After four straight weeks of heavy selling, the dollar finally found some footing. The rebound came as President Trump softened his tone — easing trade rhetoric, backing Fed independence, and signaling no plans to remove Chair Jerome Powell. Markets also took comfort from early signs that tensions with China might cool. Combined with deeply bearish USD sentiment and strong month-end rebalancing flows, the greenback finally caught a much-needed bid.

Meanwhile, bond market volatility has been extreme. Just three weeks ago, the 30-year Treasury yield ended the week at 4.41%; two trading sessions later, it spiked to 5%. In the meantime, the VIX touched 60, and bonds still couldn’t find a bid — highlighting the depth of market stress. By last week, yields had settled at 4.72%, but not before a 16-year duration Treasury had lost roughly 12% in just a few days — a brutal reminder of how sensitive long bonds are to yield shifts. The VIX also eased back to 24.8, displaying some relief in markets, which hardly have resolved deeper concerns.

Despite the softer tone from Washington, serious risks remain. Although reports suggested Presidents Xi and Trump were engaging in trade talks, the Chinese administration denied any imminent negotiations. Even with the April 12 exemption for computers and electronics, U.S. tariff rates remain alarmingly high — surpassing even post-Smoot-Hawley Act levels. The trade-weighted tariff rate on China, after adjustments, sits around 110%, a level that could severely disrupt, or even shut down, trade in many goods and inputs.

Looking ahead, a busy data calendar could shed light on how much damage is already done. Wednesday brings Q1 GDP and March personal income; Thursday, the March ISM manufacturing index; and Friday, the key April employment report. These releases may offer the first hard evidence of whether mounting fears are starting to hit the real economy.

GBP/USD turns at key 1.3400 level

George Vessey – Lead FX & Macro Strategist

The GBP/USD was higher last week but the sharp turn seen at the major technical level of 1.3400 means markets will be closely watching for any signs of weakness.

Tariff news took a back seat last week with markets instead focused on the renewed tension between US president Donald Trump and Federal Reserve chair Jerome Powell. Initially, worries that Trump was looking for ways to end Powell’s term saw the USD tumble, but a cooling of concerns saw the USD recover.

Technically, some momentum studies, like the relative strength index (RSI), have also suggested the GBP/USD could reverse.

Away from tariff news, key elections remain in focus this week. Notably, the Canadian national election, to be held on Monday, is expected to see a win for Mark Carney’s Liberal Party. Australia and Singapore both vote in national elections on Saturday.

ECB’s Kazaks warns against rate cuts

George Vessey – Lead FX & Macro Strategist

According to Bloomberg, Martins Kazaks, a member of the Governing Council, stated that the ECB should only cut rates to an “accommodation” level if the economic outlook significantly worsens.

Kazaks stated over the weekend in Washington, where he attended the IMF’s spring meetings, that while US tariff policies may slow down inflation and even trigger a recession, there is little indication of what will happen next and reducing too much would waste policy space.

“The question is more about whether we will have to go much lower below 2.00%, but we are at 2.25%,” he stated. “If it’s necessary, we’ll do it, but in order to do so and further reduce inflation, the state of the economy would need to deteriorate.”

EUR/USD has recently corrected from short-term highs. From here, the 21-day EMA support of 1.1219 will be crucial for EUR/USD.

GBP, euro end week lower

Table: seven-day rolling currency trends and trading ranges

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

German drug company Merck KGaA said Monday it has struck a deal to buy U.S. biotech firm SpringWorks Therapeutics for around $3.9 billion, expanding its portfolio of rare disease and cancer treatments.

Merck said it would offer $47 a share in cash for the Nasdaq-listed SpringWorks.

Merck’s offer represents a 26% premium to SpringWorks’ 20-day volume-weighted average price of $37.38 on Feb. 7, the day before speculation of a potential deal between the two started.

German drug company Merck KGaA said Monday it has struck a deal to buy U.S. biotech firm SpringWorks Therapeutics (SWTX) for around $3.9 billion, expanding its portfolio of rare disease and cancer treatments.

Shares of SpringWorks are up roughly 2% in premarket trading, while Merck shares are up about 1.5% in Frankfurt trading.

Merck said it would offer $47 a share in cash for the Stamford, Conn.-based firm. That represents a 26% premium to SpringWorks’ 20-day volume-weighted average price of $37.38 on Feb. 7—the day before speculation of a potential deal between the two started, Merck said. SpringWorks shares closed at $44.72 on Friday.

The transaction is expected to close in the second half of 2025, subject to SpringWorks’ shareholders approval and regulatory approvals. Merck said once the deal closes, it “will immediately contribute” to its revenue and is expected to be accretive to its earnings per share pre in 2027.

“The agreed acquisition of SpringWorks is a major step in our active portfolio strategy to position our company as a globally diversified, innovation and technology powerhouse,” Merck CEO Belén Garijo said. “For our Healthcare sector, it sharpens the focus on rare tumors, accelerates growth, and strengthens our presence in the U.S.”

Amazon is set to release its earnings report for the first quarter after the market closes on Thursday.

Analysts are bullish on the online retail and tech giant, and expect revenue and profits to rise in the quarter.

Amazon will likely face more questions on its AI spending plans, and the impact of the Trump administration’s tariffs on its business.

Amazon (AMZN) is expected to release first-quarter results after the closing bell on Thursday, with analysts bullish on the online retail and tech giant.

