.

Investors may also look to other key economic releases this week, including trade balance data on Tuesday and initial jobless claims on Thursday. Wednesday’s scheduled report on consumer credit comes as economists are evaluating consumer health amid faltering confidence, while Thursday’s wholesale inventories report could provide insight on supply chain resilience as trade tensions remain high.

Palantir, AMD, Ford, Disney and More Report Earnings

Ride-hailing company Uber and Danish pharmaceutical firm Novo Nordisk are set to follow Wednesday, along with Disney. The entertainment giant’s report Wednesday follows a better-than-expected quarter for the company as it continues to build out its streaming service, even as it reportedly laid off about 6% of its news and cable TV divisions.

Other companies due to release their latest quarterly financial results this week include Coinbase, Shopify, brewer Anheuser-Busch InBev, energy firms ConocoPhillips and Occidental Petroleum, delivery service DoorDash, online used car retailer Carvana and video game maker Electronic Arts.