10 Buy And Hold Forever Dividend Stocks For Decades Of Dividend Growth

Updated on February 24th, 2025 by Bob Ciura

It isn’t surprising that we favor stocks that pay dividends, as studies have shown that owning income producing securities is an excellent way to build wealth while also protecting to the downside.

In bull markets, dividends can add to the gains from the stock while also purchasing additional shares. When prices decline, dividends can reduce the losses while being used to acquire more shares at a now lower price.

With this in mind, we created a full list of the Dividend Kings, a group of stocks with over 50 consecutive years of dividend increases.

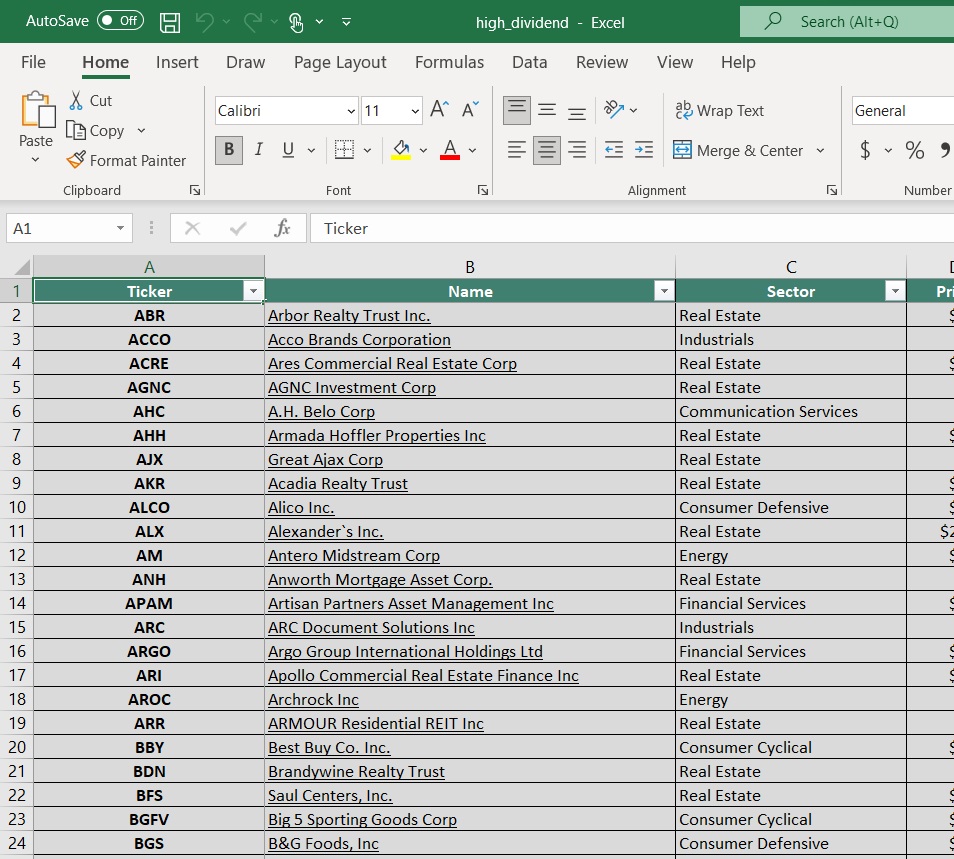

You can see the full downloadable spreadsheet of all 54 Dividend Kings (along with important financial metrics such as dividend yields, payout ratios, and price-to-earnings ratios) by clicking on the link below:

The Dividend Kings have rewarded shareholders with rising income for decades.

The following 10 stocks represent Dividend Kings that can continue to raise their dividends for decades to come.

The list includes 10 Dividend Kings with our highest Dividend Risk Score of ‘A’ in the Sure Analysis Research Database, that also have payout ratios below 70% to ensure a sustainable dividend payout.

The stocks are sorted by dividend payout ratio, from lowest to highest.