All 26 analysts tracked by Visible Alpha who follow the company rate Amazon’s stock as a “buy,” with every analyst holding a price target above the stock’s current levels. The average price target is around $243, a premium of about 29% to Friday’s close but down from about $259 ahead of last quarter’s report.

Amazon is expected to report $154.96 billion in revenue for the first quarter, up 8% from the first quarter a year ago. Adjusted earnings per share are expected to rise to $1.74 from $1.46 the same time last year.

Amazon shares have declined about 14% since the start of the year, amid a tariff-fueled market sell-off that has hit the Magnificent Seven hard.

Amazon stock was downgraded earlier this month by Raymond James analysts who said tariffs on China could hurt Amazon’s profit margins and lead to a pullback in advertising revenue from sellers on the platform who rely on Chinese imports.

Morgan Stanley analysts wrote recently that they estimate 18% of products on Amazon are imported from China, and that roughly 60% of third-party sellers on the platform have “some China exposure” that could affect ad spending plans.

The GBP/USD was higher last week but the sharp turn seen at the major technical level of 1.3400 means markets will be closely watching for any signs of weakness.

Tariff news took a back seat last week with markets instead focused on the renewed tension between US president Donald Trump and Federal Reserve chair Jerome Powell. Initially, worries that Trump was looking for ways to end Powell’s term saw the USD tumble, but a cooling of concerns saw the USD recover.

Technically, some momentum studies, like the relative strength index (RSI), have also suggested the GBP/USD could reverse.

Away from tariff news, key elections remain in focus this week. Notably, the Canadian national election, to be held on Monday, is expected to see a win for Mark Carney’s Liberal Party. Australia and Singapore both vote in national elections on Saturday.

ECB’s Kazaks warns against rate cuts

According to Bloomberg, Martins Kazaks, a member of the Governing Council, stated that the ECB should only cut rates to an “accommodation” level if the economic outlook significantly worsens.

Kazaks stated over the weekend in Washington, where he attended the IMF’s spring meetings, that while US tariff policies may slow down inflation and even trigger a recession, there is little indication of what will happen next and reducing too much would waste policy space.

“The question is more about whether we will have to go much lower below 2.00%, but we are at 2.25%,” he stated. “If it’s necessary, we’ll do it, but in order to do so and further reduce inflation, the state of the economy would need to deteriorate.”

EUR/USD has recently corrected from short-term highs. From here, the 21-day EMA support of 1.1219 will be crucial for EUR/USD.

All eyes on inflation and growth data this week

The upcoming week will see inflation data emerge as the central focus across major economies. In Australia, Q1 CPI figures (Wednesday) are expected to show a quarterly rise of 0.8% QoQ and 2.3% YoY, which could provide insight into the Reserve Bank of Australia’s policy trajectory.

Meanwhile, preliminary inflation readings from Germany and France (Wednesday) will offer a closer look at price pressures within the Eurozone, with Eurozone-wide CPI data due Friday. These data points will likely shape expectations around the European Central Bank’s (ECB) next moves.

Additionally, the US will release its Personal Income and Spending (Thursday) alongside the PCE price index—widely regarded as the Federal Reserve’s preferred measure of inflation. These figures will be closely monitored amidst ongoing speculation about the Fed’s future rate decisions.

Growth metrics will also be in focus. The US Q1 GDP preliminary reading (Wednesday) is expected to show annualized growth of 0.4%. The Eurozone will release Q1 GDP estimates as well. This, alongside PMI data from the manufacturing sector in US (Thursday) and across Europe (Friday), will offer further context on the region’s economic momentum.

The Bank of Japan (BoJ) will announce its policy decision on Thursday, with the target rate expected to remain unchanged at 0.5%.

Labour market data from the US (Friday) will be a key highlight, with nonfarm payrolls expected to rise by 123k in April, a notable slowdown from March’s strong 228k reading. The unemployment rate is forecast to hold steady at 4.2%. These figures will provide insight into the resilience of the US labour market amidst tighter monetary conditions.

The UK calendar looks light, with CBI realized sales on Monday, BRC shop price index on Tuesday and loan growth numbers due Thursday.

GBP, euro end week lower

Table: seven-day rolling currency trends and trading ranges

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Apple shares will be in the spotlight ahead of the iPhone maker’s highly anticipated fiscal second-quarter results, due after Thursday’s closing bell.

Wall Street will be paying close attention to the tech giant’s guidance for the current quarter in an effort to determine what impact tariffs and potential price increases have had on consumer demand.

The stock trades significantly above this month’s low, though the relative strength index signals lackluster price momentum ahead of earnings.

Investors should monitor key support levels on Apple’s chart around $169 and $157, while also watching crucial resistance levels near $220 and $237.

Apple (AAPL) shares will be in the spotlight ahead of the iPhone maker’s highly anticipated fiscal second-quarter results, due after Thursday’s closing bell.

Wall Street will be paying close attention to the tech giant’s guidance for the current quarter in an effort to determine what impact tariffs and potential price increases have had on consumer demand for the company’s devices.

Investors will also be looking for updates on recent reports that Apple intends to produce most of its U.S.-sold iPhones in India by the end of 2026. The company is aiming to mitigate risks related to the Trump administration’s steep import duties imposed on China, a country where Apple reportedly assembles up to 90% of its iPhones.

Apple shares trade 16% lower year to date as of Friday’s close but have recovered nearly 25% from this month’s low as investors assess the company’s plans to navigate tariff-related challenges.

Below, we break down the technicals on Apple’s weekly chart and identify key price levels worth watching ahead of the tech giant’s earnings report.

Lackluster Price Momentum Ahead of Earnings

After staging a dramatic intraday reversal at the 200-week moving average (MA) on above-average volume earlier this month, Apple shares have continued to gain ground.

However, while the relative strength index (RSI) has moved upwards ahead, the indicator remains just below the 50 threshold, signaling lackluster price momentum.

Let’s point out key support and resistance levels on Apple’s chart that investors will likely be monitoring.

Key Support Levels to Monitor

The first area to monitor sits around $169. Retracements to this level on the chart would likely attract strong buying interest near this month’s low, which also closely aligns with the August 2022 peak and troughs in October 2023 and April 2024.

The bulls’ failure to defend this key technical level opens the door for a drop to lower support at $157. Investors could seek entry points in this region near a horizontal line that connects several peaks and troughs on the chart between September 2021 and March 2023.

Crucial Resistance Levels to Watch

In the event of a rally, it’s worth keeping an eye on the $220 level, an area currently just below the 50-week MA. The shares could run into selling pressure in this location near price action on the chart extending back to June last year.

Finally, further buying could see Apple’s stock revisit the $237 area. Investors who have accumulated shares at lower prices may seek profit-taking opportunities in this region near last year’s July and October peaks.

The comments, opinions, and analyses expressed on Investopedia are for informational purposes only. Read our warranty and liability disclaimer for more info.

As of the date this article was written, the author does not own any of the above securities.

Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

Aussie lower as elections loom

The Australian dollar was lower over the long weekend ahead of a major week of Australian news that sees the key March-quarter inflation numbers due on Wednesday and the Federal election on Saturday.

The AUD/USD had climbed to four-month highs last week – in line with gains in global equity markets – but the pair eased back from these highs on Friday.

The NZD/USD was also lower on Friday as the kiwi reversed after briefly trading above 0.6000 last week for the first time since November.

Key elections remain in focus in other parts of the world with the Canadian national election to be held on Monday — and expected to see a win for Mark Carney’s Liberal Party.

The Singapore national election is due on 3 May. Lawrence Wong’s People’s Action Party is seen as likely to win.

The USD/SGD was higher on Friday with the pair near two-week highs.

China-US trade talks and China-EU partnerships

A representative for China’s Commerce Ministry stated that “any reports on development in talks are groundless” and urged the US to lift all unilateral tariffs.

US President Donald Trump claimed that his administration has been meeting with Chinese officials on trade.

President Xi Jinping is working to mend fences with the European Union in the meanwhile.

According to a European official quoted by Bloomberg, Xi is getting ready to remove penalties on a number of EU legislators, and EU authorities are thinking about removing tariffs on Chinese electric vehicles.

European leaders may talk about resurrecting an investment treaty and expanding trade with China at a conference scheduled for July in Beijing.

USD/CNH remains around 2% below its recent all-time highs of 7.4290.

USD/CNH has been sitting on support line of 50-day EMA of 7.2834, where USD buyers may look to take advantage.

The next key resistance for the pair remains key psychological level of 7.3000 and 7.3500.

All eyes on inflation and growth data this week

The upcoming week will see inflation data emerge as the central focus across major economies. In Australia, Q1 CPI figures (Wednesday) are expected to show a quarterly rise of 0.8% QoQ and 2.3% YoY, which could provide insight into the Reserve Bank of Australia’s policy trajectory.

Meanwhile, preliminary inflation readings from Germany and France (Wednesday) will offer a closer look at price pressures within the Eurozone, with Eurozone-wide CPI data due Friday. These data points will likely shape expectations around the European Central Bank’s (ECB) next moves.

Additionally, the US will release its Personal Income and Spending (Thursday) alongside the PCE price index—widely regarded as the Federal Reserve’s preferred measure of inflation. These figures will be closely monitored amidst ongoing speculation about the Fed’s future rate decisions.

Growth metrics will also be in focus. The US Q1 GDP preliminary reading (Wednesday) is expected to show annualized growth of 0.4%. The Eurozone will release Q1 GDP estimates as well. This, alongside PMI data from the manufacturing sector in US (Thursday) and across Europe (Friday), will offer further context on the region’s economic momentum.

The Bank of Japan (BoJ) will announce its policy decision on Thursday, with the target rate expected to remain unchanged at 0.5%.

Labour market data from the US (Friday) will be a key highlight, with nonfarm payrolls expected to rise by 123k in April, a notable slowdown from March’s strong 228k reading. The unemployment rate is forecast to hold steady at 4.2%. These figures will provide insight into the resilience of the US labour market amidst tighter monetary conditions.

Aussie, kiwi lower over weekend

Table: seven-day rolling currency trends and trading ranges

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Editor’s Note: It’s no secret that President Donald Trump wants to bring manufacturing back to the United States. And while headlines focus on reshoring and rebuilding American manufacturing, few are asking the obvious question: Who is going to do the work?

The answer isn’t “more workers.”

It’s machines.

That is why my InvestorPlace colleague Luke Lango is holding a special 2025 Summer Panic Summit on May 1 at 7 p.m. Eastern.

At the event, Luke will share why he is predicting a buying frenzy, fueled by investors redeploying cash into stocks. He will also introduce a new set of seven small-cap U.S.-based AI stocks, dubbed the “MAGA 7” (Make AI Great in America), as the key to building a “nest egg” in this new bull market.