Table of Contents

Dividend King To Hold Forever: Nordson Corp. (NDSN)

Nordson was founded in 1954 in Amherst, Ohio by brothers Eric and Evan Nord, but the company can trace its roots back to 1909 with the U.S. Automatic Company.

Today the company has operations in over 35 countries and engineers, manufactures, and markets products used for dispensing adhesives, coatings, sealants, biomaterials, plastics, and other materials, with applications ranging from diapers and straws to cell phones and aerospace.

Source: Investor Presentation

On August 14th, 2024, Nordson increased its dividend by 15% to $0.78 per share quarterly, marking 61 years of increases.

On December 11th, 2024, Nordson reported fourth quarter results for the period ending October 31st, 2024. For the quarter, the company reported sales of $744 million, 4% higher compared to $719 million in Q4 2023, which was driven by a positive acquisition impact, and offset by organic decrease of 3%.

Industrial Precision saw sales decrease by 3%, while the Medical and Fluid Solutions and Advanced Technology Solutions segments had sales increases of 19% and 5%, respectively. The company generated adjusted earnings per share of $2.78, a 3% increase compared to the same prior-year quarter.

Click here to download our most recent Sure Analysis report on NDSN (preview of page 1 of 3 shown below):

Dividend King To Hold Forever: Sysco Corp. (SYY)

Sysco Corporation is the largest wholesale food distributor in the United States. The company serves 600,000 locations with food delivery, including restaurants, hospitals, schools, hotels, and other facilities.

Source: Investor Presentation

On January 28th, 2025, Sysco reported second-quarter results for Fiscal Year (FY)2025. The company reported a 4.5% increase in sales for the second quarter of fiscal year 2025, reaching $20.2 billion.

U.S. Foodservice volume grew by 1.4%, while gross profit rose 3.9% to $3.7 billion. Operating income increased 1.7% to $712 million, with adjusted operating income growing 5.1% to $783 million. Earnings per share (EPS) remained at $0.82, while adjusted EPS grew 4.5% to $0.93.

The company reaffirmed its full-year guidance, projecting sales growth of 4%-5% and adjusted EPS growth of 6%-7%.

Click here to download our most recent Sure Analysis report on SYY (preview of page 1 of 3 shown below):

Dividend King To Hold Forever: Archer Daniels Midland (ADM)

Archer-Daniels-Midland is the largest publicly traded farmland product company in the United States. Archer-Daniels-Midland’s businesses include processing cereal grains, oilseeds, and agricultural storage and transportation.

Archer-Daniels-Midland reported its third-quarter results for Fiscal Year (FY) 2024 on November 18th, 2024. The company reported adjusted net earnings of $530 million and adjusted EPS of $1.09, both down from the prior year due to a $461 million non-cash charge related to its Wilmar equity investment.

Consolidated cash flows year-to-date reached $2.34 billion, reflecting strong operations despite market challenges.

Click here to download our most recent Sure Analysis report on ADM (preview of page 1 of 3 shown below):

Dividend King To Hold Forever: Farmers & Merchants Bancorp (FMCB)

Farmers & Merchants Bancorp is a locally owned and operated community bank with 32 locations in California. Due to its small market cap and its low liquidity, it passes under the radar of most investors.

F&M Bank has paid uninterrupted dividends for 88 consecutive years and has raised its dividend for 59 consecutive years.

In late January, F&M Bank reported (1/23/25) financial results for the fourth quarter of fiscal 2024. The bank grew its earnings-per-share 9% over the prior year’s quarter, from $28.55 to a new all-time high of $31.11. Loans and deposits grew 1% each.

Net interest income dipped -3% due to a contraction of net interest margin from 4.30% to 4.05% amid higher deposit costs. Management remains optimistic for the foreseeable future, as the bank enjoys one of the widest net interest margins in its sector.

We reiterate that F&M Bank is one of the most resilient banks during downturns, such as the pandemic, a potential recession or the financial turmoil caused by the collapse of Silicon Valley Bank, Credit Suisse and First Republic.