Luke is joining us today to break down why physical AI — robots, automation, and machine vision — is the only way the industrial revival can realistically take shape.

With a historic $7 trillion sitting on the sidelines and a potential market-shaking event on the horizon, we may be on the cusp of a full-blown investment supercycle.

Take it away, Luke…

Here is a hard truth few in Washington will say out loud.

President Trump’s economic agenda faces a major challenge.

Reindustrializing America. Reshoring manufacturing. Bringing back “Made in the USA.”

Trump has made this a central part of his economic agenda.

But no one is talking about a major roadblock preventing all this from happening.

Here is the hard truth: You can’t bring back American manufacturing unless robots do most of the work.

It’s all about the numbers.

There simply are not enough people, enough skill, or cheap enough labor to make it happen any other way.

That reality means one thing for investors: physical AI — not just digital AI — is about to explode.

However, the stocks of companies developing and using physical artificial intelligence – robotics and other forms of AI-powered automation – can’t explode yet.

They need a catalyst.

Something that will uncap $7 trillion in cash that’s been sitting on the sidelines and, basically, cause a “Summer Panic” in the markets.

So in this issue, let’s dig a little deeper into that catalyst – and all 7 trillion of those dollars.

Plus, I’ll start to show you why this “Summer Panic” could drive physical AI stocks higher.

And I’ll reveal the No. 1 way you can position yourself to grab some of those gains.

Take a look…

An Imminent $7 Trillion “Summer Panic” Catalyst

Today, roughly $7 trillion is parked in money‑market funds, earning about 4.5% while investors wait for better opportunities to pop up.

In other words, we’re all waiting for a catalyst that could be the pin that pops the “cash bubble,” unleashing a violent rotation back into stocks — what we’re calling the 2025 Summer Panic

In fact, I’m so confident that this big event scheduled to take place very soon — May 7 to be exact – that it is virtually guaranteed to trigger huge moves in the market.

It has been almost 30 years — since 1997 — since investors last saw the same one‑two punch of this bullish signal and a breakthrough technology platform. Back then it was the internet. This year it is artificial intelligence.

When that cash stampede begins, history suggests it will not dribble in slowly. In 1997 the same signal sent money‑market balances down 8% in a single quarter and ignited a two‑year melt‑up that minted millionaires.

I believe the setup is even stronger now. And on May 7, the $7 trillion sitting in cash could rush toward the very companies building America’s AI‑powered factory floor.

Trump’s Reshoring Agenda: Big Vision, Big Problem

President Trump is pushing what may be the boldest industrial policy in U.S. history — a $500 billion commitment to expand AI infrastructure through the Stargate Project, support domestic manufacturing, and restore U.S. supply‑chain independence.

It is a compelling vision: chip fabs in Ohio, EV‑battery plants in Michigan, robotics in Texas, steel in Pennsylvania.

But no one is talking about a major problem: Who is going to work in all these factories?

Labor Supply: The People Simply Aren’t There

As of today, fewer than 2 million Americans are filing for unemployment benefits. Meanwhile, the president’s reshoring goals imply replacing tens of millions of overseas manufacturing jobs.

China has more than 100 million manufacturing workers.

India has about 20 million.

Vietnam has more than 10 million.

That is 130 million to 150 million manufacturing jobs in just three Asian countries, many of which feed U.S. supply chains. Yet the United States cannot staff its existing plants, never mind an expanded industrial base, without automation.

Labor Quality: Americans Don’t Want These Jobs

The United States offshored manufacturing work for a reason. The positions are difficult, often dangerous, and generally not the kind of roles in which young Americans see a future.

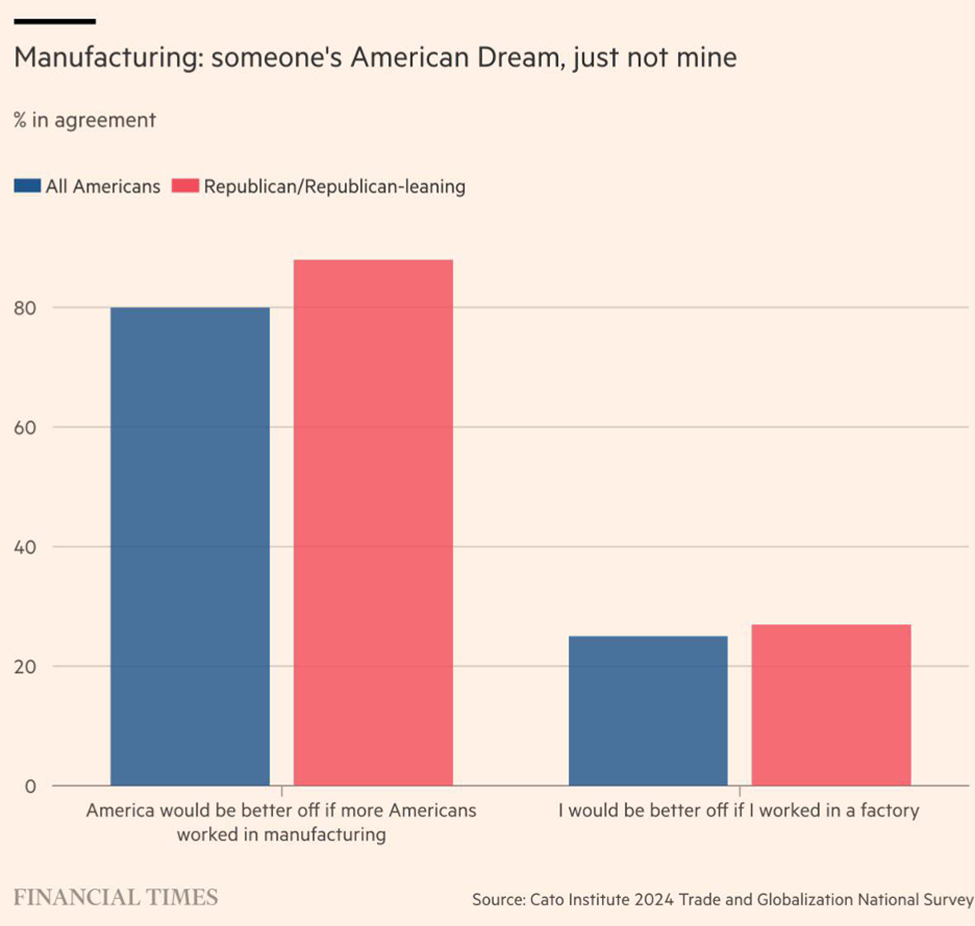

A recent Cato Institute survey captured the mismatch:

80% of respondents say the nation would be better off if more people worked in manufacturing.

Only 20% say they would be better off working in a factory.

The workforce has moved on.

But, if President Trump has his way, the factories will be moving back.

Labor Cost: We Can’t Compete on Wages

The economics here are even starker:

Minimum wage in China averages about $300 a month.

Vietnam: roughly $200.

India: below $200 in many regions.

U.S. federal minimum wage implies more than $1,200 a month, and factories often pay far more.

U.S. labor is four to six times as expensive as most Asian labor. That math doesn’t pencil out unless companies deploy AI-powered machines that don’t take breaks, benefits, or paid time off.

Robots: The Only Way Reshoring Works

Put simply: Trump’s industrial renaissance only works if robots build it.

The 21st‑century American factory will not look like Detroit in the 1950s. It will look like Tesla Inc.’s (TSLA) Gigafactory, multiplied across industries.

There will be fewer humans working inside them, replaced instead by dozens of industrial arms, autonomous material handling, machine vision‑based quality-assurance systems, and zero‑light warehouses.

The goal may be to replace Chinese or Indian labor with American labor. The reality is that we’ll replace foreign humans with domestic machines.

That is why our team sees physical AI — robots, automation systems, machine vision — as the next leg of the AI Revolution.

Enter the Physical AI Revolution

Until now, most of the AI hype has revolved around language models, chatbots, and digital copilots. Those software breakthroughs have been transformative for knowledge work.

But the next frontier is the physical world:

Factory robots that can see, learn, and adapt.

Warehouse pick‑and‑pack bots powered by machine vision models.

Autonomous forklifts and mobile platforms.

AI‑driven robotic arms that can manufacture, weld, and inspect.

With Stargate’s build‑out of domestic compute capacity, that kind of robotic intelligence can scale quickly. Just as ChatGPT catalyzed digital AI adoption, the Trump administration-supported 2025‑’26 infrastructure wave could catalyze physical‑AI adoption across manufacturing, logistics, and defense.

Finding market-beating investments within emerging tech megatrends such as this is exactly what I excel at. My predictive record in emerging tech is well documented:

TipRanks named me the No. 1 Stock Picker of 2020, out of more than 15,000 professionals.

Since 2014, I have highlighted almost 200 stocks that went on to double and more than a dozen that soared 10X, 20X, even 30X — including Alphabet Inc. (GOOG), Amazon.com Inc. (AMZN), Meta Platforms Inc. (META), Apple Inc. (AAPL), Microsoft Corp. (MSFT), Tesla Inc. (TSLA), and Nvidia Corp. (NVDA) long before they were household names.

Those “Mag 7” calls turned a hypothetical $70,000 total investment (seven positions at $10,000 each) into about $1.2 million at peak.

Now, I believe the next wealth‑defining list will be a basket of small, U.S.‑based physical‑AI leaders I’m calling the “MAGA 7.” No, I’m taking political sides here.

In this case, “MAGA” stands for Make AI Great in America.

The Generational‑Wealth Window

This rare alignment of (1) a rally-inducing market signal (the one I’m predicting will happen on May 7), (2) a record cash hoard, and (3) a breakthrough technology platform has happened once in modern history — the late‑1990s dot‑com era.

Investors who acted early in 1997 could have turned five‑figure stakes into six‑ and seven‑figure fortunes in just a few years.

If I’m right, May 7 could mark the start of a second, and possibly larger, melt‑up — one in which physical‑AI winners become the new titans of American industry.

That is the sort of opportunity often described as “generational wealth.” It is not about adding a few percentage points to a portfolio. It is about potentially changing a family’s balance sheet for decades.

This is not merely a policy trend. It is an investment megatrend.

The economic math points to automation.

Political momentum points to domestic buildout.

The AI infrastructure build points to a physical AI supercycle.

President Trump wants to bring manufacturing back to America, but only robots can make the math work. If the Fed signals an easing cycle on May 7, the $7 trillion in sidelined cash could rush into the exact names supplying America’s next factory workforce.

That is why this coming Thursday, May 1, at 7 p.m. Eastern, I’m hosting an urgent strategy online session. During the event I’ll show you how we can not only protect our portfolios this summer… but also see triple-digit gains in the coming years.

Plus, like I’ve been saying, I’ll detail seven new opportunities – the “MAGA 7” – at the center of this historic Summer Panic.