Click here to download our most recent Sure Analysis report on FMCB (preview of page 1 of 3 shown below):

Dividend King To Hold Forever: Hormel Foods (HRL)

Hormel Foods was founded back in 1891 in Minnesota. Since that time, the company has grown into a juggernaut in the food products industry with nearly $10 billion in annual revenue.

Hormel has kept with its core competency as a processor of meat products for well over a hundred years, but has also grown into other business lines through acquisitions.

Hormel has a large portfolio of category-leading brands. Just a few of its top brands include include Skippy, SPAM, Applegate, Justin’s, and more than 30 others.

It has also pursued acquisitions to drive growth. For example, in 2021, Hormel acquired the Planters snack nuts business from Kraft-Heinz (KHC) for $3.35 billion, which has boosted Hormel’s growth.

Source: Investor Presentation

Hormel posted fourth quarter and full-year earnings on December 4th, 2024, and results were in line with expectations. The company posted adjusted earnings-per-share of 42 cents, which met estimates. Revenue was off 2% year-on-year to $3.14 billion, also hitting estimates.

Operating income was $308 million for the quarter on an adjusted basis, or 9.8% of revenue. Operating cash flow was $409 million for Q4.

For the year, sales were $11.9 billion, and adjusted operating income was $1.1 billion, or 9.6% of revenue. Adjusted earnings-per-share was $1.58. Operating cash flow hit a record of $1.3 billion.

Guidance for 2025 was initiated at $11.9 billion to $12.2 billion in sales, with organic net sales growth of 1% to 3%.

Click here to download our most recent Sure Analysis report on HRL (preview of page 1 of 3 shown below):

Dividend King To Hold Forever: PPG Industries (PPG)

PPG Industries is the world’s largest paints and coatings company. Its only competitors of similar size are Sherwin-Williams and Dutch paint company Akzo Nobel.

PPG Industries was founded in 1883 as a manufacturer and distributor of glass (its name stands for Pittsburgh Plate Glass) and today has approximately 3,500 technical employees located in more than 70 countries at 100 locations.

On January 31st, 2025, PPG Industries announced fourth quarter and full year results for the period ending December 31st, 2024. For the quarter, revenue declined 4.6% to $3.73 billion and missed estimates by $241 million.

Adjusted net income of $375 million, or $1.61 per share, compared favorably to adjusted net income of $372 million, or $1.56 per share, in the prior year. Adjusted earnings-per-share was $0.02 below expectations.

Source: Investor Presentation

For the year, revenue from continuing operations decreased 2% to $15.8 billion while adjusted earnings-per-share totaled $7.87.

PPG Industries repurchased ~$750 million worth of shares during 2024 and has $2.8 billion, or ~10.3% of its current market capitalization, remaining on its share repurchase authorization. The company expects to repurchase ~$400 million worth of shares in Q1 2025.

For 2025, the company expects adjusted earnings-per-share in a range of $7.75 to $8.05.

Click here to download our most recent Sure Analysis report on PPG (preview of page 1 of 3 shown below):

Dividend King To Hold Forever: California Water Service Group (CWT)

California Water Service is a water stock and is the third-largest publicly-owned water utility in the United States.

It was founded in 1926 and has six subsidiaries that provide water to approximately 2 million people in 100 communities, primarily in California but also in Washington, New Mexico and Hawaii.

Source: Investor Presentation

California Water Service reported its third quarter earnings results on October 31st. Operating revenues totaled $300 million during the quarter, which was 18% higher than the same quarter last year. This represents a stronger performance compared to what the analyst community had forecasted.

The operating revenue increase was driven by rate increases over the last year as well as by higher accrued unbilled revenue compared to the previous year’s quarter.

Click here to download our most recent Sure Analysis report on CWT (preview of page 1 of 3 shown below):

Dividend King To Hold Forever: Gorman-Rupp Co. (GRC)

Gorman-Rupp began manufacturing pumps and pumping systems back in 1933. Since that time, it has grown into an industry leader with annual sales of nearly $700 million and a market capitalization of $1 billion.

Today, Gorman-Rupp is a focused, niche manufacturer of critical systems that many industrial clients rely upon for their own success.