$7 trillion in sideline cash could soon flood the market…

Tom Yeung here with your Sunday Digest.

In the 1990s, my father moved our family to a new overseas “Florida-style” housing development. The land was cheap… the house was reasonably priced… and we needed the space.

At first, he wasn’t sure he had made the right decision. Our home was far from the city and stood in a former swamp. He watched nervously as home prices stayed stagnant like the water in our backyard.

But then came the catalyst: The local government replaced the four-lane road outside our development with a mega-highway.

After that, everything changed at once. Waterways were rerouted to drain the neighborhood, shopping malls were built nearby, and more houses quickly appeared. Suddenly, our home was worth multiples of what my father had originally paid.

These sorts of catalysts are often the most important thing in investing. Regional banks and biotechs can trade sideways for years… and then surge 100% on a takeover offer. Falling stocks tend to continue downward until a good news catalyst stems the tide.

Now, InvestorPlace Hypergrowth Specialist Luke Lango believes he’s identified a new catalyst that will change the entire market.

In fact, he’s so confident that a big event scheduled to take place May 7 is virtually guaranteed trigger huge moves in the market. While I can’t explain everything in this Digest, Luke is hosting his 2025 Summer Panic Summit on Thursday, May 1, at 7 p.m. Eastern to give you all the details and help you prepare. You can click here to reserve your spot now.

Of course, the fundamental value of a company remains the best gauge of a stock’s value. A catalyst alone isn’t enough to sustain a stock price.

But achieving that value often takes a push in the right direction. So, let’s consider three more companies that I recommend buying the dip on in anticipation of this game-changing May 7 catalyst.

Built for the Storm

In January, I wrote about CME Group Inc. (CME), a financial exchange that historically performs best during rising markets and periods of volatility. The Chicago-based exchange has exclusive licenses to issue futures contracts on the S&P 500, Russell 2000, and Nasdaq indexes, and more than 95% of all U.S. interest-rate futures trade on CME’s exchange.

Professional traders essentially must use CME’s products to help reduce risk (or profit from it).

As expected, the past several months have proven a windfall for the exchange. On April 23, CME Group reported that revenues had risen 10% to $1.6 billion, and earnings per share (EPS) were up 12% to $2.80. Shares have climbed 12% since that recommendation, compared to a 10% decline in the S&P 500.

CME should see another price jump over the next 30 days, especially given the muted price reaction to first-quarter earnings. Volatility is spiking, and the uncertainty sparked by President Donald Trump’s “Liberation Day” tariffs has sent trading volumes on the CME exchange to near-record highs. Daily traded volumes for April currently average 40 million contracts, compared to 29.8 million in the first quarter and 7.8 million in 2024.

That should help CME do well. President Trump has yet to finalize any trade deals with the 75 countries he’s pledged to do with, so don’t count on volatility suddenly going away.

The Taxman Comes

We knew going into 2025 that taxes would be a hot topic. President Trump’s 2017 Tax Cuts and Jobs Act (TCJA) expires this year, and Congress must propose a replacement. Here’s what I noted last December when naming Intuit Inc. (INTU)my No. 5 pick for 2025:

Tax changes for 2025 should reaccelerate growth. The incoming president has suggested he will implement sweeping overhauls, including tariffs, tax cuts on tips, and changes to how Social Security works.

This will create a bonanza for companies like Intuit, which saw a similar boost during Trump’s first presidency – with shares rising 38% in Trump’s first year in office alone. Some campaign promises – such as no taxes on tips – will spawn thousands of inventive ways to avoid taxes.

Shares of this blue-chip software firm have slipped just 4% since that recommendation, compared to a 13% retreat in the tech-heavy Nasdaq-100 index.

Now, I believe another breakout moment is coming for Intuit. Over the past 15 years, shares of the tax and accounting firm have risen 10% on average between May and July. (Markets seem consistently surprised that Intuit’s TurboTax software does so well in March and April.) In addition, the White House and Congress have recently begun talking about how to pay for an extension of the TCJA… and it’s going to be complicated.

That should cause Intuit’s shares to grind higher as the Trump administration floats new tax ideas. The stock trades at a reasonable 30X forward earnings – 15% below its five-year average of 35X – and significant changes to America’s tax code should provide a boost to demand.

A Conservative Play

Finally, several banks seem ripe for investment.

And the one that stands out most is U.S. Bancorp (USB).

USB is one of America’s best-run banks. The Minneapolis-based firm has high profits, excellent cost controls, and conservative underwriting. Net charge-offs peaked at just 2.5% of loans during the depths of the financial crisis – well below the 3%-plus rates of rival firms. Its cyclical midpoint return on equity (ROE) of 13% sits a third higher than the industry median.

This quality obviously comes with a price tag. Shares have traded at an average of 1.8X price-to-book value since 2005, and price-to-earnings ratios typically sit in the low teens.

However, recent fears of a U.S. recession have pushed shares to unusually low levels. As shown in the graph below, USB has only dipped below the 1.0X price-to-book mark three times in the past 20 years.

2008: The Global Financial Crisis

2020: The Covid-19 Pandemic

2023: The U.S. Regional Banking Crisis

That presents an opportunity. As Luke will explain in his presentation on Thursday, May 1, which you can register for now, he expects to see stocks like USB undergo a “V”-shaped recovery like we saw in 2009. That should send multiples of USB back into the 1.25X to 1.5X range, a 25% to 50% upside.

It’s important to note that the conservative nature of USB means its upside will be limited to 50%. It’s not a moonshot bet like Moderna Inc. (MRNA) or other firms I’ve recently talked about. But for conservative investors looking for some “singles” to complement home runs, it’s hard to beat the quality of U.S. Bancorp.

The Opportunity of a Generation

Stories like my father’s don’t come around very often. Housing prices usually rise in the low single-percentages… unless you managed to buy a New York City apartment in 1975 or Florida real estate in 1990.

The same is usually true for stocks. It’s not every day you see 2X… 5X… 10X returns.

But Luke Lango is seeing a new catalyst that could drive stocks higher… the sort of surge that we haven’t seen since the 1997 internet boom.

That’s because investors are currently sitting on a record $7 trillion in cash, waiting for the opportunity to jump in. Private equity alone is sitting on at least $2.62 trillion, according to S&P Global Market Intelligence.

That means we could see an enormous return of this cash to the stock market this summer.

Which is why this coming Thursday, May 1, at 7 p.m. Eastern, Luke is hosting an urgent strategy online session. During the event he’ll show us how we can not only protect our portfolios this summer… but also see triple-digit gains in the coming years.

Plus, he plans to detail seven new opportunities at the center of this historic summer panic.

Thomas Yeung is a market analyst and portfolio manager of the Omnia Portfolio, the highest-tier subscription at InvestorPlace. He is the former editor of Tom Yeung’s Profit & Protection, a free e-letter about investing to profit in good times and protecting gains during the bad.

Skechers USA shares tumbled Friday morning after the footwear maker withdrew its full-year sales and profit forecasts.

The company said it was “due to macroeconomic uncertainty stemming from global trade policies.”

Skechers’ first-quarter results also came in just below analysts’ estimates.

Skechers USA (SKX) shares tumbled in premarket trading Friday, a day after the footwear maker pulled its full-year forecasts amid tariffs uncertainty.

The shoe company said after the bell Thursday that it was suspending its full-year outlook it provided last quarter “due to macroeconomic uncertainty stemming from global trade policies.”

In February, Skechers’ fiscal 2025 outlook disappointed as the company said it expected sales of $9.7 billion to $9.8 billion and earnings per share (EPS) of $4.30 to $4.50.

For the first quarter, Skechers reported $2.41 billion in sales along with adjusted EPS of $1.17, with both metrics coming in narrowly below Visible Alpha consensus estimates.

Last month, Morgan Stanley analysts said footwear makers like Skechers could be particularly hard hit by tariffs on imports from countries like Vietnam, as roughly a third of the shoes imported into the U.S. last year came from the country. They said it would likely be difficult for many shoe companies to raise prices to offset the tariff costs without hurting demand for their products.

Skechers shares, which had lost about a quarter of their value so far this year entering Friday, were down 6.5% in premarket trading.

The president wants to reindustrialize America. There’s just one teensy problem…

Steel mills, chip fabs, and assembly lines buzzing with “Made in the U.S.A.” labels: The president has promised all of this in a bid to get America’s factories booming.

There’s just one teensy problem…

A problem no one on Capitol Hill dares to whisper, let alone solve…

You can’t rebuild American manufacturing without robots.

In America, there’s an abundance of “not enough.” We have: not enough workers, not enough skills, not enough cheap labor. The math is clear — automation must fill the gap.

That’s why the next great fortune won’t come from chatbots or cloud software. It will come from physical AI—the robotic arms, vision sensors, and autonomous movers that transform concrete slabs into fully automated factories.

Need proof? Look at the cash on the sidelines: about $7 trillion parked in money-market funds, earning table scraps. History says that money never sits still for long. All it needs is a spark to stampede into the market.

That spark could be the “Summer Panic” — an event poised to pop the cash bubble and catapult physical-AI stocks into a once-in-a-generation run.

In today’s issue you’ll discover:

The hidden catalyst that could send idle trillions racing into robotics.

Why past “breadth thrusts” signaled double-digit gains — and why this one could be bigger.

The No. 1 stock to buy before the machines reclaim America’s assembly lines.

Washington won’t talk about this roadblock. Wall Street hasn’t priced it in. But savvy investors who act now could ride the automation wave long before Main Street sees it coming.

Strap in — the robots are clocking in, and the real money is about to follow.

In other words, we’re all waiting for a catalyst that could be the pin that pops the “cash bubble,” unleashing a violent rotation back into stocks — what we’re calling the 2025 Summer Panic

In fact, I’m so confident in this big event scheduled to take place very soon – May 7 to be exact – that it is virtually guaranteed to trigger huge moves in the market. That’s why I’m hosting a 2025 Summer Panic Summit on Thursday, May 1, at 7 p.m. Eastern to give you all the details and help you prepare. You can click here to reserve your spot now.

It has been almost 30 years — since 1997 — since investors last saw the same one‑two punch of this bullish signal and a breakthrough technology platform. Back then it was the internet. This year it is artificial intelligence.

When that cash stampede begins, history suggests it will not dribble in slowly. In 1997 the same signal sent money‑market balances down 8% in a single quarter and ignited a two‑year melt‑up that minted millionaires.

I believe the setup is even stronger now. And on May 7, the $7 trillion sitting in cash could rush toward the very companies building America’s AI‑powered factory floor.