Gorman Rupp generates about one-third of its total revenue from outside of the U.S.

Source: Investor Presentation

Gorman-Rupp posted fourth quarter and full-year earnings on February 7th, 2025, and results were weaker than expected. Adjusted earnings-per-share came to 42 cents, which was three cents light of estimates.

Revenue was up 1.3% year-over-year to $162.7 million, which matched expectations. The increase in sales was primarily attributed to the impact of pricing increases taken in the year-ago period.

Gross profit was $49.2 million for the quarter, or 30.2% of revenue. These were down from $50.9 million and 31.7%, respectively, in the same period of 2023.

The decline in gross margins of 150 basis points included 220 basis points of increased labor and overhead costs, which were driven by healthcare expenses.

That was partially offset by a 70-basis point improvement in cost of materials, which itself was driven by a 140-basis point improvement in selling prices offset by a 70-basis point decline from inventory costing.

Click here to download our most recent Sure Analysis report on GRC (preview of page 1 of 3 shown below):

Dividend King To Hold Forever: SJW Group (SJW)

SJW Group is a water utility company that produces, purchases, stores, purifies and distributes water to consumers and businesses in the Silicon Valley area of California, the area north of San Antonio, Texas, Connecticut, and Maine.

SJW Group has a small real estate division that owns and develops properties for residential and warehouse customers in California and Tennessee. The company generates about $670 million in annual revenues.

Source: Investor Presentation

On October 28th, 2024, SJW Group reported third quarter results for the period ending June 30th, 2024. For the quarter, revenue grew 9.9% to $225.1 million, beating estimates by $11.6 million. Earnings-per-share of $1.18 compared favorably to earnings-per-share of $1.13 in the prior year and was $0.04 more than expected.

As with prior periods, the improvement in revenue was mostly due to SJW Group’s California and Connecticut businesses, which benefited from higher water rates, while growth in customers aided the Texas business.

Higher rates overall added $40 million to results for the quarter, higher customer usage added $4.8 million, and growth in customers contributed $2.4 million. Operating production expenses totaled $166.7 million, which was a 12% increase from the prior year.

Click here to download our most recent Sure Analysis report on SJW (preview of page 1 of 3 shown below):

Dividend King To Hold Forever: Stepan Co. (SCL)

Stepan manufactures basic and intermediate chemicals, including surfactants, specialty products, germicidal and fabric softening quaternaries, phthalic anhydride, polyurethane polyols and special ingredients for the food, supplement, and pharmaceutical markets.

It is organized into three distinct business lines: surfactants, polymers, and specialty products. These businesses serve a wide variety of end markets, meaning that Stepan is not beholden to just a handful of industries.

Source: Investor presentation

The surfactants business is Stepan’s largest by revenue, accounting for ~68% of total sales in the most recent quarter. A surfactant is an organic compound that contains both water-soluble and water-insoluble components.

Stepan posted fourth quarter and full-year earnings on February 19th, 2025, and results were mixed once again. Revenue was down 1.2% year-on-year to $526 million, but did beat estimates by almost $5 million. Adjusted earnings-per-share came to 12 cents, which missed estimates by 21 cents.

Global sales volume was off 1% year-over-year as double-digit growth in surfactants was offset and then some by demand weakness in polymers. Surfactants were up 3% year-over-year in Q4 to $379 million. Polymer net sales fell 12% to $130 million.

The company managed to generate about $13 million in pre-tax cost savings during the quarter, and about $48 million for the full year.

Click here to download our most recent Sure Analysis report on SCL (preview of page 1 of 3 shown below):

Final Thoughts

Screening to find the best Dividend Kings is not the only way to find high-quality dividend growth stocks to hold forever.

Sure Dividend maintains similar databases on the following useful universes of stocks:

There is nothing magical about investing in the Dividend Kings. They are simply a group of high-quality businesses with shareholder-friendly management teams that have strong competitive advantages.

Purchasing businesses with these characteristics–at fair or better prices–and holding them forever, will likely result in strong long-term investment performance.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].