Trump’s Reshoring Agenda: Big Vision, Big Problem

President Trump is pushing what may be the boldest industrial policy in U.S. history — a $500 billion commitment to expand AI infrastructure through the Stargate Project, support domestic manufacturing, and restore U.S. supply‑chain independence.

It is a compelling vision: chip fabs in Ohio, EV‑battery plants in Michigan, robotics in Texas, steel in Pennsylvania.

But no one is talking about a major problem: Who is going to work in all these factories?

Labor Supply: The People Simply Aren’t There

As of today, fewer than 2 million Americans are filing for unemployment benefits. Meanwhile, the president’s reshoring goals imply replacing tens of millions of overseas manufacturing jobs.

China has more than 100 million manufacturing workers.

India has about 20 million.

Vietnam has more than 10 million.

That is 130 million to 150 million manufacturing jobs in just three Asian countries, many of which feed U.S. supply chains. Yet the United States cannot staff its existing plants, never mind an expanded industrial base, without automation.

Labor Quality: Americans Don’t Want These Jobs

The United States offshored manufacturing work for a reason. The positions are difficult, often dangerous, and generally not the kind of roles in which young Americans see a future.

A recent Cato Institute survey captured the mismatch:

80% of respondents say the nation would be better off if more people worked in manufacturing.

Only 20% say they would be better off working in a factory.

The workforce has moved on.

But, if President Trump has his way, the factories will be moving back.

Labor Cost: We Can’t Compete on Wages

The economics here are even starker:

Minimum wage in China averages about $300 a month.

Vietnam: roughly $200.

India: below $200 in many regions.

U.S. federal minimum wage implies more than $1,200 a month, and factories often pay far more.

U.S. labor is four to six times as expensive as most Asian labor. That math doesn’t pencil out unless companies deploy AI-powered machines that don’t take breaks, benefits, or paid time off.

The Only Way Reshoring Works Is With Physical AI

Put simply: Trump’s industrial renaissance only works if robots build it.

The 21st‑century American factory will not look like Detroit in the 1950s. It will look like Tesla Inc.’s (TSLA) Gigafactory, multiplied across industries.

There will be fewer humans working inside them, replaced instead by dozens of industrial arms, autonomous material handling, machine vision‑based quality-assurance systems, and zero‑light warehouses.

The goal may be to replace Chinese or Indian labor with American labor. The reality is that we’ll replace foreign humans with domestic machines.

That is why our team sees physical AI — robots, automation systems, machine vision — as the next leg of the AI Revolution.

Enter the Physical AI Revolution

Until now, most of the AI hype has revolved around language models, chatbots, and digital copilots. Those software breakthroughs have been transformative for knowledge work.

But the next frontier is the physical world:

Factory robots that can see, learn, and adapt.

Warehouse pick‑and‑pack bots powered by machine vision models.

Autonomous forklifts and mobile platforms.

AI‑driven robotic arms that can manufacture, weld, and inspect.

With Stargate’s build‑out of domestic compute capacity, that kind of robotic intelligence can scale quickly. Just as ChatGPT catalyzed digital AI adoption, the Trump administration-supported 2025‑’26 infrastructure wave could catalyze physical‑AI adoption across manufacturing, logistics, and defense.

Finding market-beating investments within emerging tech megatrends such as this is exactly what I excel at. My predictive record in emerging tech is well documented:

TipRanks named me the No. 1 Stock Picker of 2020, out of more than 15,000 professionals.

Since 2014, I have highlighted almost 200 stocks that went on to double and more than a dozen that soared 10X, 20X, even 30X — including Alphabet Inc. (GOOG), Amazon.com Inc. (AMZN), Meta Platforms Inc. (META), Apple Inc. (AAPL), Microsoft Corp. (MSFT), Tesla Inc. (TSLA), and Nvidia Corp. (NVDA) long before they were household names.

Those “Mag 7” calls turned a hypothetical $70,000 total investment (seven positions at $10,000 each) into about $1.2 million at peak.

Now, I believe the next wealth‑defining list will be a basket of small, U.S.‑based physical‑AI leaders I’m calling the “MAGA 7.” No, I’m taking political sides here.

In this case, “MAGA” stands for Make AI Great in America.

The Generational‑Wealth Window

This rare alignment of (1) a rally-inducing market signal (the one I’m predicting will happen on May 7), (2) a record cash hoard, and (3) a breakthrough technology platform has happened once in modern history — the late‑1990s dot‑com era.

Investors who acted early in 1997 could have turned five‑figure stakes into six‑ and seven‑figure fortunes in just a few years.

If I’m right, May 7 could mark the start of a second, and possibly larger, melt‑up — one in which physical‑AI winners become the new titans of American industry.

That is the sort of opportunity often described as “generational wealth.” It is not about adding a few percentage points to a portfolio. It is about potentially changing a family’s balance sheet for decades.

This is not merely a policy trend. It is an investment megatrend.

The economic math points to automation.

Political momentum points to domestic buildout.

The AI infrastructure build points to a physical AI supercycle.

President Trump wants to bring manufacturing back to America, but only robots can make the math work. If the Fed signals an easing cycle on May 7, the $7 trillion in sidelined cash could rush into the exact names supplying America’s next factory workforce.

That is why this coming Thursday, May 1, at 7 p.m. Eastern, I’m hosting an urgent strategy online session. During the event I’ll show you how we can not only protect our portfolios this summer… but also see triple-digit gains in the coming years.

Plus, like I’ve been saying, I’ll detail seven new opportunities – the “MAGA 7” – at the center of this historic Summer Panic.